{kind=link}

- The US and China last night completed ‘phase one’ of a bigger trade deal, requiring Chinese purchases of US agricultural goods, some intellectual-property and currency measures and access for US financial services in return for US refraining from next week’s planned tariff hike on USD250bn of Chinese goods.

- The two sides will now have to write down the trade deal over the next three to five weeks possibly followed by a signing ceremony at the APEC meeting 16-17 November. Chinese media, while noting progress, warned not to be ‘overly optimistic’ about the prospects for future negotiations.

- The completion of ‘phase one’ of the trade deal could likely boost market confidence further near-term as it removes some uncertainty, but it will not be a game changer for the global economy in our view.

- Although negotiations of ‘phase two’ are expected to commence in November, we still think there are significant hurdles for a more comprehensive deal.

- In FX markets, the temporary boost in market confidence provides an opportunity to position for further broad dollar strength.

US-China reaches partial deal

Almost 18 months after the US-China trade fight began, the two sides late last night reached a partial trade deal. As part of the deal, China would significantly step up purchases of U.S. agricultural commodities, likely buying about USD 40 to 50 billion worth of products, agree to certain intellectual property measures and concessions related to financial services and the functioning of the Chinese currency market, Trump said Friday at the White House. In return for the Chinese concessions, the US will not implement the planned tariff hike next week.

The agreement is expected to take three to five weeks to put on paper, which will allow the leaders of the two countries to most likely formally sign the agreement at the APEC meeting in Chile on 16-17 November 2019. Importantly, Trump said the deal was the first phase of a broader agreement. Following the signing of ‘phase one’ the negotiations of ‘phase two’ will begin immediately, according to Trump.

While the trade deal could boost risk sentiment near-term, it will not be a gamechanger for the global economy. Financial markets will breathe a sigh of a relief as the deal removes some of the tail risk of a full-blown trade war between the two sides. On Friday night, US stock markets rose a little more than 1% as rumours spread that the US and China had reached a partial deal, while US yields fell back after increasing immediately after the announcement of the agreement.

However, we do not think the deal will be a major game-changer for the global economy. Although the commitment to buying US agricultural goods was slightly larger than expected, the size of the deal is fairly limited.

Moreover, the deal just avoids next week’s tariff hikes but does not reduce any of the tariffs put in place over the last 18 months, let alone cancel the US tariff hikes planned for December. While we are cautiously optimistic that the two sides can agree on putting the deal together on paper, there are risks of negotiations stalling again in the next four to five weeks with possible tensions escalating again. According to Chinese media, the Chinese side also struck a more cautious tone with the official Economic Daily social media account stating that while negotiators had made efforts to make progress they should not be ‘overly optimistic’ about the prospects for future negotiations.

All in all, we do not think the deal will provide a lasting boost to the global economy at this stage – here the easing by global central banks is far more important near-term (and yesterday’s deal may influence the Fed in a slightly more hawkish direction). However, it may still to some extent help the emerging economic stabilisation that we are seeing in China, which will also at some stage benefit the rest of the global economy.

Why a real deal is difficult – but not impossible

We still believe the US and China are far from reaching a comprehensive trade deal. The signals from China have been that 80% of US demands have been met, but the last 20% is an infringement of Chinese sovereignty and would compromise China’s development model. These ‘phase two’ negotiations would have to focus on intellectualproperty theft, forced technology transfer and US complaints about Chinese industrial subsidies. China also wants tariffs to be rolled back in full as part of a big trade deal. Trump, on the other hand, has said he would only take a deal if it were a ‘big deal’. Otherwise, he is happy without one.

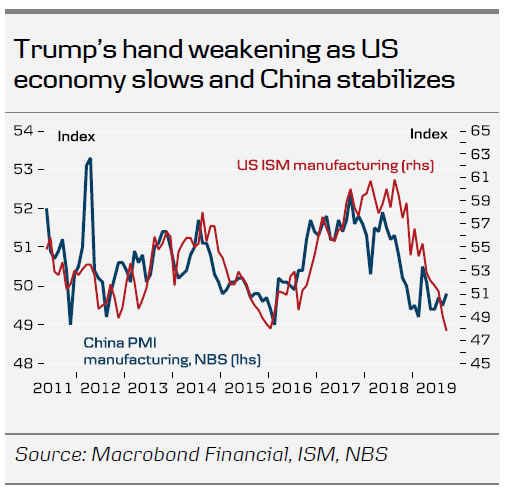

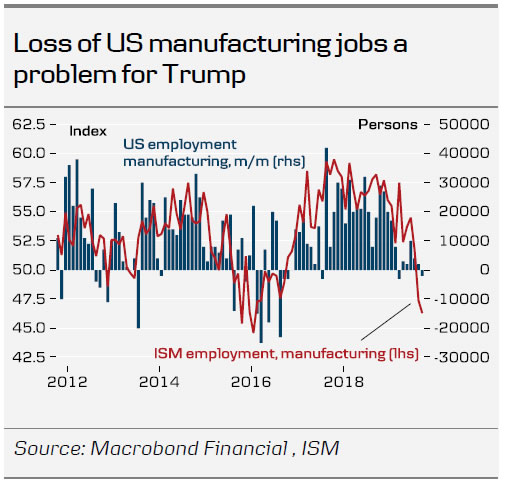

However, there is still a possibility that he would give in next year when the November presidential election moves closer. His hand is weakening currently as the US economy is slowing down and manufacturing jobs are going down again. Farmers are also under a lot of pain and he needs to deliver a permanent solution for them in order to make them happy. A permanent trade deal could reverse the loss of manufacturing jobs and give a large boost to US farmers. The impeachment process, however, is a new big unknown factor in relation to the prospect of a deal. If Trump ends up impeached, it is highly uncertain how this would affect his actions and priorities.

Overall, our baseline scenario is still one of no-deal ahead of the US election. However, a lot of things are in play; it can still go both ways and yesterday’s deal could be a new start (but with implementation risks).

FX: An opportunity to position for further broad dollar strength

Following the trade deal between China and the US, we see room room to price in more optimism in markets but expect improved risk sentiment to fade over the coming week(s). We thus advice to utilize this as an opportunity to position for further broad dollar strength and weaker Scandies vs. euro and dollar. For corporate clients and depending on the FX exposure, this could be attractive levels to lock in hedging ratios for the remainder of Q4. Similarly, investors could consider adding new shorts on Scandies (we favour short SEK).

Over last week, markets have already moved from a quite pessimistic to a decently but not overly optimistic stance. In our view, there is room to price in further optimism over this week via lower EUR/SEK, EUR/NOK and higher EUR/JPY whereas EUR/USD has likely already priced most of what can be expected. The fundamental macro situation remains fragile and we have yet to get to point where we think the trends of the previous 1-1½ years are turning, see also the macro comment above.