{kind=link}

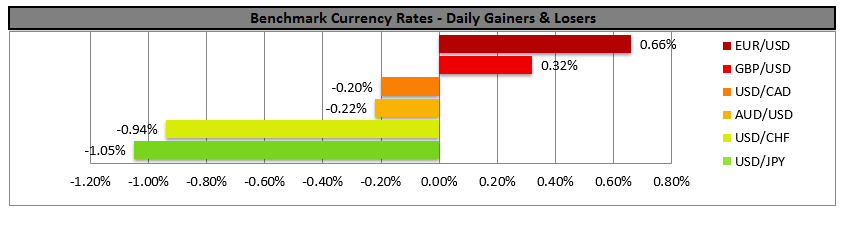

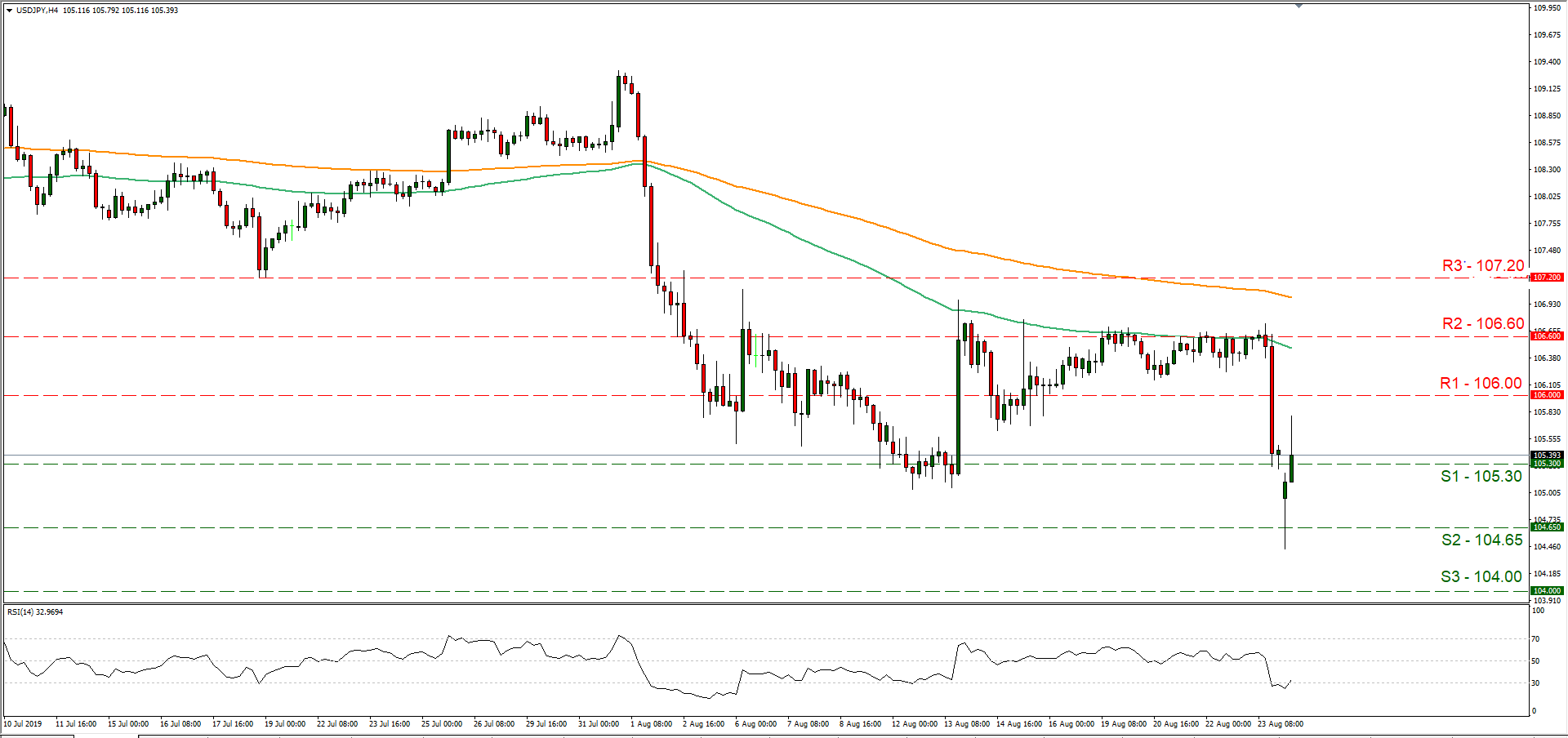

The USD tumbled against a number of its counterparts on Friday as the US-Sino trade war escalated further. The escalation started as China announced counter-tariffs on imports from the US yet the US President was quick to respond by telling US companies that they need an alternative to China and threatening with additional tariffs. It should be noted that early during today’s Asian session, the Chinese Vice President stated that China wants to a “calm” resolution of the dispute through negotiations, which could ease tensions somewhat, yet that remains to be seen. Please note that the event overshadowed a speech by Fed’s Chair Jerome Powell, in which no further stimulus was announced, yet he stated that the US economy is in a “favourable place” and that the Fed would “act as appropriate” to keep economic expansion on track. It should be noted that the US President tweeted that the Fed was doing nothing, after the speech. We expect volatility to continue and should tensions start easing a bit, we could see safe havens weaken. USD/JPY tumbled on Friday yet recovered some ground during today’s Asian session and currently is trading just above the 105.30 (S1) support line. Please note that the pair had scored a yearly low in today’s early Asian session. We could see the pair maintaining a sideways motion, yet should trade tensions ease somewhat, we could see the pair rising. Should the pair’s long positions be favoured by the market, we could see the pair breaking the 106.00 (R1) resistance and aim for higher grounds. Should the pair come under the market’s selling interest, we could see it breaking the 1105.30 (S1) support line and aim for the 104.65 (S2) support level.

Oil prices drop as trade tensions rise

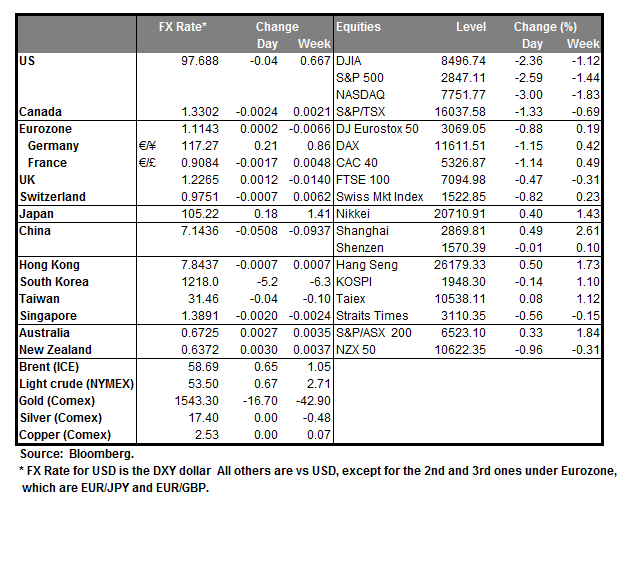

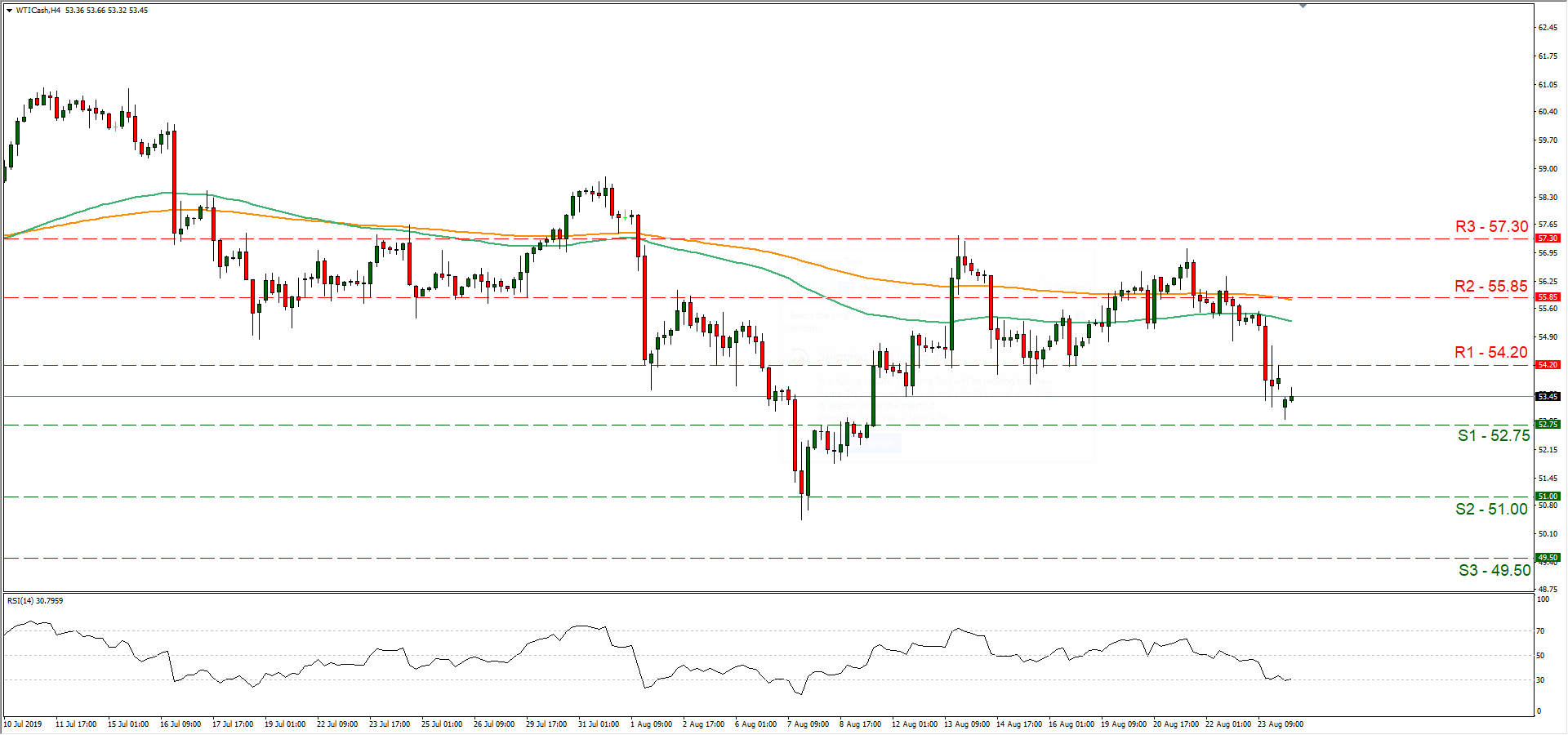

Oil prices dropped on Friday and during the Asian session today opened with a negative gap as trade tensions increased fears of a possible recession. Concerns about a global economic slowdown are fuelled by the ratcheting up of the trade war between the United States and China. Analysts tend to note that the price of the oil could get lift should there be talks between the two countries, however that could prove to be very difficult. It should also be noted that the US oil rig count dropped on Friday as well diming expectations for oil demand. We could see oil prices drop further in the next few days should there be no improvement in the US Sino relationships or a fundamental shift. WTI prices dropped on Friday breaking the 54.20 (R1) support line, now turned to resistance. We could see the commodity’s prices maintaining a sideways motion, yet should tensions escalate, we could see them drop once again. Should the bears dictate WTI prices we could see them breaking the 52.25 (S1) support line and aim for the 51.00 (S2) support barrier. Should the bulls take over, we could see the commodity’s prices breaking the 54.20 (R1) resistance line and aim for the 55.85 (R2) resistance hurdle.

Other economic highlights today and early tomorrow

Today we expect Germany’s IfO Business Climate for August and the US Durable goods orders for July.

As for the week ahead

On Tuesday, we Germany’s 2nd GDP rate for Q2 and the US CB Consumer Sentiment for August. On Wednesday, we get from Germany the GfK Consumer Sentiment for September. On a busy Thursday, we get New Zealand’s Business confidence, Australia’s Capex Germany’s employment data and Germany’s preliminary HICP for August and the 2nd estimate of the US GDP growth rate for Q2 . On Friday, we get Eurozone’s preliminary HICP for August, the US consumption rate and Canada’s GDP rate for June. On Saturday, we get China’s NBS Manufacturing PMI for August.

USD/JPY H4

Support: 105.30 (S1), 104.65 (S2), 104.00 (S3)

Resistance: 106.00 (R1), 106.60 (R2), 107.20 (R3)

WTI H4

Support: 52.75 (S1), 51.00 (S2), 49.50 (S3)

Resistance: 54.20 (R1), 55.85 (R2), 57.30 (R3)