{kind=link}

We now look for the FOMC to cut rates 100 bps by the end of Q2-2020 due to the growth-slowing effects that the COVID-19 outbreak has imparted to the economy. However, the timing of the rate cuts is highly uncertain.

U.S. Economy Likely Will Slow in Coming Quarters

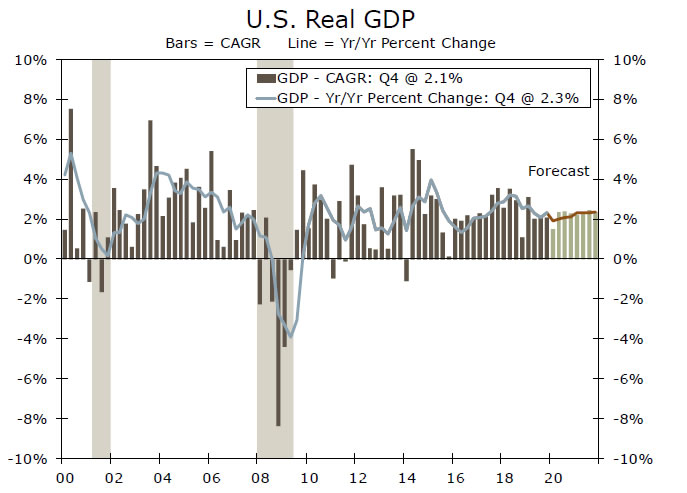

We have been forecasting that the Fed would keep its target range for the fed funds rate unchanged at 1.50% to 1.75% through at least the end of this year. This outlook for the fed funds rate was predicated on our forecast that the U.S. economy would grow at a trend-like 2.0% in 2020 (top chart). We will not update our GDP forecast until March 11, but the risks to our view that the U.S. economy will grow 2.0% this year now seem to be skewed to the downside due to the COVID-19 outbreak. Although the situation remains very fluid, there are three channels through which U.S. real GDP growth could downshift, at least in the next few quarters.

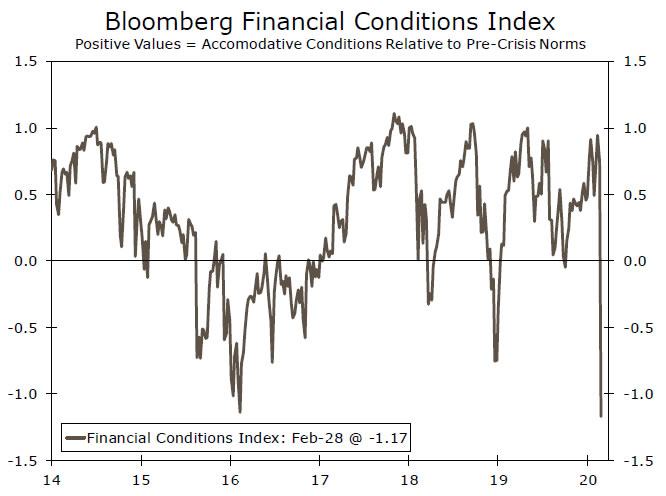

First, slower growth in countries that have been affected by the outbreak will exert headwinds on U.S. export growth. Second, as we have written in a number of reports in recent weeks, the U.S. supply chain could be adversely affected by output stoppages in other countries. Third, financial conditions have tightened significantly over the past week or so (middle chart). Not only has the stock market swooned, but corporate bond spreads have pushed wider. If the selloff in capital markets is sustained, banks could eventually tighten lending standards for businesses and households.

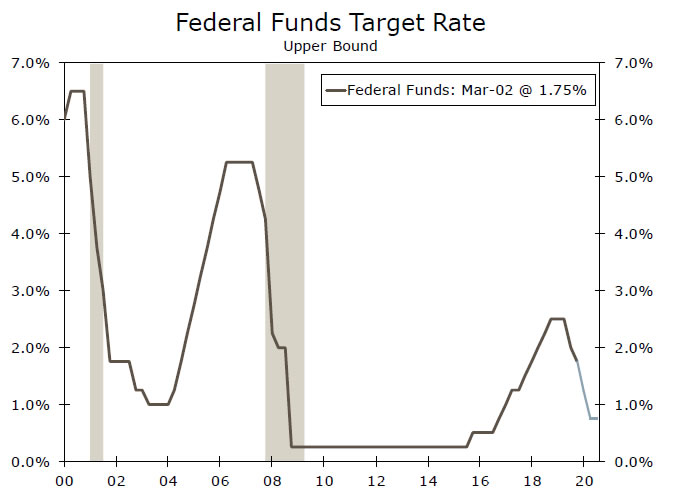

Consequently, we now look for the FOMC to cut rates 100 bps by the end of Q2-2020 (bottom chart). That said, we are uncertain about the exact timing of the rate cuts. If financial markets continue to spiral lower, the FOMC may very well decide to cut rates before the committee’s next scheduled meeting on March 18. Or the committee could wait until March 18 to cut rates 50 bps with a follow-up 50 bps rate cut on April 29, or it could spread the rate cuts out to the June and July meetings. The timing of rate cuts will depend on the spread of the COVID-19 outbreak and its effects on economic activity, which are all very much uncertain at this time. We also look for the yield on the 10- year Treasury security to end the year in a range of 1.25% to 1.50%.

In some sense, Fed rate cuts are ill-suited to offset the supply shock that the COVID-19 outbreak has imparted to the global economy. But as we argued in a recent report, there would be some beneficial effects stemming from lower interest rates. Fed Chairman Powell suggested on February 28 that the committee is prepared to ease policy by stating that the Federal Reserve will use its “tools and act as appropriate to support the economy.”

We believe that our updated outlook of 100 bps of Fed rate cuts is evenly balanced by upside and downside risks in the current uncertain environment. If authorities succeed in bringing the outbreak under control in the near future, then the FOMC may not need to cut rates 100 bps. On the other hand, if the U.S. economy were to slip into recession because of the outbreak, then the Fed very well take its range for the fed funds rate all the way back to the zero lower bound. Stay tuned.