{kind=link}

US stocks bounced back as traders reflected on the Fed rate cut, Joe Biden surge, and positive economic data. The Fed slashed rates by 50 basis points on Tuesday as officials saw a material change in the US economic outlook. Shortly afterwards, Joe Biden made one of the biggest political comebacks in modern history. He surged forward to win more delegates on Super Tuesday. Yesterday, data from ADP showed that the economy added more than 188k private payrolls in February, which was higher than the expected 170k. We will receive the official NFP data tomorrow. Also, data from the Institute of Supply Management showed that non-manufacturing PMI rose to 57.3, which is the highest level since February last year. Healthcare stocks led the market with a 5.8% gain, which is their best day since 2008.

Oil prices rose slightly during the American session as traders waited for an important OPEC+ meeting. The meeting is set to address the recent drop in oil prices as demand falls. In a report yesterday, Markit said that oil demand will have its steepest decline on record in the first quarter. The firm attributed this to school closures and the decision by airlines to cancel flights. Saudi Arabia is said to be calling for supply cuts of one million barrels a day to stabilize prices. Russia, a non-OPEC member that has collaborated with the cartel has balked at making more cuts. Today, we will look at the progress and whether the countries will agree on a positive path forward.

The Australian dollar rose slightly as the country’s central bank signalled that it will start quantitative easing. The RBA believes that coronavirus will knock at least half a percentage point off GDP in the first quarter. In a statement to parliament, the deputy central bank governor said that the bank had the capacity of one more rate cut. Beyond that, he said that quantitative easing would be the only option. This statement came a day after the country unexpectedly slashed interest rates to 0.50%. Today, data from the country showed that exports and imports dropped by 3% in January as the trade surplus narrowed down to $5.21 billion.

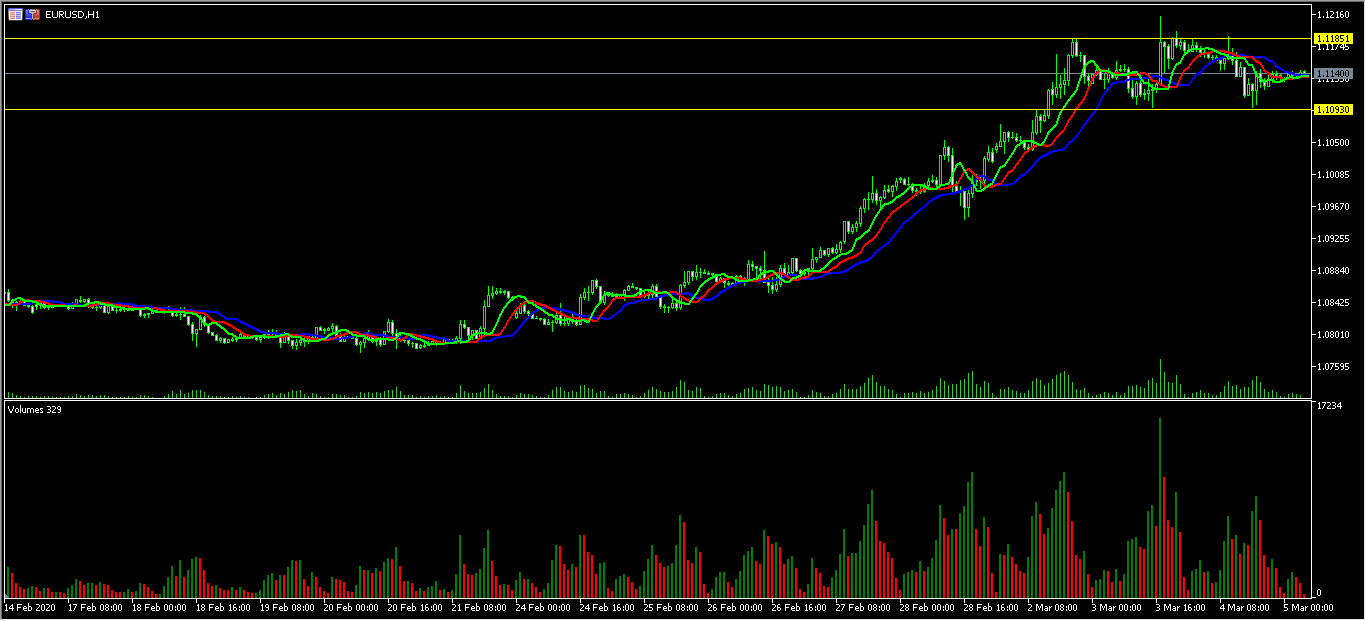

EUR/USD

The EUR/USD pair was little changed in the American and Asian sessions. The pair is trading at 1.1140, which is slightly above yesterday’s low of 1.1093 and slightly below yesterday’s high of 1.1185. As a result of this consolidation, the price is along the jaw, lips, and teeth lines of the alligator indicator. Volumes have also declined. The pair may remain inside the current channel ahead of the official jobs report tomorrow.

XBR/USD

The XBR/USD pair rose slightly to a high of 51.80 during the Asian session. This price is slightly below yesterday’s high of 53.77 and above last week’s low of 48.88. The price is along the 14-day and 28-day moving averages while the RSI has remained neutral at 48. The signal line of the MACD has declined and is about to pass the centreline. The pair will likely see significant movements today as OPEC members meet.

AUD/USD

The AUD/USD pair rose to an intraday high of 0.6628, which is above Friday’s low of 0.6433. The price is slightly above the 14-day and 28-day moving averages. It is also above the Ichimoku cloud on the hourly chart. The RSI has risen slightly and the price is slightly above the 61.8% Fibonacci Retracement level. The pair will likely continue rising today.