{kind=link}

- US and China reach a deal on a ‘phase one’ trade deal but details fail to impress

- Equities rally eases as euphoria begins to fade; yen extends losses

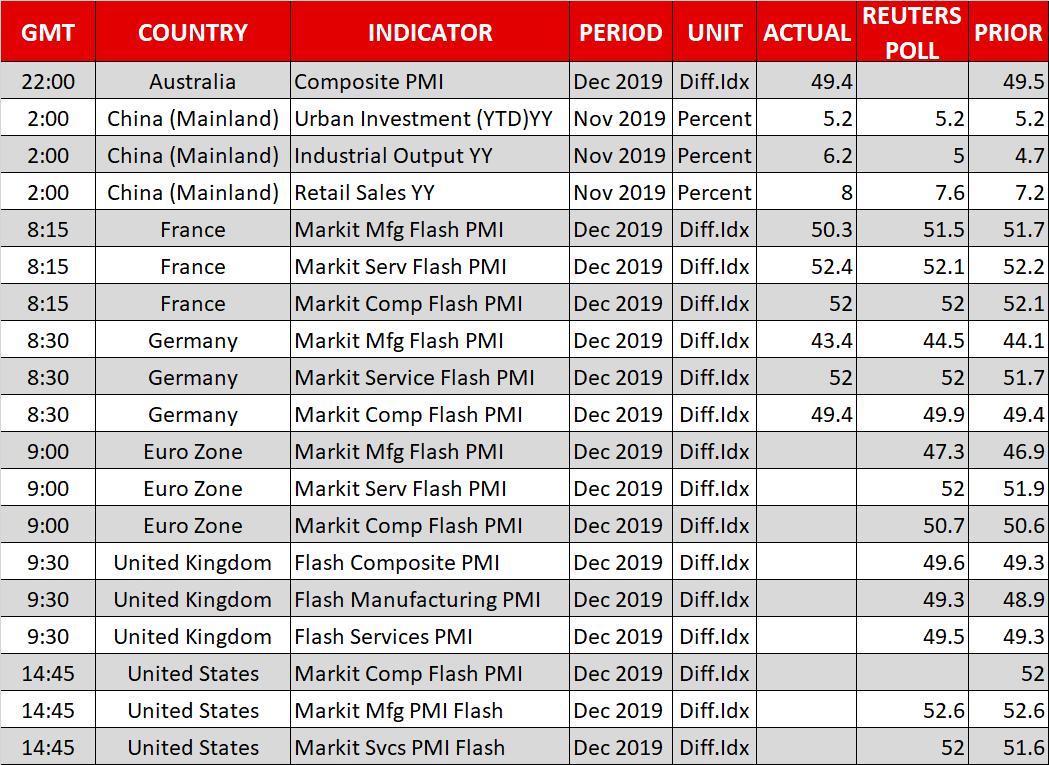

- Flash December PMIs in focus in Europe and US

US and China confirm an interim deal

The United States and China confirmed reports on Friday that a ‘phase one’ trade deal had been agreed by the two sides, ending weeks of speculation about whether a preliminary accord was possible before the end of the year.

Speaking to CBC on Sunday, US Trade Representative Robert Lighthizer assured that “this is totally done, absolutely”. Under the terms of the deal, China will increase its purchases of US agricultural goods to about $40-$50 billion annually. In total, China will purchase an additional $200 billion of goods from the US. In return the US has agreed to suspend the planned tariffs for December 15 and halve them on up to $120 billion of tariffs from 15% to 7.5%.

However, the size of the reduction on existing duties fell short of an earlier Wall Street Journal report that the US will cut tariffs on all $360 billion worth of Chinese imports. This and the absence of much details about the deal left markets disappointed, leading to only mild gains on Wall Street on Friday and for many Asian indices to pare earlier advances by today’s close.

Risk assets set to end year on a high

But while the initial jubilation of the long-awaited announcement proved short lived, the agreement is still a milestone that should substantially diffuse trade tensions between the world’s two largest economies as well as pave the way for a ‘phase two’ deal. Though there’s already some confusion as to when negotiations on ‘phase two’ will begin with Lighthizer contradicting President Trump’s Twitter comments that they would start immediately.

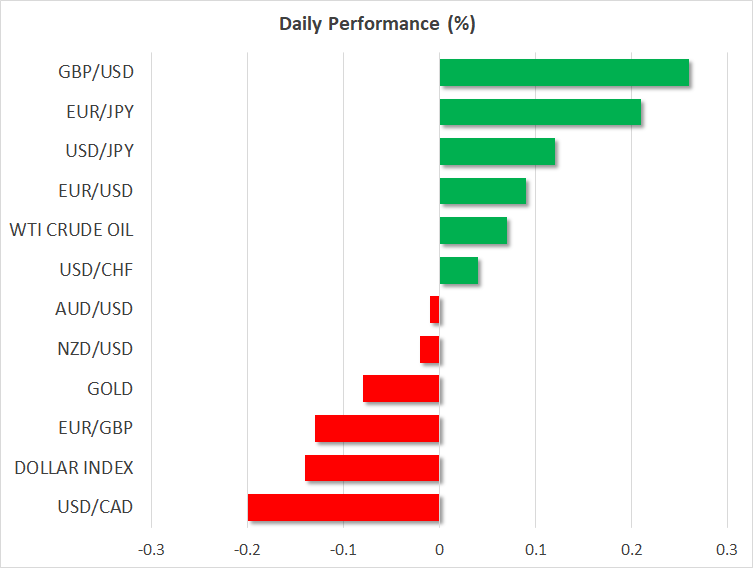

For now, markets are breathing a sigh of relief that a concrete agreement has finally been achieved and risk assets looks set to end the year on a high. Equity futures for US stocks were pointing to a modest but solid start on Monday. European indices fared better as apart from the Sino-US deal, the decisive British election result also boosted shares in the region, particularly, London’s FTSE 100, which soared to a near 3-week high at today’s open.

In currency markets, the pound continued to ride on the post-election wave to briefly hit the $1.34 level. The buoyant pound weighed on the dollar index, which was marginally lower today, though the greenback did manage to climb versus the safe-have yen, which has been on the retreat for the past week on the back of the receding geopolitical uncertainties.

The Australian and New Zealand dollars were flat versus their US counterpart, with the aussie giving up earlier gains after Australia’s government downgraded the country’s growth forecast, fuelling expectations of further monetary easing.

Mixed Eurozone PMIs dent euro’s advances

The euro, meanwhile, was struggling to hold onto its gains after the flash PMIs out of the Eurozone showed the block’s economy was not out of the woods just yet.

Services activity bounced back in December, according to IHS Markit’s preliminary report, but the manufacturing PMI fell back again, leaving the composite PMI unchanged in the last month of the year. Still, the data is unlikely to alter policy at the European Central Bank, with new president, Christine Lagarde, sounding more upbeat about the Eurozone’s prospects than her predecessor in her first policy meeting last week.

Flash PMIs will be watched out of the UK shortly, followed by the US at 14:45 GMT.