{kind=link}

For the 24 hours to 23:00 GMT, the EUR rose 0.25% against the USD and closed at 1.1029 on Friday.

On the data front, Germany’s unemployment rate remained unchanged at 5.0% in February, in line with market expectations. Meanwhile, consumer price inflation climbed 1.7% on a yearly basis in February, marking its highest level since July and compared to a similar level in the previous month.

In the US, the final Michigan consumer sentiment index climbed to 101.0 in February, compared to a level of 99.8 in the prior month. The preliminary figures had indicated an advance to 100.9. Additionally, the Chicago Fed Purchasing Managers’ Index advanced to 49.0 in February, compared to a level of 42.9 in the prior month. Moreover, advance goods trade deficit narrowed to $65.5 billion in January, compared to a revised deficit of $68.7 billion in the previous month. Furthermore, personal income advanced by 0.6% on a monthly basis in January, compared to a revised rise of 0.1% in the previous month. On the contrary, personal spending rose by 0.2% on a monthly basis in January, less than market forecast for a rise of 0.3% and compared to a revised rise of 0.4% in the prior month.

In the Asian session, at GMT0400, the pair is trading at 1.1049, with the EUR trading 0.18% higher against the USD from Friday’s close.

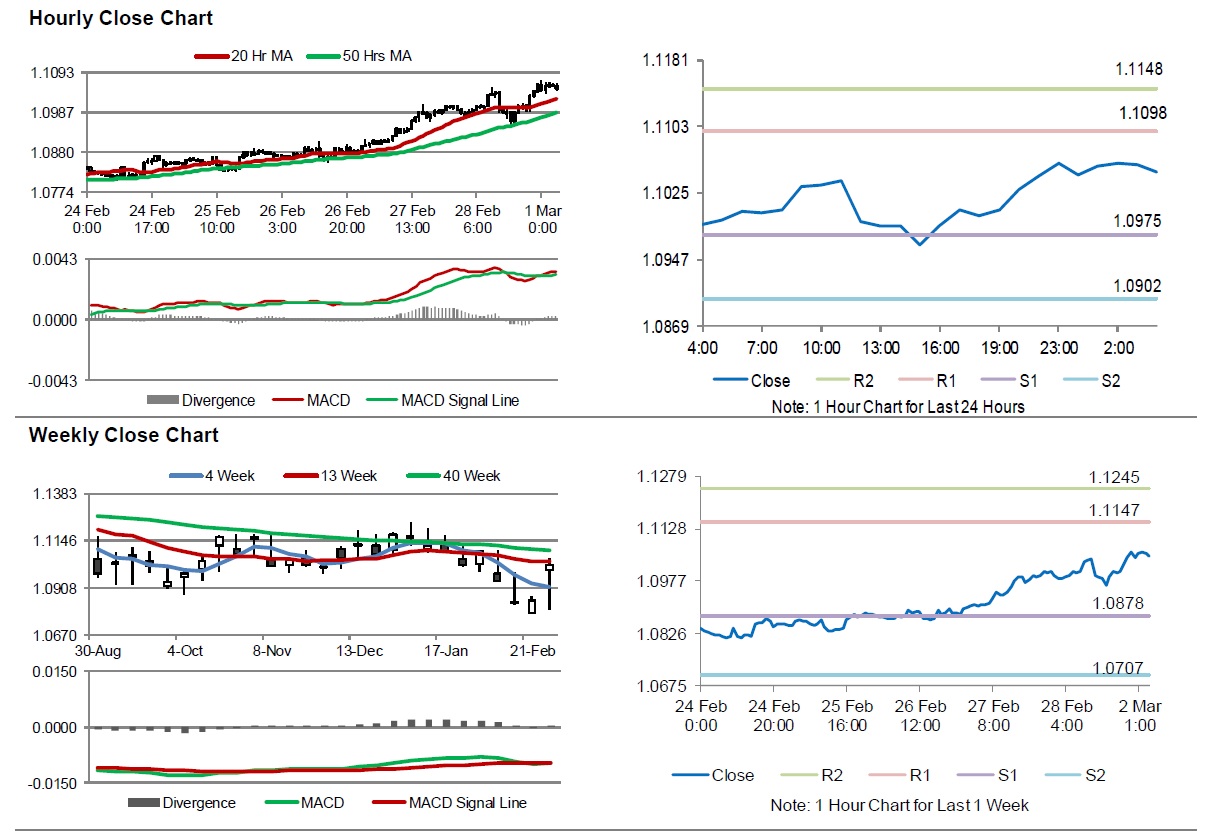

The pair is expected to find support at 1.0975, and a fall through could take it to the next support level of 1.0902. The pair is expected to find its first resistance at 1.1098, and a rise through could take it to the next resistance level of 1.1148.

Moving ahead, investors would closely monitor the Markit manufacturing PMIs scheduled to release across the Euro-zone in a few hours. Later in the day, the US Markit manufacturing PMI and the ISM manufacturing PMI, both for February, as well as construction spending data for January, would pique significant amount of market attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.