{kind=link}

It will be a decisive week for the US dollar, with the minutes of the latest Fed meeting being released on Wednesday (18:00 GMT), before Fed chief Jay Powell delivers remarks at the Jackson Hole symposium on Friday (14:00 GMT). Since the minutes won’t reflect the latest escalation in trade, they could appear slightly hawkish relative to current market pricing, lifting the dollar. Any gains may remain short-lived though, if Powell opens the door for a prolonged easing cycle.

Market concerns about the US economic outlook have risen lately, as another escalation in the trade conflict, combined with a deteriorating global environment, are fueling fears of a recession. While American economic data remain decent, Trump’s recent decision to introduce more tariffs on China has elevated uncertainty, leading investors to price in even more aggressive Fed rate cuts on expectations that policymakers will try to safeguard the economy.

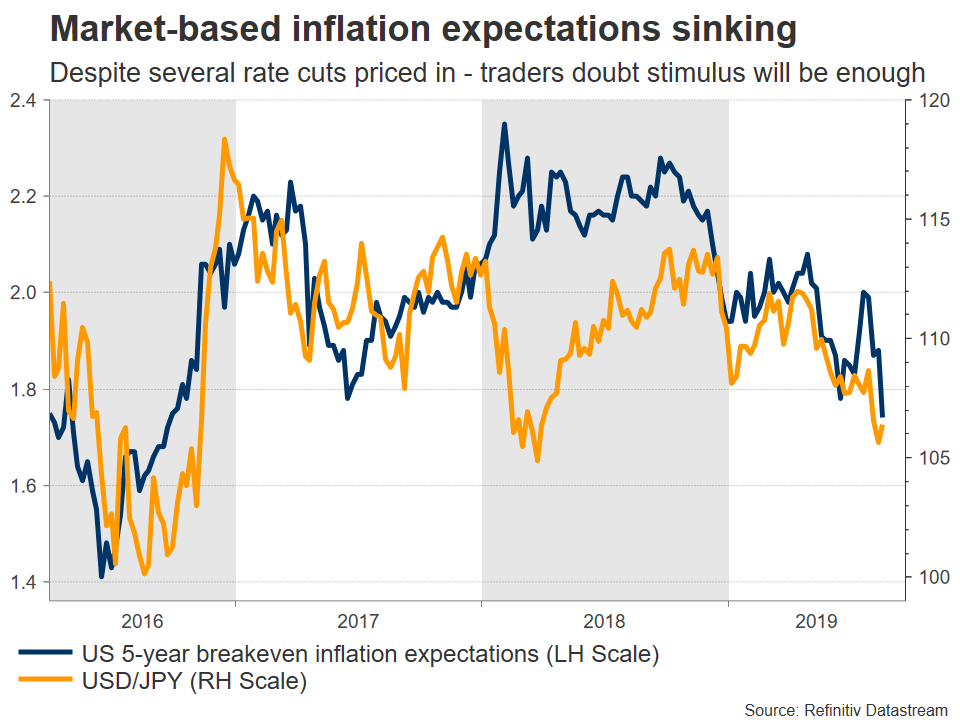

Similar to the story before the July meeting, traders are now ‘certain’ that the Fed will cut again in September – the question is how deep the cut will be. A quarter point rate cut is fully priced in, with markets also assigning a ~15% chance for a bigger, half-point move. In total, markets expect a full percentage point of rate reductions by July 2020. Despite all this easing being factored in though, inflation expectations remain low – a sign that traders don’t believe the stimulus will be enough to lift inflation back to 2% anytime soon.

Turning to this week’s events, the minutes of the July meeting could be seen as slightly hawkish by the markets. The gathering took place before trade tensions escalated, so they may paint a picture of a Committee that is not fully on board with cutting rates aggressively. Recall that two officials voted against cutting rates in July and the minutes could show more policymakers skeptical of future action, since the risks were not as severe back then. A not-so-dovish tone could push the dollar somewhat higher, as the probability for a half-point cut in September declines.

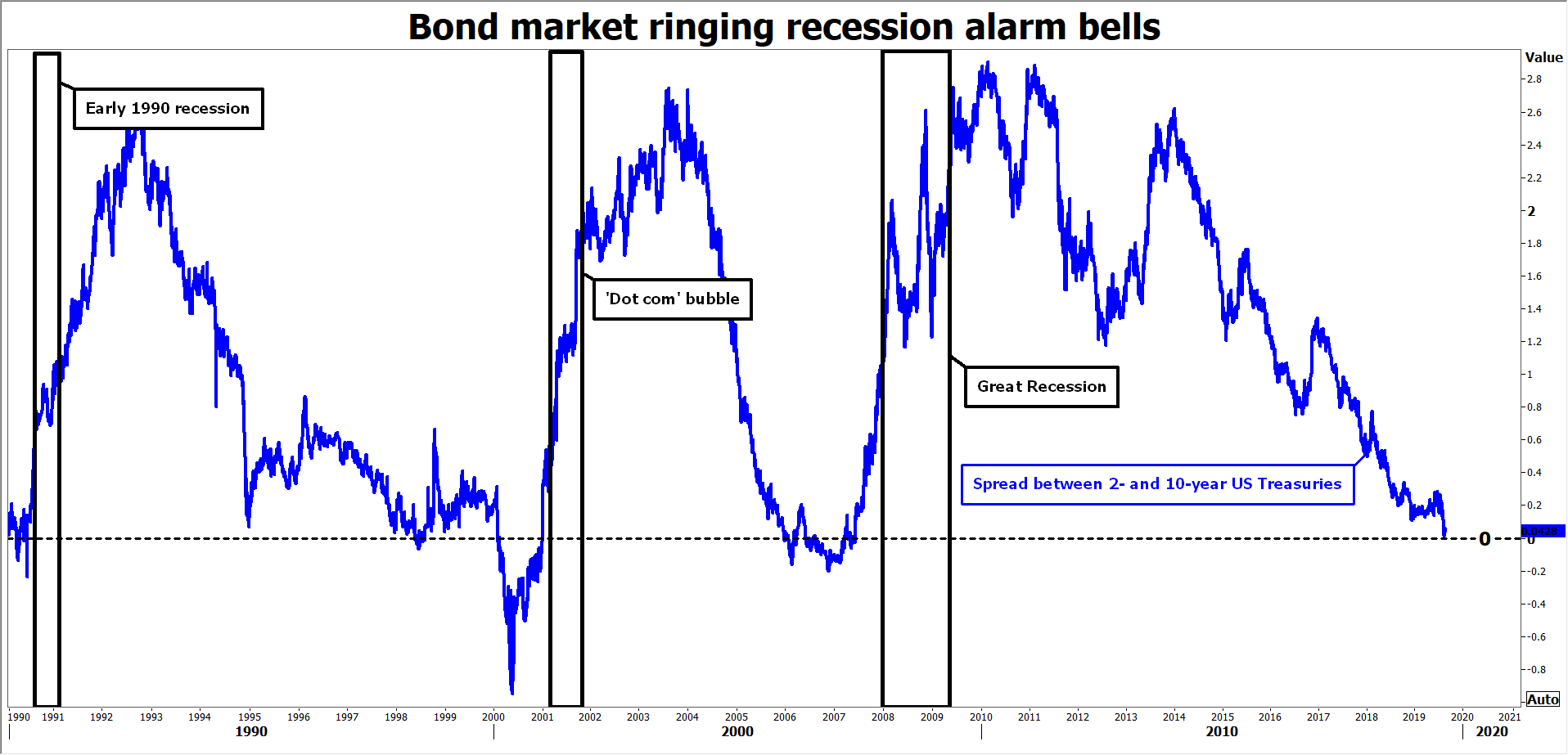

Any gains may not be sustained for long though, as Chairman Powell’s speech on Friday represents a huge risk. He was reluctant to commit to prolonged easing of policy back in July, labelling the rate cut as an “insurance” move instead, but things have changed since then. Trade uncertainty has skyrocketed, economic data from Germany to China have weakened, and the US bond market is flashing recession signals.

The question therefore is, will Jay Powell change his tune this time and indicate that a series of cuts are possible over the coming months amid mounting risks, or will he stick to his ‘one cut at a time’ mantra and repeat that this is not necessarily the start of a protracted easing cycle?

It’s a very close call, but Powell may have more incentive to lean in a dovish direction here and open the door for the Fed to ease more powerfully than previously indicated, calming markets. Anything short of that could be interpreted as the Fed falling further ‘behind the curve’ and therefore amplify concerns of a policy mistake, making a bad situation even worse.

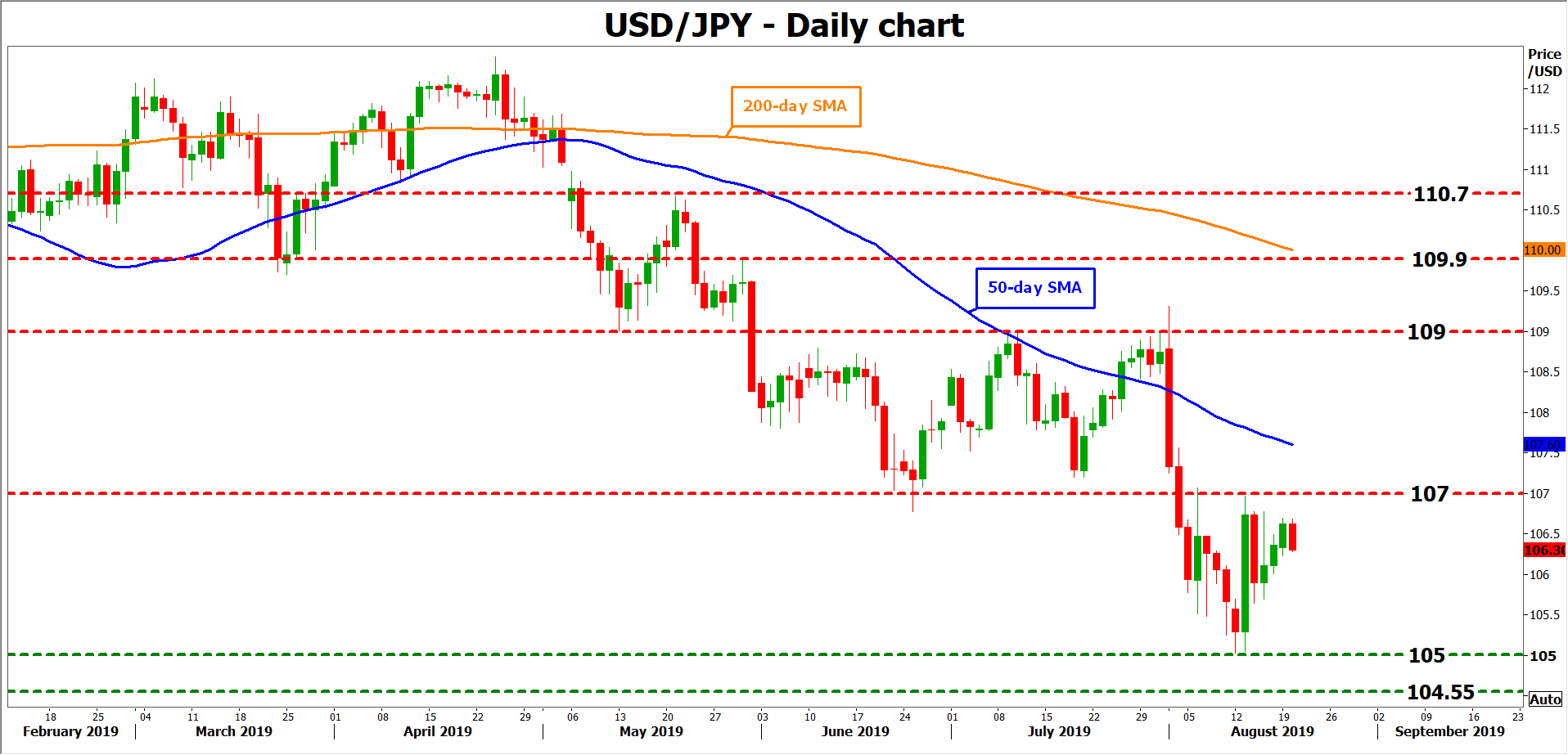

Taking a technical look at dollar/yen, a potential break above 107.00 may open the door for a test of the 109.00 region.

On the flipside, another wave of losses could find support near the 105.00 handle, where a bearish violation would turn the focus to the 2018 low of 104.55.