{kind=link}

Three months before Draghi’s departure, chances for a looser monetary policy are rising higher as heightening global risks are threatening to keep the European Central Bank (ECB) on guard. Nevertheless, more stimulus will likely be a matter of guidance for the future at Thursday’s policy meeting rather than an order for execution despite expectations for a weaker flash composite PMI.

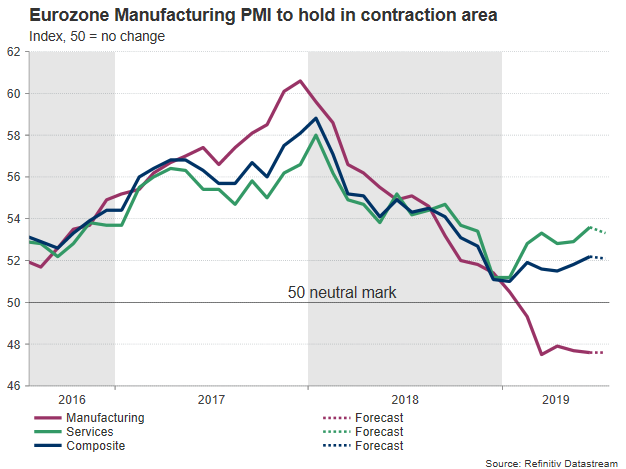

Eurozone flash Composite PMI to inch lower

The ECB has a tough time as eurozone economic indicators have yet to show any sign of improvement, while the Brexit drama, an unstable government in Italy and the US-Sino trade war threaten to prolong the growth weakness for the rest of the year.

The headline Harmonized Consumer Price Index (HCPI) came in slightly better than initial estimates at 1.3% year-on-year in June but what policymakers are seeking is much stronger inflation of close to but below 2.0%. Similar to other major economies, the Eurozone saw its unemployment rate trending downwards to multi-year lows in the past six-years and even though growth in wages rose gradually to decade-highs, inflation pressures remained stubbornly muted, forcing policymakers to keep deposit rates in negative territory and at a record low of -0.4%.

With consumer confidence holding negative and trade risks peaking in the horizon, businesses have little incentive to drive prices higher and engage in new investment. The flash manufacturing PMI for the month of July is likely to indicate on Wednesday (0800 GMT) that factories remained in negative territory as the index is forecast to steady at 47.6, below the 50 threshold that separates contraction from expansion. The services PMI could slow by 0.3 points from the seven-month high of 53.6 reached in June, leading the composite PMI slightly down to 52.1 from 52.2 previously. Yet, with German business surveys reporting more weakness recently, doubts have started to rise about how long the services industry can keep supporting growth in the Eurozone.

September looks the right time to act

Minutes from the previous policy meeting in June and recent dovish speeches by ECB policymakers flagged that Draghi is preparing to deliver an easing package before his successor Christine Lagarde steps up in early November. Since the central bank’s kit is running out of tools to further support the economy, Draghi is expected to cut interest rates by a smaller 0.10 bps compared to the normal 0.25 bps and restart the quantitative easing program that ended in December, probably with some limits – buying for example no more than a third of a country’s debt.

The easing move, however, may come after the summer break at the September meeting rather on Thursday, when the central bank releases new economic projections. A new series of targeted long-term refinancing operations (TILTRO-III) are also scheduled to come in effect in the same month. For the time being policymakers could use a cautious forward guidance to prepare markets over a fresh stimulus injection in coming months.

Still, a rate cut cannot be ruled out on Thursday if the Markit PMI survey disappoints significantly. Given that a weaker exchange rate helps exporters to remain competitive, the ECB could slash rates before the Fed potentially lifts the euro higher by reducing its own borrowing costs next week.

All in all, the next move in the Eurozone’s monetary policy is highly anticipated to be more supportive to the bloc and Christine Lagarde is unlikely to go against this trend when she takes over in November. The former IMF chairwoman, who believes that a raise in import tariffs is not a solution to protect intellectual property rights, has been long praising central banks over their stimulus measures and has backed ECB’s strategy earlier this month, showing that she is on the same page. However, since the Draghi’s stimulus efforts proved fruitless to boost inflation during his term, Lagarde should turn more proactive if she wants to succeed as an ECB governor.

Technical analysis

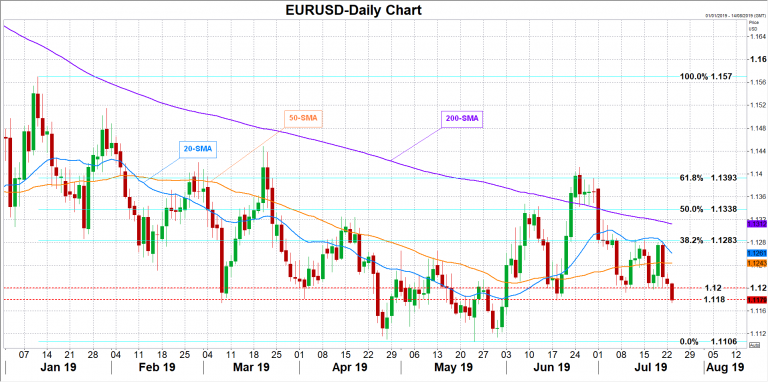

Turning to FX markets, EURUSD has been stuck within the 1.12 zone and below the 20-day simple moving average (SMA) the past two weeks. A miss in PMI readings on Wednesday and a more dovish policy meeting on Thursday could pressure the pair towards the 1.1100 round-level.

In the positive scenario, where PMI figures come in line or above expectations and ECB policymakers fail to convince markets over a rate cut as soon as in September, EURUSD could retest the 1.1260-1.1283 area encapsulated by the 20-day SMA and the 38.2% Fibonacci of the 1.1569-1.1106 downleg. Slightly higher, the bulls would need to overcome the 200-day SMA to reach resistance around the 50% Fibo of 1.1338.

It is also worth noting that any comments on whether the “below but close to 2.0%” inflation target is appropriate could also shake the euro after a bloomberg report revealed last week that the ECB is considering to use a symmetrical inflation target.