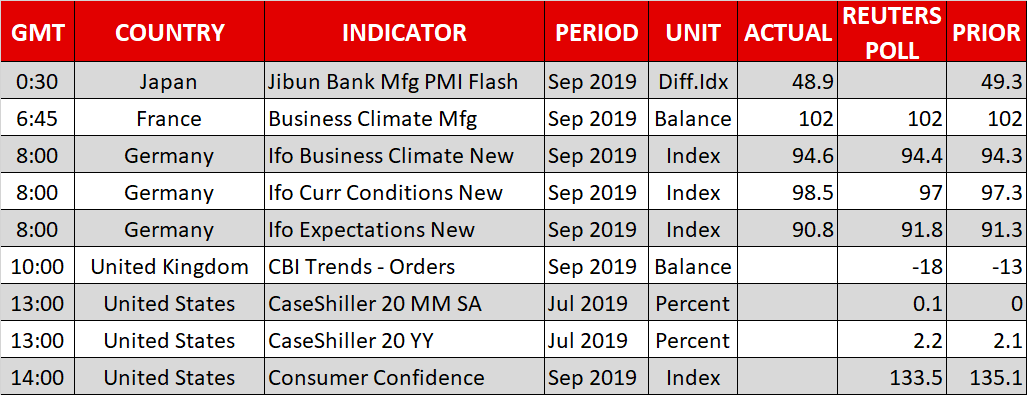

{kind=link}

- UK Supreme Court rules at 09:30 GMT whether Parliament’s suspension was lawful – upside risk for sterling?

- RBNZ rate decision due early on Wednesday; kiwi may briefly spike higher

- US stocks recover after upbeat manufacturing PMI, but safe havens tell another story

UK Supreme Court to rule on Johnson’s suspension of Parliament

It will be an eventful day in Britain, as the nation’s Supreme Court will decide whether Boris Johnson’s choice to suspend Parliament for five weeks was lawful, or not. For the pound, this may represent a substantial upside risk. To explain – if the judges rule the suspension was perfectly lawful, then nothing changes and UK lawmakers stay home until October 14. That may weigh on the pound, but only slightly, as this is already the status quo.

However, it the Court decides that Boris acted unlawfully, then there are a range of possible outcomes, most of which seem positive for sterling. For instance, the Supreme Court could compel Parliament to return, which would further weaken Johnson’s ‘no-deal negotiating’ hand, reducing the risk of a disorderly Brexit. In a more extreme scenario, Johnson could resign and a General Election might be called sooner, which also argues for a relief rally in the pound given the prospect of a ‘pro-remain’ coalition government.

RBNZ to keep its rate powder dry – can the kiwi get off the floor?

The Reserve Bank of New Zealand (RBNZ) will announce its rate decision during the Asian session on Wednesday, at 02:00 GMT. Economists expect no change in policy after the central bank slashed rates by a half-point at its previous meeting, but markets are not as certain, assigning a ~20% probability for a surprise quarter-point rate cut.

Even though the domestic economy continues to struggle, with business confidence remaining stubbornly low in the midst of the trade war, the RBNZ is still unlikely to act again so soon. Given their bold action last time, policymakers can afford to take a step back and monitor how the economy fares and how the trade talks play out, before deciding whether and when to act again.

Assuming the RBNZ stands pat, then the kiwi may spike higher on the decision as those looking for an immediate cut are disappointed. That said, the central bank will almost certainly keep the door wide open for more action at the November meeting, so any gains may be only modest. In the bigger picture, the kiwi is comfortably the worst-performing major currency so far this year, and whether it manages to get off the floor will depend mostly on how the US-China talks unfold in early October.

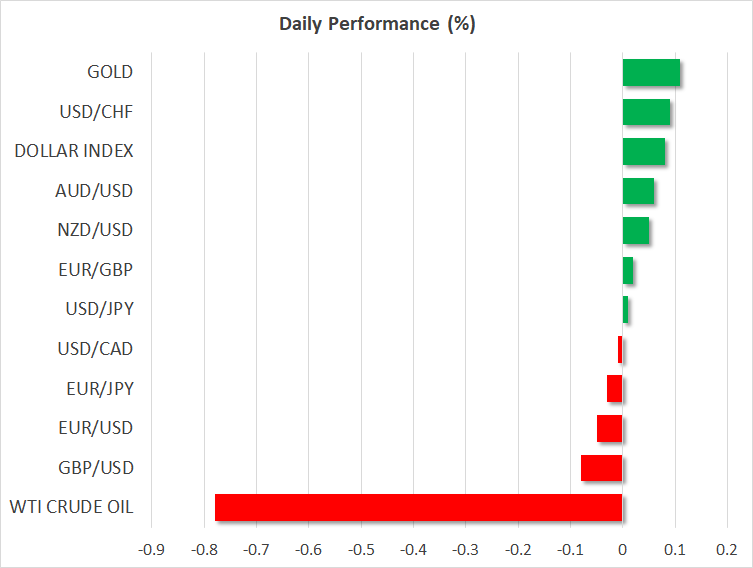

US stocks claw their way back, but gold firms

In the broader market, US stocks recovered some early losses to close virtually unchanged yesterday, seemingly shrugging off the risk of a recession in the euro area. The recovery was helped by a stronger-than-expected US Markit manufacturing PMI for September, which calmed some nerves about the health of the American economy.

Yet, in a sign that concerns about the global outlook are alive and kicking, gold prices climbed despite a stronger dollar, which typically weakens demand for bullion by making it more expensive to buy for investors using foreign currencies.

Similarly, the Japanese yen and Swiss franc outperformed in the FX market as investors turned more defensive. Euro/franc is now near its recent lows again, raising the question of whether the SNB will step into the market soon to keep the Swiss currency from appreciating any further.