{kind=link}

Is the RBA headed for unconventional policy?

Up ahead markets catch two RBA speeches. Deputy Gov. Guy Debelle speaks on “Employment and Wages” at 10.50am AEDT. RBA Gov. Philip Lowe gives a talk titled “Unconventional Monetary Policy: Some Lessons From Overseas” at 8.05pm AEDT. While both are important, we pay particular attention to the latter given its potential to adjust rate expectations in the yield curve, and having flagged it in early October in a SPECIAL REPORT: AUD Outlook – UMPT.

We think AUDUSD traders will have their finger on the pulse in terms of how they react to Lowe’s tone from the speech, with two questions of significant value: when UMPT is likely and what form it could take. Guidance in these two areas likely triggers adjustments in how markets are pricing 2020 rate cuts. Around 7bps of cuts are currently priced into Dec 2019. As AUD long positioning is substantial relative to other G10 currencies, we think this could open the door to some long covering should Lowe usher a positive view on UMPTs.

ASX points up on overnight highs

There wasn’t an equities bear in sight in NY with major US benchmarks S&P 500 and Nasdaq charging to all-time highs. This should bode well for Aussie equities at the open with ASX Dec Futures suggesting a 27pt rally. A combination of Fed liquidity injections and net positive US-China trade talks are likely the drivers of the move. But again, as we’ve noted here there continues to be a divergence between equity fundamentals, the likelihood of a US-China phase 1 deal and bullish equities price action. Hence, we suspect Fed Repo operations are having a significant impact behind the scenes above all else.

New Zealand retail sales improve as expected

Early morning data in quarterly NZ retail sales out at 8.45am AEDT didn’t disappoint, coming out much stronger on the prior month. Retail Sales Volume q/q printed 1.6% vs the previous 0.2%. Retail quarterly vs 1 year ago showed a 4.5% gain, up on 2.9% in Q2. NZDUSD has reacted to the announcement climbing 0.17% in early trading. However, NZ 10y yields remain unchanged. Stronger NZ retail sales are commensurate with the RBNZ’s decision to leave rates on hold over the summer, with their next meeting not till Feb 2020.

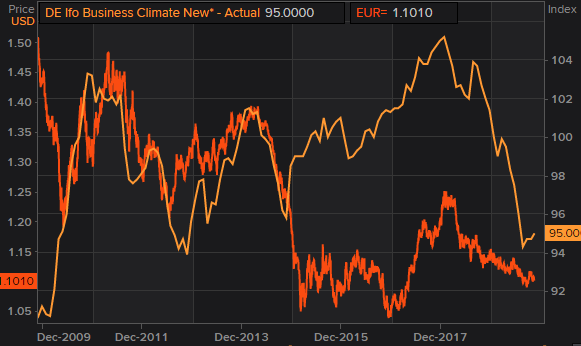

Did German IFO surveys disappoint?

Building off our preview of German IFOs yesterday markets were hesitant in driving EUR sentiment higher when the main Business Climate survey printed 95 in line with expectations, a small improvement on the prior month’s 94.6. Comments from the IFO institute highlighted the fact that despite last week’s beat in PMIs, German manufacturing and services still look vulnerable. In particular, excerpts from their release commented that “manufacturing is still stuck in a recession”. The release went some way to confirm our view that downside pressure remains on EURUSD and getting into short EURGBP may look fair value.

In the chart below, we show that German IFO and EURUSD have moved together in broad strokes over the past 10 years.