{kind=link}

- Fed to stay on hold today, but adopt a slightly more cautious tone?

- Yen retreats, stocks rebound as risk sentiment recovers

- However, bond and stock markets are not on the same page today

- Barrage of corporate earnings coming up: Microsoft, Facebook, Tesla, Boeing

No action from Fed, but perhaps a more dovish take

Investors may finally divert their attention away from the deadly coronavirus today, when the Federal Reserve concludes its policy meeting at 19:00 GMT. There’s virtually no chance of a rate cut and since this is one of the ‘smaller’ gatherings without updated economic forecasts, the market reaction may depend entirely on Chairman Powell’s remarks during the subsequent press conference at 19:30 GMT.

The American economy remains in good shape overall, with growth running at a healthy clip around 2%, supported by strong consumption and a revitalized housing market. Moreover, trade concerns have dropped off the financial radar for the time being, following the ‘phase one’ US-China deal.

Yet, there have also been some worrisome spots lately. Real wage growth has cooled, and the broader labor market is exhibiting signs of stress too, with job openings trending lower – an early indication that employment growth may be about to slow. The manufacturing sector continues to contract, while inflation as measured by the core PCE index remains muted. And while trade worries have faded for now, virus worries may have taken their place, as the potential impact on the global economy is still a mystery.

All this suggests that if there is any change in tone from the Fed today, it might be towards a more cautious narrative, where policymakers highlight the slowing data pulse and the mounting global risks. If so, the dollar might drop as investors price in a higher probability for a near-term rate cut.

Having said that, the broader outlook for the world’s reserve currency still seems positive. There’s no real alternative to the dollar right now, which offers a unique combination of safety alongside high(er) interest rates, compared to its major peers like the euro or yen. For that to change, either the Fed needs to start cutting rates aggressively, or the Eurozone has to launch a meaningful fiscal spending package to boost growth.

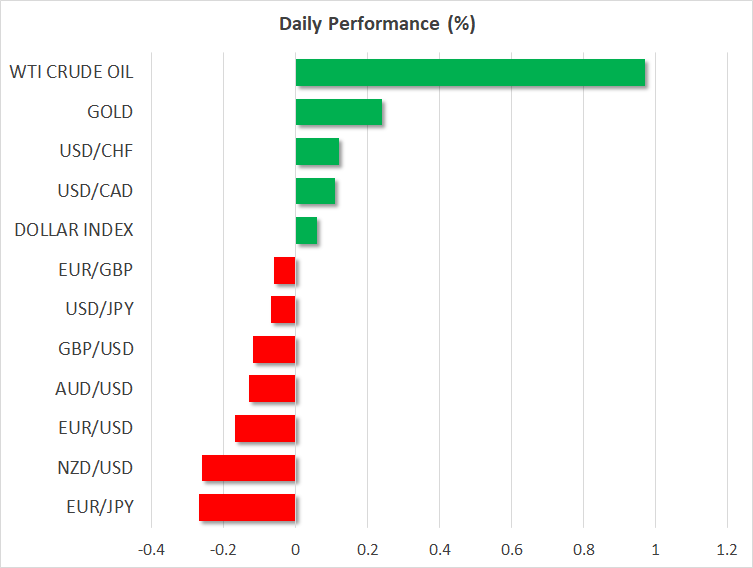

Risk sentiment recovers, but investors still undecided

Riskier assets and safe havens continue to trade like a rollercoaster, with American stocks recovering a good chunk of their virus-related losses on Tuesday, while defensive currencies like the yen and Swiss franc surrendered ground. It seems ‘no news is good news’ on the virus front, with traders brushing aside the ever-increasing number of confirmed cases, taking heart from the measures taken in China and by other countries to prevent further spread of the virus.

The recovery also drew strength from solid US data. The Conference Board consumer confidence index rose by more than expected in January, allaying concerns about the outlook for consumption. Since this index is considered an early recessionary signal, its unexpected strength likely pushed back the ‘day of reckoning’, lifting stocks.

On Wednesday though, risk sentiment is caught in ‘no man’s land’. Futures point to a modestly higher open on Wall Street, but Treasury yields are lower, so the stock and bond markets are signaling very different things about what the day ahead holds. As such, a single headline could tip the scales.

Moreover, the bond-stock market divergence highlights that risk sentiment is not out of the woods yet and that investors are still on the defensive, even if equities are behaving otherwise thanks to an abundance of liquidity. Expectations about corporate earnings could also be a factor affecting this puzzle.

Parade of earnings hits Wall Street today

Besides the Fed, traders will keep a close eye on quarterly earnings results by several heavyweight corporate players today. Notable names in the spotlight include Microsoft, Facebook, Tesla, and Boeing.