{kind=link}

The Canadian dollar started the week gaining versus the US dollar. The comments from Bank of Canada (BoC) policy makers on June 11 had pushed the loonie higher against the greenback, but the Fed turned up the rhetoric last week to even things out. Fed members were mixed in their endorsement/criticism of the aggressive rate hike path, but most were in agreement that the central bank needs to start shrinking its massive balance sheet. The trillions of dollars which were accumulated as part of the Fed’s quantitive easing program and are still in the books of the CB need to be sold in a gradual manner for true normalization to be achieved.

The week started with few economic indicators to guide the market. New orders for US durable goods in May fell by 1.1 percent month to month, removing transportation items also disappointed with a 0.1 percent gain when 0.4 percent was expected. Second quarter growth has proven sluggish and the durable goods data hit the USD to the downside. The main champion for the dollar has been the Fed and this week there will be plenty of fedspeak to digest with three Federal Open Market Committee (FOMC) members due to speak on Tuesday.

Oil prices are higher on the North American session than last week. This all could change with the release of the US crude inventories on Wednesday at 10:30 am EDT. The OPEC oil production cut agreement has failed to spark a rally in energy prices when US and other non-agreement producers are ramping up their supply keeping the crude glut in place.

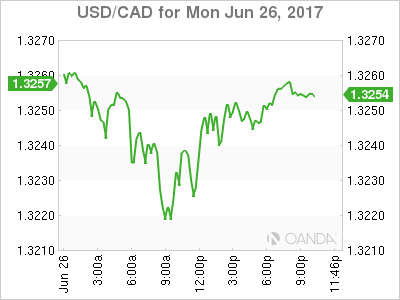

The USD/CAD lost 0.253 percent in the last 24 hours. The currency pair is trading at 1.3237 after a disappointing US durable goods number early on Monday. The final reading of the US second quarter GDP will be released on Thursday, June 28 at 8:30 am EDT with growth now expected to be lower than the 1.2 percent gain reported last month.

Bank of Canada (BoC) Governor Stephen Poloz will be in Europe this week to attend the European Central Bank (ECB) Forum in Portugal. He will be joined in a panel by the heads of the Bank of England (BoE), Bank of Japan (BOJ) and the host. At this stage the BOJ stands apart as the other have made hawkish statements about their respective economies being on the mend with rate hikes and end of QE programs to start this year. In Canada the comments from Deputy Governor Carolyn Wilkins in Winnipeg put a rate hike firmly on the table for this year. The weak inflation data on Friday is not expected to derail an upcoming hike, but it could have pushed it further back towards the fourth quarter or later.

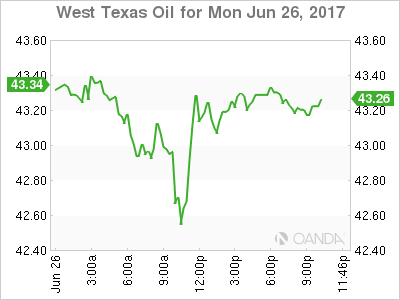

Crude gained 0.799 percent in the last 24 hours. West Texas Intermediate is trading at $43.27 near daily highs after a slow start to the week. Energy prices managed to trade above the $43 price line awaiting the weekly inventory data that tells the score between the Organization of the Petroleum Exporting Countries (OPEC) production cuts and the US ramp up of supply.

Energy prices touched 7 month lows last week and market sentiment is expecting another drop, specially if inventories of crude or gasoline in the US show another large buildup. US production has grown by about 10 percent with Brazil and Canada also increasing output, while the OPEC is now considering further cuts to keep prices from falling further.

Market events to watch this week:

Tuesday, June 27

10:00 am USD CB Consumer Confidence

Wednesday, June 28

10:30 am USD Crude Oil Inventories

Thursday, June 29

8:30 am USD Final GDP q/q

8:30 am USD Unemployment Claims

Friday, June 30

4:30 am GBP Current Account

8:30 am CAD GDP m/m