{kind=link}

Dec. rate cut still unlikely despite dovish RBA minutes

AUDUSD was offered 20pips on the RBA’s release of November Minutes but has since edged back up above 0.68 following a slight uptick in broad risk sentiment. Most of the statement read in line with prior releases but there were some lines of interest that rubbed off as dovish on the reader. Importantly, the Board noted that the case to ease monetary policy at the November meeting was partially offset by the “case to wait and assess the effects of [prior] stimulus”. Members suggested that a reduction in November could have a “different effect on confidence than in the past”. In our view, this alludes to the idea that the RBA are likely less inclined to cut the official cash rate, currently at 0.75%, putting it within arm’s reach of negative territory. Instead, the RBA may be subtly hinting at the potential use of some form of QE in Q1 2020. Overall, we think it’s highly unlikely we see a Dec. rate cut of any sort despite the marginal tick higher in Dec. rate cut pricing and see near-term support for AUDUSD dips.

PM Johnson vs Corbyn debate in session

While this event is unlikely to cause any significant GBPUSD price action, we’d be remiss not to treat it as an interesting event given it could impact election polling. The television debate is scheduled for 8pm LT and will run for one hour. As mentioned in our ASIA MORNING: Election Outlook Drives GBP Outperformance, Sterling price action remains highly correlated to expectations in the forthcoming Dec. 12 UK election. Market expectations are currently set for Conservatives to sustain their parliamentary majority. Positioning among our clients is marginally short presently which makes sense given momentum looks exhausted trading into 1.3. We think however this could turn as the calendar approaches Dec. 12 given our medium-term GBPUSD bullishness.

Dec. rate cut still unlikely despite dovish RBA minutes

AUDUSD was offered 20pips on the RBA’s release of November Minutes but has since edged back up above 0.68 following a slight uptick in broad risk sentiment. Most of the statement read in line with prior releases but there were some lines of interest that rubbed off as dovish on the reader. Importantly, the Board noted that the case to ease monetary policy at the November meeting was partially offset by the “case to wait and assess the effects of [prior] stimulus”. Members suggested that a reduction in November could have a “different effect on confidence than in the past”. In our view, this alludes to the idea that the RBA are likely less inclined to cut the official cash rate, currently at 0.75%, putting it within arm’s reach of negative territory. Instead, the RBA may be subtly hinting at the potential use of some form of QE in Q1 2020. Overall, we think it’s highly unlikely we see a Dec. rate cut of any sort despite the marginal tick higher in Dec. rate cut pricing and see near-term support for AUDUSD dips.

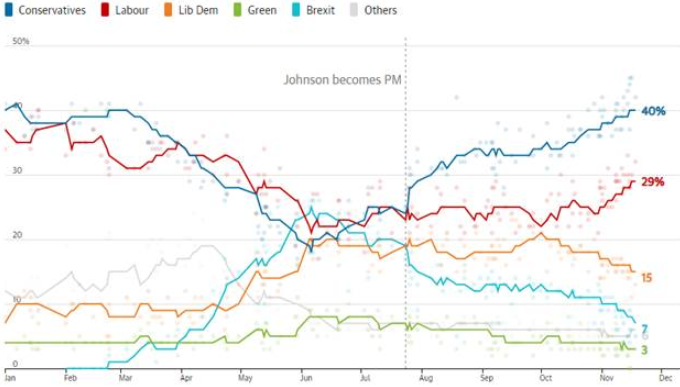

PM Johnson vs Corbyn debate in session

While this event is unlikely to cause any significant GBPUSD price action, we’d be remiss not to treat it as an interesting event given it could impact election polling. The television debate is scheduled for 8pm LT and will run for one hour. As mentioned in our ASIA MORNING: Election Outlook Drives GBP Outperformance, Sterling price action remains highly correlated to expectations in the forthcoming Dec. 12 UK election. Market expectations are currently set for Conservatives to sustain their parliamentary majority. Positioning among our clients is marginally short presently which makes sense given momentum looks exhausted trading into 1.3. We think however this could turn as the calendar approaches Dec. 12 given our medium-term GBPUSD bullishness.