{kind=link}

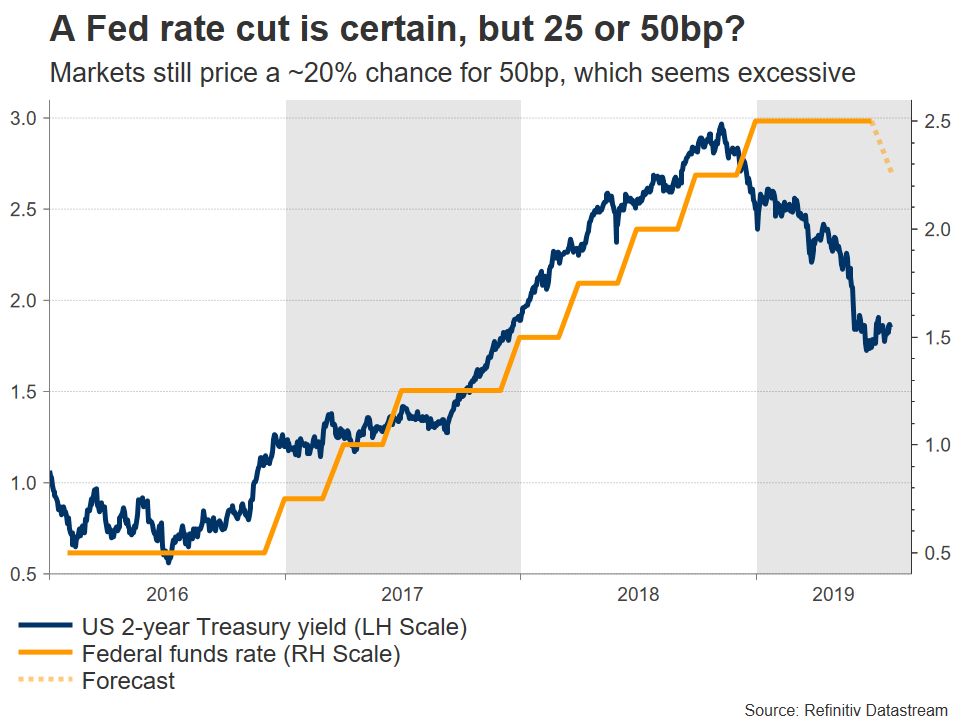

The Federal Reserve is virtually certain to cut rates on Wednesday at 18:00 GMT – the question is how deep it will slash. A 50 basis points (bp) cut seems excessive given recent Fed commentary, so a 25bp move is probably on the cards instead. Since markets still price in a ~20% chance for a 50bp cut, the immediate reaction in the dollar may be higher. Whether any surge is sustained though, will depend on the signals that policymakers send about the pace and depth of future cuts.

It will be a huge week for the US dollar, as besides the Fed rate decision on Wednesday, the latest nonfarm payrolls report will also be released on Friday. On the monetary front, a rate cut is certain according to market pricing, so the real question revolves around the size of this cut – will it be 25 or 50bp?

Bearing in mind some recent comments from Fed officials, a 25bp move seems far more likely. First and foremost, even the most dovish policymaker – James Bullard – said he would like to cut only by 25bps at the upcoming meeting. Bullard voted to cut rates last month and was firmly opposed to raising rates last year, so if he isn’t on board with a 50bp move, who is?

At the time of writing, a 25bp cut is fully priced in, and markets also factor in an almost 20% probability for a 50bp move. This means that more easing is priced in than the Fed is likely to deliver on Wednesday, so the knee-jerk reaction in the dollar may be higher on the decision.

Whether any surge is sustained though, will depend on the signals about the pace and scope of future rate cuts that Chairman Powell sends in the press conference. Is this a one-off ‘insurance’ cut, or the beginning of a prolonged easing cycle? Markets are pricing in a total of four rate cuts – or roughly 100bp of rate reductions – by this time next year.

On balance, Powell is more likely to emphasize that more cuts may be needed soon – vindicating the market’s dovish expectations and therefore sending the dollar back down. He has repeatedly indicated that “an ounce of prevention is better than a pound of cure” and that his Fed will “act as appropriate to sustain the expansion”. These imply that they don’t intend to ‘fall behind the curve’ by delivering less easing than markets expect overall, especially with the risk of a recession looming.

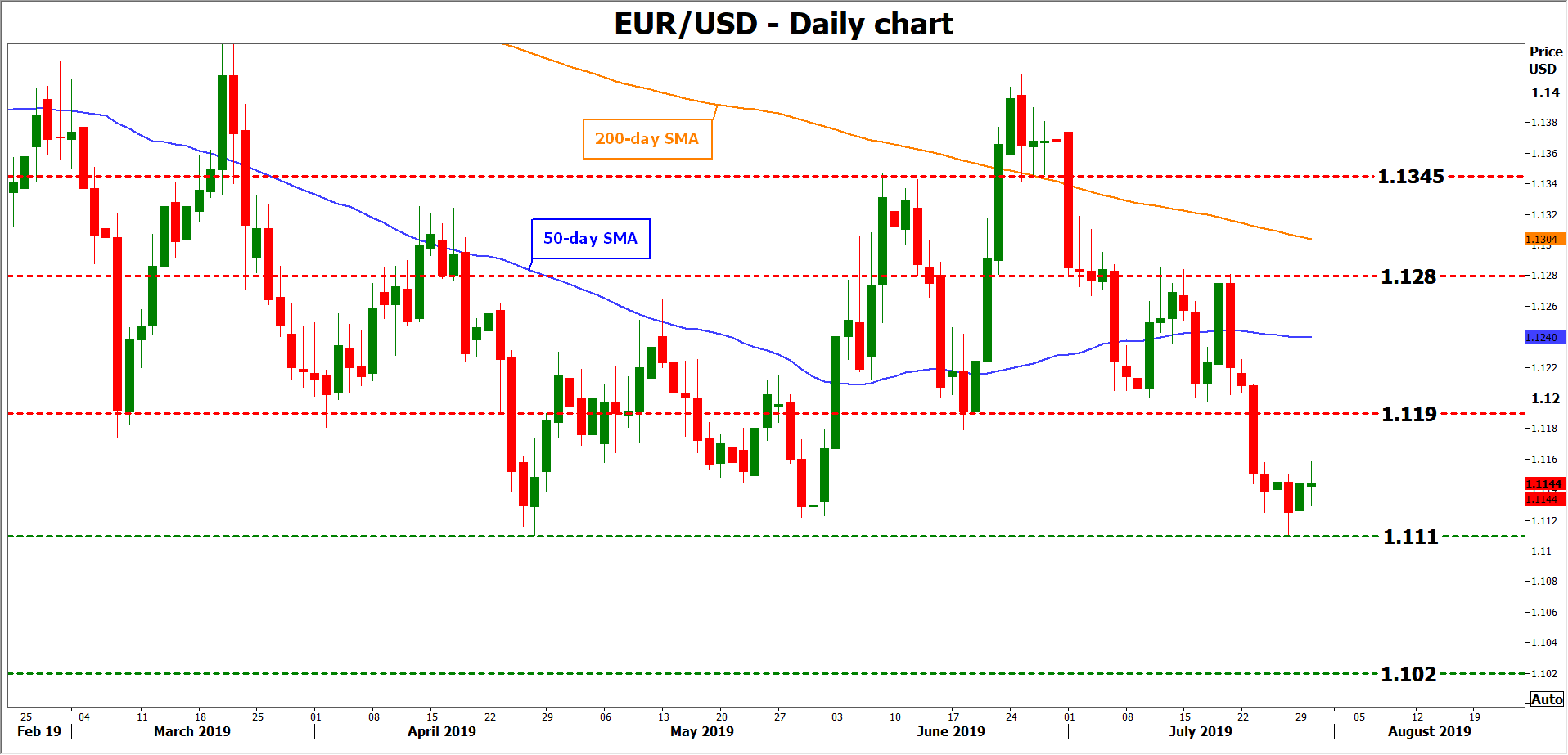

In the big picture, the outlook for the dollar still seems negative. The major central banks are entering an easing cycle, and the Fed has the most scope and ‘firepower’ with which to ease. Hence, the dollar’s downside may be far greater than the euro’s for example as the ECB has much less room to cut, given its already-negative rates. This argues for a higher euro/dollar over time – though a lot will also depend on how aggressive the ECB’s upcoming stimulus package is.

Taking a technical look at euro/dollar, immediate support to declines may be found near 1.1110, with a downside break opening the door for a test of the 1.1020 zone.

On the flipside, a rebound may stall initially near the 1.1190 area, marked by the inside swing low on July 9. A bullish violation would turn the focus to 1.1280.