{kind=link}

The Japanese yen was relatively unchanged after some mixed data from the country. The unemployment rate in August remained unchanged at 2.2%. This was slightly better than the 2.3% that traders were expecting. The jobs to applications ratio for August remained unchanged at 1.59. The Tankan big manufacturing outlook index was at 2, which was better than the expected 1. The large manufacturers index for the third quarter was at 5, which was lower than the expected 2. The Tankan large non-manufacturers index declined to 21 from the previous 23. Nearby in South Korea, the country’s exports declined by 11.7% while imports declined by 5.6%. The two countries have been having a so-called mini trade war.

The Australian dollar rose – and then pared the gains – after the interest rates decision by the Australian central bank. As was widely expected, the bank slashed interest rates by 25 basis points. In the accompanying statement, the central bank said that rates could remain lower for an extended period of time. The Australian economy is widely sensitive to the global economy because most of its goods are shipped to China. The bank expects inflation to be slightly below the 2.0% target in 2020 and slightly above the 2.0% target in 2021.

Later today, traders will receive the nationwide house price index (HPI) for September. The index is expected to decline from 0.6% to 0.5%. On a MoM basis, the HPI is expected to increase by 0.1%. From Germany, the market will receive the manufacturing PMI. This is expected to decline from 43.5 to 41.4. If it does, it will be a sign that the German economy could slide into a recession, which will lead to more calls for fiscal policy measures. Traders will also receive the CPI data from the European Union. The headline CPI is expected to remain unchanged at 1.0% while the core CPI is expected to increase from 0.9% to 1.0%.

In Canada, traders will receive the July GDP data. In the month, the economy is expected to have declined from 0.2% to 0.1%. From the US, traders will receive the ISM manufacturing PMI data, which is expected to show an increase from 49.1 to 50.4. There will also be a lot of talk from central banks today. ECB president, Mario Draghi, Buba president Weidmann, Fed member Bullard, and Bowman will make speeches.

EUR/USD

The EUR/USD pair declined to a low of 1.0895 as the fourth quarter started. On the hourly chart below, this price is slightly below the 28-day and 14-day moving averages. The RSI has remained slightly above the oversold level of 30 while the on-balance volume has continued moving lower. The pair is now trading at the lowest level since 2017. As the new quarter starts, the pair could continue moving lower as it heads to 1.0340.

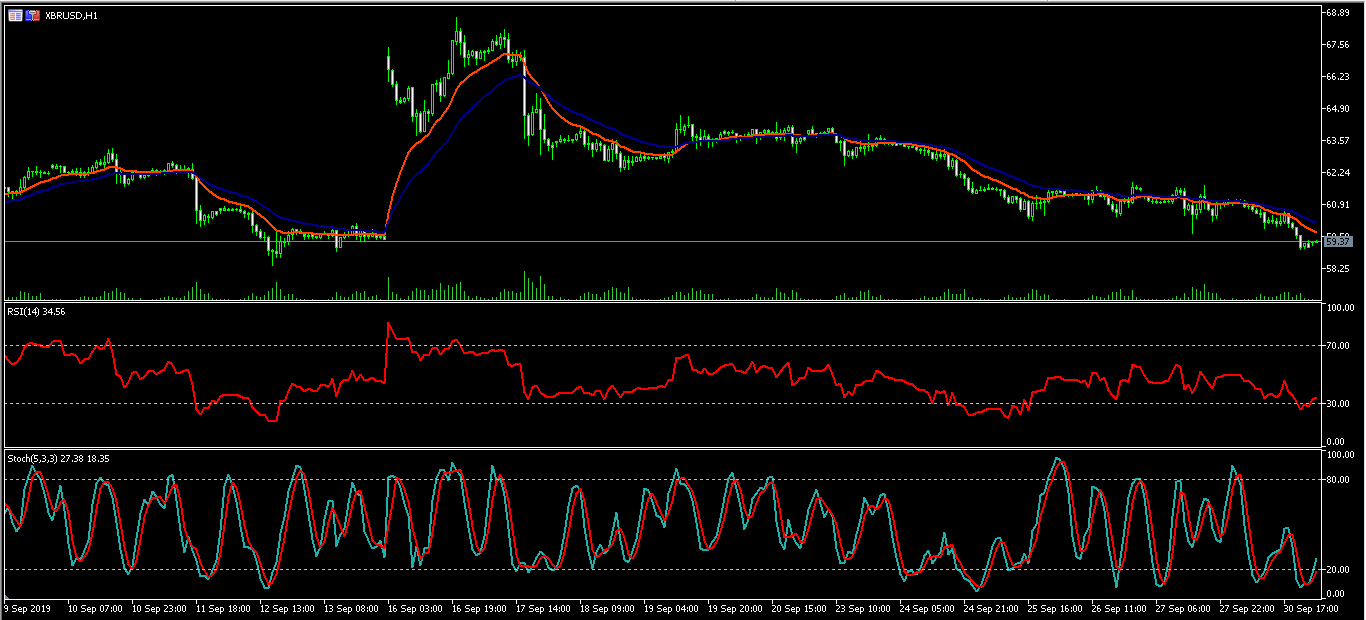

XBR/USD

The price of Brent crude oil declined yesterday to a low of $59. On the hourly chart below, the XBR/USD pair is trading below the 14-day and 28-day moving averages. The RSI has moved slightly above the overbought level. The same is true with the stochastic oscillator. The pair will likely continue to move lower to test the important support of 58.40.

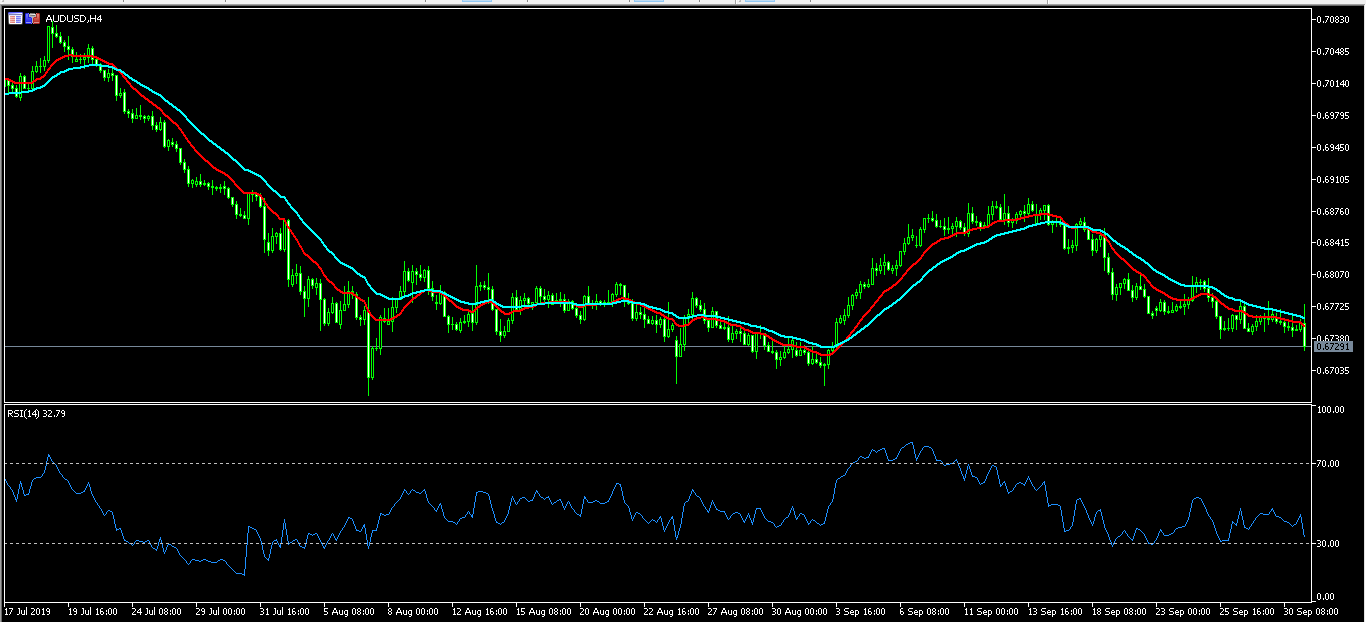

AUD/USD

The AUD/USD pair pared the initial gains after the RBA delivered its interest rates decision. The pair rose to a high of 0.6775 and then declined to a low of 0.6725. On the four-hour chart, the pair has been on a strong downward trend after reaching a high of 0.6896 in September. The price is below the short and medium-term moving averages while the RSI has declined to almost 30. The pair will likely continue moving lower to test the previous low of 0.6690.