{kind=link}

Improving European manufacturing balanced euro against dollar

The dollar is mixed against major pairs after a week where Fed speakers offered a mixed narrative. The majority of policy makers agree that the massive balance sheet accumulated during the quantitative easing program from the US central bank should start shrinking sooner rather than later. The point of debate remains the number of rate hikes in the horizon, with St. Louis Fed President James Bullard calling it "unnecessarily aggressive" and the CME FedWatch tool showing a 50 percent probability of a hike in December.

Flash manufacturing purchasing manager surveys boosted the euro on Friday with improvements in France, Germany and Europe overall. The German Ifo business survey released on Monday, June 26 at 4:00 am EDT could be inline with the perception of European recovery even as inflation struggles to gain momentum. The European Central Bank (ECB) forum will also kick off on Monday with plenty of speaking opportunities for President Mario Draghi. The European calendar will close with inflation data on Thursday and Friday expected with little improvement as the market ponders what the next move will be for the ECB before the end of the year which could include a rate hike, the start of QE tapering or both at the same time.

The US calendar will feature events like the release of core durable goods orders on Monday, June 26 at 8:30 am EDT. The Conference Board’s Consumer Confidence index on Tuesday, June 27 at 10:00 am EDT which is expected to have declined slightly from last month and the Final Q1 GDP release on Thursday, June 29 at 8:30 am EDT confirming the slowdown of the economy in the first quarter compared to the last two periods of 2016. Hopes for tax reform and infrastructure spending in 2017 have faded and with it the possibility of a 3 percent GDP growth this year putting downward pressure on the USD.

The EUR/USD gained 0.037 percent in the last five days. The single pair is trading at 1.1202 and will end the week near where it started on Monday. There was little in the way of economic releases that involved the pair. European manufacturing flash PMI data on Friday helped the EUR overcome the USD strength from Fed member comments suggesting the US central bank will raise the interest rate more this year. Economic fundamentals in the US have been questionable but the resolve of the Fed remains solid. Europe on the other hand is riding a wave of optimism form strong data and a reduction of political risk after the Emmanuel Macron victory in the French elections.

The last week of June will be devoid of major indicators with the spotlight once again directed at US political drama with only the German Ifo business climate survey to give insight into Europe.

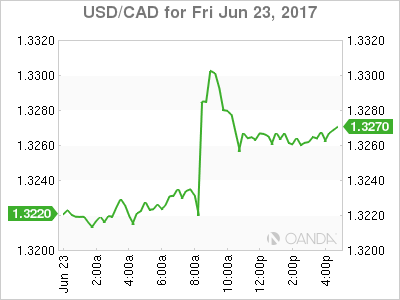

The USD/CAD gained 0.275 percent on Friday. The currency is trading at 1.3263 after a disappointing CPI reading of 0.1 percent putting inflationary pressures at a slow pace. The soft inflation data reduced the possibility of a July interest rate hike by the Bank of Canada (BoC).

The loonie is being guided by X factors. 1)The price of oil has historically shared a strong correlation given the importance of the commodity as part of GDP. Oil prices have been weaker as low demand has been met with steady supply creating a glut. 2)NAFTA renegotiations are hovering over the currency as the Trump administration started the process in a combative mode. Three quarter of Canadian exports go to the United States and a change in that trade relationship would be significant on either direction. 3) Monetary policy winds have shifted starting the Fed. Single rate hikes per year in 2015 and 2016 have been followed by 2 rate hikes this year by the Fed putting the Fed funds rate in a 100-125 basis points. The BoC first put another rate cut off the table earlier in the year as the economy had a strong first quarter and hints of a continuation of the trend in the second quarter triggered the hawkish comments. Rising household debt could trump weak inflation as the central bank would rather introduce gradual change to avoid a sudden impact to Canadians.

The USD/CAD has gone from a high of 1.3350 to a low of 1.3220 after the BoC comments only to slowly climb back as Fed speakers have mostly been repeating the same comments. More rate hikes coming and a reduction of the balance sheet sooner rather than later. Only a few dovish members have strayed from those comments, and even then only walking back the aggressive rate hike path, but agreeing on the need to reduce the 4 trillion accumulated during its quantitative easing program.

The price of energy fell 4.184 percent in the last 24 hours. West Texas Intermediate is trading at $42.79 due to oversupply concerns. The weakness of the USD has kept the price of oil near the $42 price level, but growing supply from US producers has been offsetting the effect of the oil production cut extension between OPEC and other major producers.

Oil started the week around the $44.59 price level before losses accumulated on a daily basis and not even the drawdown of US crude inventories on Wednesday was enough to reverse the trend. Uncertainty about the stability of the Organization of the Petroleum Exporting Countries (OPEC) after the appointment of the new Saudi Arabia crown prince did not boost prices as OPEC members Libya and Nigeria have sorted their supply disruptions leaving the market still caught in a glut of crude.

Market events to watch this week:

Monday, June 26

- 4:00 am EUR German Ifo Business Climate

- 8:30 am USD Core Durable Goods Orders m/m

- 1:30pm EUR ECB President Draghi Speaks

Tuesday, June 27

- 10:00 am USD CB Consumer Confidence

- 1:00pm USD Fed Chair Yellen Speaks

Wednesday, June 28

- 10:30 am USD Crude Oil Inventories

Thursday, June 29

- 8:30 am USD Final GDP q/q

- 8:30 am USD Unemployment Claims

Friday, June 30

- 4:30 am GBP Current Account

- 8:30 am CAD GDP m/m

*All times EDT