{kind=link}

The main event next week will be the European Central Bank (ECB) policy meeting, where markets are pricing in a 90% probability for a rate cut even though economists forecast no action. It’s a close call, but the fragmented ECB may opt for more targeted lending measures to shield the economy from the virus fallout, not a rate cut. There’s also a raft of economic data coming up, alongside the UK government budget. All told, markets will continue to dance to the tune of news about the virus.

ECB meeting: Targeted action, not blanket cuts

After the American, Canadian, and Australian central banks all slashed rates this week to negate the negative effects of the coronavirus on their economies, it’s now the turn of European policymakers to decide whether to follow suit. The ECB will conclude its meeting on Thursday and while markets are convinced rates will be cut by 10 basis points to -0.6%, economists disagree.

And with good reason. European interest rates are deep in negative territory already, meaning that the ECB only has a couple more ‘rate bullets’ left, and it might prefer to save them for a crisis where monetary policy can actually help. Cutting rates is a weak ‘antidote’ for a supply-side shock like this one, and even the positive effects on demand are questionable if fears intensify enough for consumers to curtail spending.

Another issue is how divided ECB officials are. Several policymakers – especially those representing large economies like Germany and France – think that monetary policy is already extremely accommodative and that any more stimulus would do next to nothing to boost the struggling economy. Therefore, cutting rates further may be a bridge too far.

Instead of cutting rates, the ECB could announce a scheme to provide liquidity to businesses impacted by the virus, helping those that have seen their supply lines cut and their cash flows dry up, by giving them very cheap loans. This is arguably the best strategy available, considering that the Bank is low on policy ammunition and highly divided. It won’t really boost market confidence, but it does put a ‘bandage’ on the wound.

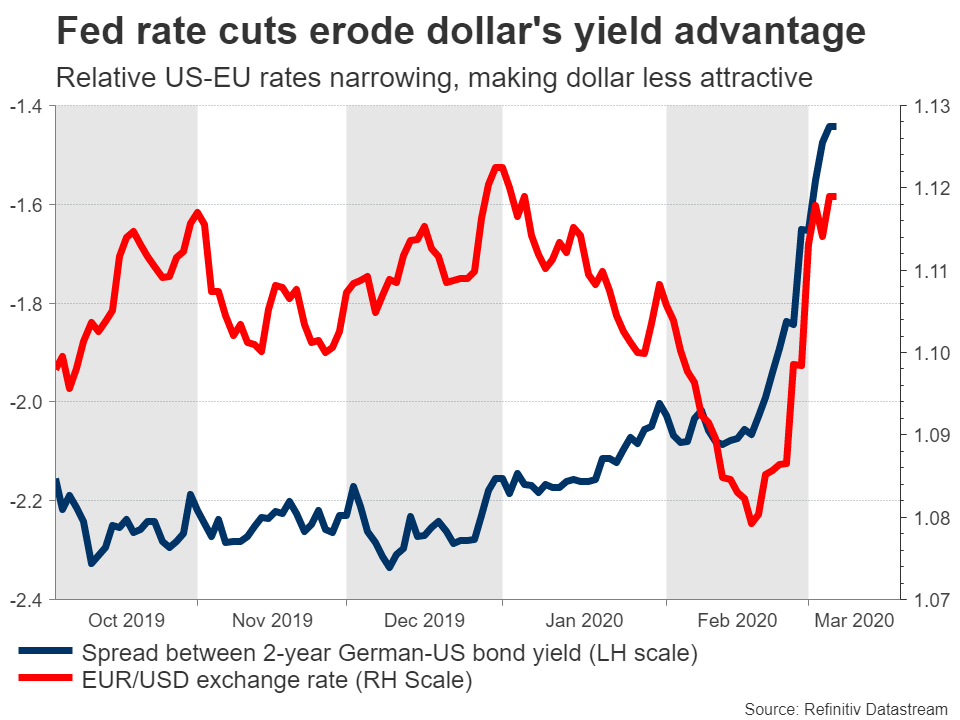

As for the euro, if the ECB doesn’t cut rates, then the single currency could spike higher, extending the gains it posted in recent weeks as risk appetite soured and carry trades were unwound. In the bigger picture though, unless risk sentiment continues to deteriorate, it’s difficult to envision a sustained rally in the euro from here.

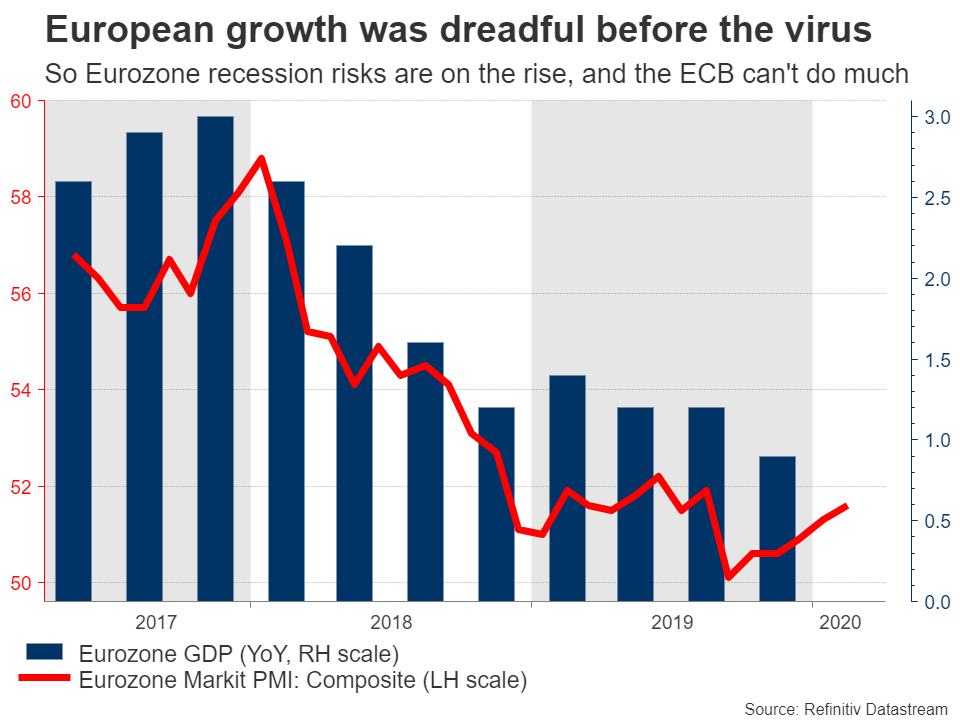

The US economy is much healthier than the Eurozone, which given Italy’s troubles may be facing the threat of a recession soon. Meanwhile, US authorities are getting ahead of this risk by adding powerful stimulus to shield their economy, and the Europeans aren’t. Another thing to consider is that markets are now pricing in almost four Fed rate cuts by September. If for any reason the Fed doesn’t deliver as much, the dollar could get a strong shot in the arm.

Chinese data to reveal extent of virus damage

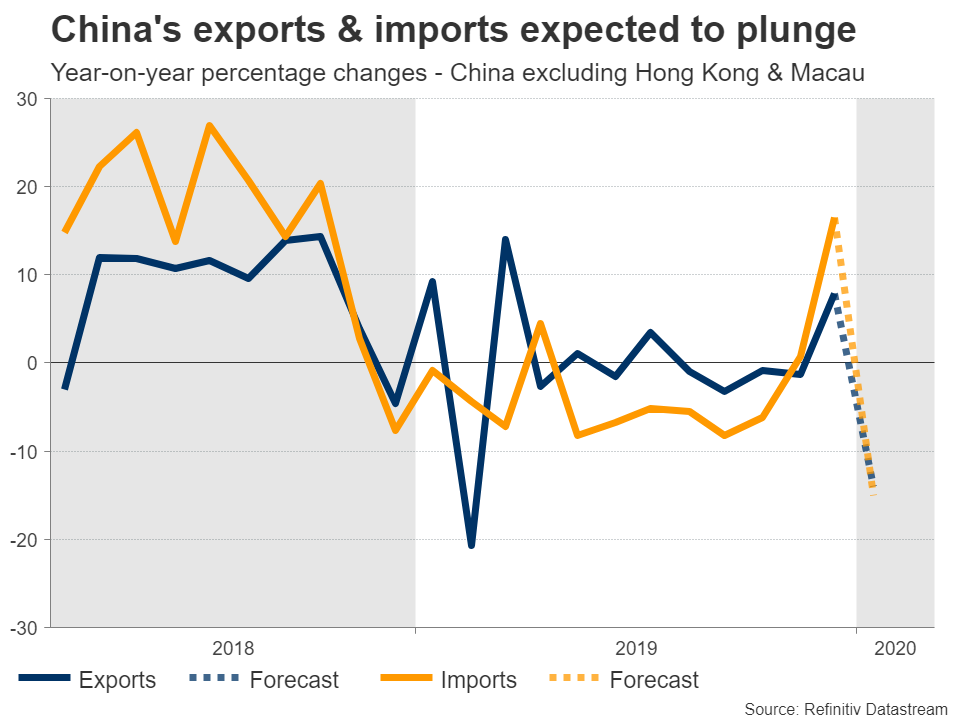

The world’s second biggest economy has been ravaged by the virus in recent weeks, with many factories staying closed and consumers turning defensive. The PMIs for February showed a collapse in economic activity, and the upcoming ‘hard data’ are likely to reaffirm as much.

China’s trade data for February are due over the weekend, and forecasts point to a sharp drop in both exports and imports. Then on Tuesday, inflation data for the same month will be released, and markets may focus mainly on the producer price index, which is seen as gauge of industrial demand.

As for risk sentiment, it’s hard to envisage a real turnaround soon. Central bankers are already throwing everything they have at this problem, and while they’ve successfully halted the plunge in stock markets, it hasn’t been enough to actually lift equities. News flow is also likely to remain negative as the number of infections rises outside of China. The fear is that this could eventually hit demand if consumers rein in spending on entertainment activities and travel, for example.

For risk appetite to truly recover, markets may need to see a slowdown in the number of infections, which would fuel the narrative that global demand won’t take a severe hit. However, with the virus spreading quickly in the US and Europe, that point may be far away still.

Will UK budget lift the pound?

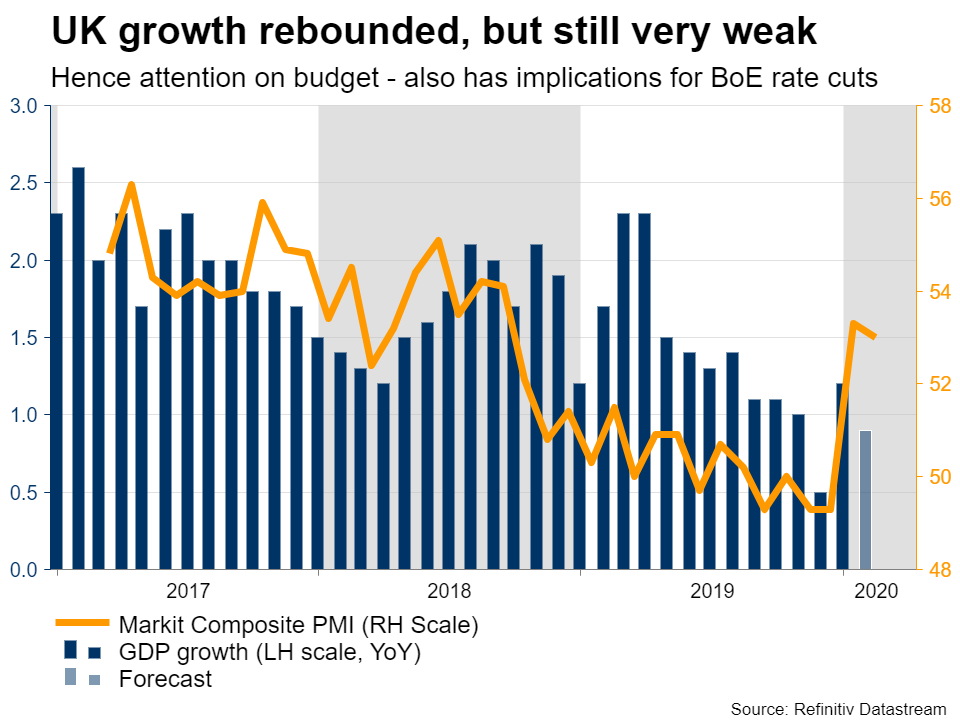

In Brexit land, the key event will be the unveiling of the government’s budget on Wednesday. With the UK economy slowing down and the virus threatening to dampen growth even further, investors will scrutinize how expansionary this budget is. A budget that includes a big boost to public spending might see the pound gain, by fueling expectations that the Bank of England (BoE) may not have to cut rates aggressively to stimulate the economy by itself.

Cable has rebounded lately, though admittedly, that reflects more dollar weakness than sterling strength. In the very near term, this upswing could continue. Not only because of the budget, but also because the BoE is unlikely to cut rates as aggressively as markets think. A quarter-point rate cut at the March 26 meeting is now fully priced in, and markets are also pricing in a 40% probability for a larger, half-point cut.

Just a couple of days ago, though, incoming BoE Governor Andrew Bailey said the Bank should wait for more data that capture the economic hit of the virus before deciding whether to cut. While the BoE may cut in March regardless, his comments suggest the Bank won’t deliver the aggressive half-point cut some are looking for, which argues for more gains in the pound as those dovish expectations are priced out.

However, the pound’s surge may not last long. The Brexit negotiations finally resumed this week and considering recent comments by PM Johnson about not adhering to EU rules and being prepared to walk away from the talks, it may be a matter of time before the posturing and the drama return. In other words, the risk of a disorderly Brexit hasn’t disappeared, and such worries may intensify going forward if no material progress is made.

On the data front, GDP numbers for January are also out on Wednesday, but may be overshadowed by the budget.

US CPI not a game changer for Fed

In the States, the main release will be the CPI for February, due on Wednesday. Yet, with the Fed so focused on the virus, economic data might not matter much for the dollar’s near-term path. The Fed is not reacting to any real weakness in the US economy. Rather, it’s trying to shield the economy from the future virus impact.

Therefore, markets are now pricing in another half-point (50bp) rate cut at the Fed’s March meeting, and it’s doubtful that even stellar data between now and then would be enough to change that.