{kind=link}

Employment numbers out of Canada will be in focus on Friday at 12:30 GMT. As most other central banks rush to join the global rate cut frenzy, the jobs data will be watched closely for clues on whether the Bank of Canada is any closer to adopting an easing bias. However, despite the Bank of Canada’s neutral stance looking increasingly out of step with the rest of the world, the Canadian dollar has been on the slide since late July, falling to 7-week lows versus the greenback in recent days.

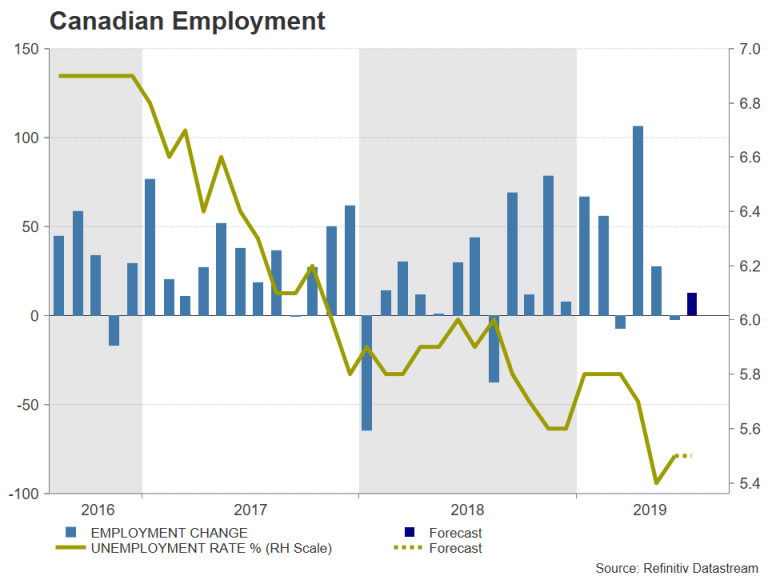

Canada’s growth momentum has improved

The Canadian economy has picked up momentum in recent months even as most other advanced economies struggle under the weight of global trade frictions. One important contributor to the improving growth picture has been the strong labour market. The nation’s unemployment rate is the lowest since the mid-1970s, reaching 5.4% in May before edging up to 5.5% in June.

Jobless rate to remain steady in July

For July, the jobless rate is anticipated to hold at 5.5% but total employment is forecast to rise by 12.5k after a surprise 2.2k drop in June. However, the weakness in June was attributed to a fall in part-time employment and full-time jobs rose by a solid 24.1k. Moreover, average hourly wages jumped to a one-year high of 3.6% year-on-year in June, pointing to a tight labour market.

If wages continue to head higher, that would make it difficult for the BoC to risk cutting interest rates pre-emptively to cushion the economy from the global headwinds, especially with inflation running at 2% y/y. However, in its last assessment at the July 10 policy meeting, the Bank was keen to stress that the current uptick in inflation was likely to be temporary and placed greater emphasis on the worsening trade conflict.

BoC willing to look through temporary inflation rise

This suggests the BoC would be willing to look through a brief overshoot of inflation above its 2% target if it thinks a more accommodative monetary policy would be necessary to support growth. The market reaction therefore to the incoming data ahead of the September 4 policy meeting is likely to be somewhat limited as investors will want to wait and see to what extent policymakers’ views will have changed following the significant escalation in the US-China trade row over the past week.

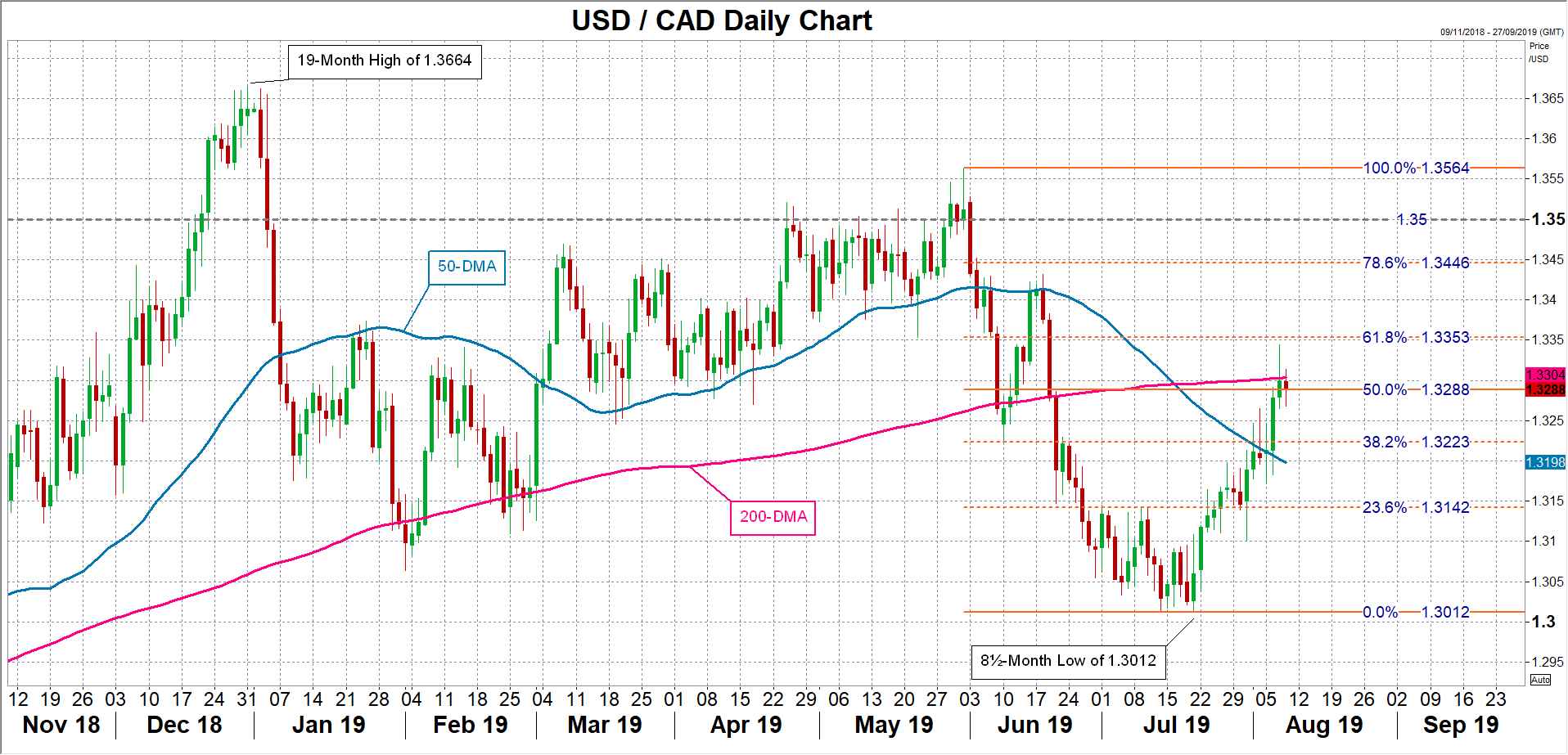

In the meantime, the worsening trade uncertainty and falling oil prices have dragged the loonie to multi-week lows against other majors such as the US dollar, euro and yen.

Loonie on the back foot

Having briefly flown past the 200-day moving average at 1.33, the dollar/loonie’s next target is the 61.8% Fibonacci retracement of the downleg from 1.3564 to 1.3012, at 1.3353. A worse-than-expected set of employment figures could aid a successful break above the 61.8% Fibo and open the way for the 78.6% Fibonacci at 1.3446, followed by the 1.35 handle.

However, if the jobs numbers reinforce the positive outlook for the Canadian economy, a pullback in dollar/loonie is likely, initially to the 38.2% Fibonacci at 1.3223 and then the 23.6% Fibonacci at 1.3142.

Looking beyond Friday’s employment report, the loonie’s direction will not only depend on what the BoC announces at the September policy meeting, but also on whether the US Federal Reserve starts to signal a more aggressive easing cycle, which would of course be positive for the Canadian currency.