{kind=link}

Central banks all over the world are nervous. Overnight, the RBI and RBNZ delivered deeper than expected rate cuts, while Bank of Thailand (BOT) decided it was time to ease again and erase the lone rate hike from December. The floodgates of easy money have been opened and will unlikely slowdown for the rest of the year. Global growth concerns and deflationary pressures are likely to keep the punchbowl overflowing with stimulus that should start supporting commodities.

Rate cuts alone will not be enough, so calls for quantitative easing (QE) from the Fed will grow, despite their reluctance to even commit to an easing cycle. The 2s/10s spread flattened below 10 basis points as recession risks continue to ramp up as the US-China trade war appears to have no end in sight.

The tit-for-tat trade war will see a critical update on Huawei by the end of next week. If the temporary license that loosened restrictions on Huawei is not renewed, this will a major risk off event that will kickstart the next freefall with global equities.

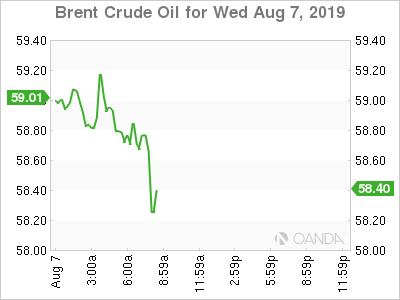

Oil

Oil looks shaky after Brent tentatively fell into bear market territory and as the US EIA cut their estimates for global oil demand in 2019 to only 1 million barrels a day. The oil market appears immune to both the recent string of consecutive drawdown with US stockpiles and supply disruptions in the Persian Gulf as the focus remains on the doom and gloom global economic environment.

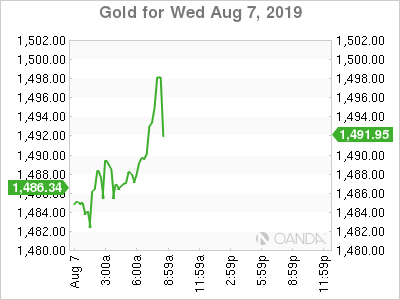

Gold

Gold captured the $1,500 an ounce level and the rally seems set to roll on as no one is expecting any immediate progress on the trade front and the proactive easing efforts from central banks globally. When the Fed capitulates later this month that could be the catalyst to support the drive towards the $1,650 an ounce level.