{kind=link}

Asian shares are tired and struggling for direction this morning due to a lack of fresh market- moving news, with investors on the sidelines ahead of earnings reports from major American companies.

Although Wall Street closed again at record highs overnight, this positive momentum is unlikely to rollover into Tuesday’s session given how market players are adopting a wait-and-see approach. The mood across financial markets will certainly be influenced by US corporate earnings, especially the performance of major US banks like JP Morgan, Goldman Sachs and Wells Fargo. Should earnings disappoint investor expectations, risk aversion is set to make a rude return and sadly global equity markets will be in the direct firing line.

Dollar creeps higher before US Retail Sales

The Greenback is having a hard time nursing deep wounds inflicted by Fed rate cut bets and this continues to be reflected in the Dollar Index (DXY) which is trading around 97.00 as of writing.

More pain could be in store for the bruised Dollar this afternoon if US retail sales prints below market expectations. Economists are forecasting a tepid 0.1% expansion in sales for the US economy last month. Given how consumption contributes to almost 70% of US GDP, a disappointing figure will not only fuel concerns over the US economy but strengthen the case for a US interest rate cut this month – ultimately punishing the Dollar. With the fundamental ingredients initially sweetening appetite for the Dollar expired, weakness could be a major theme during the second half of 2019.

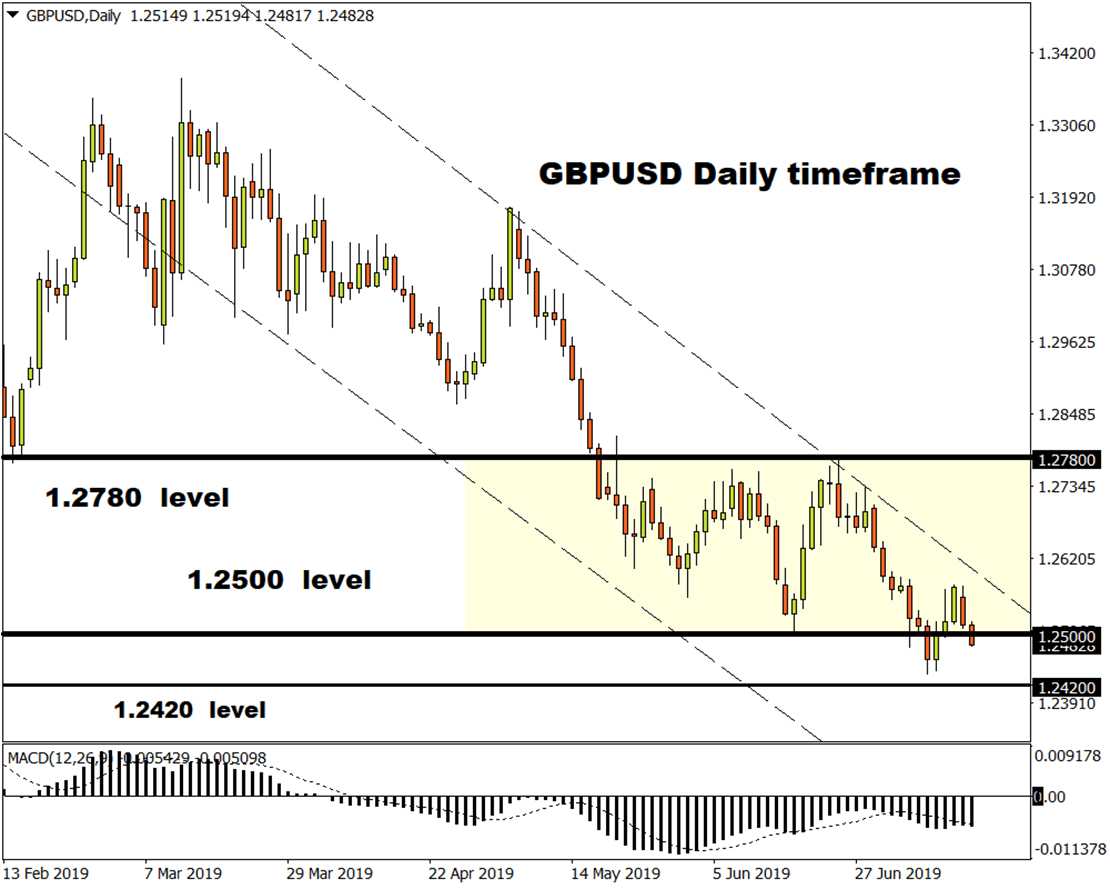

Currency spotlight – GBPUSD

For as long as Brexit uncertainty, political risk in Westminster and BoE rate cut bets remain major themes, the Sterling is poised to remain depressed and unloved in the G10 space.

The British pound slipped towards six-month lows against the Dollar this morning and is likely to extend losses as the bitter cocktail of negative themes swirling around Brexit and UK growth sour appetite for the currency.

Focusing on the technical picture, the GBPUSD is under pressure on the daily charts. A breakdown below 1.2500 should encourage a move lower towards 1.2420.

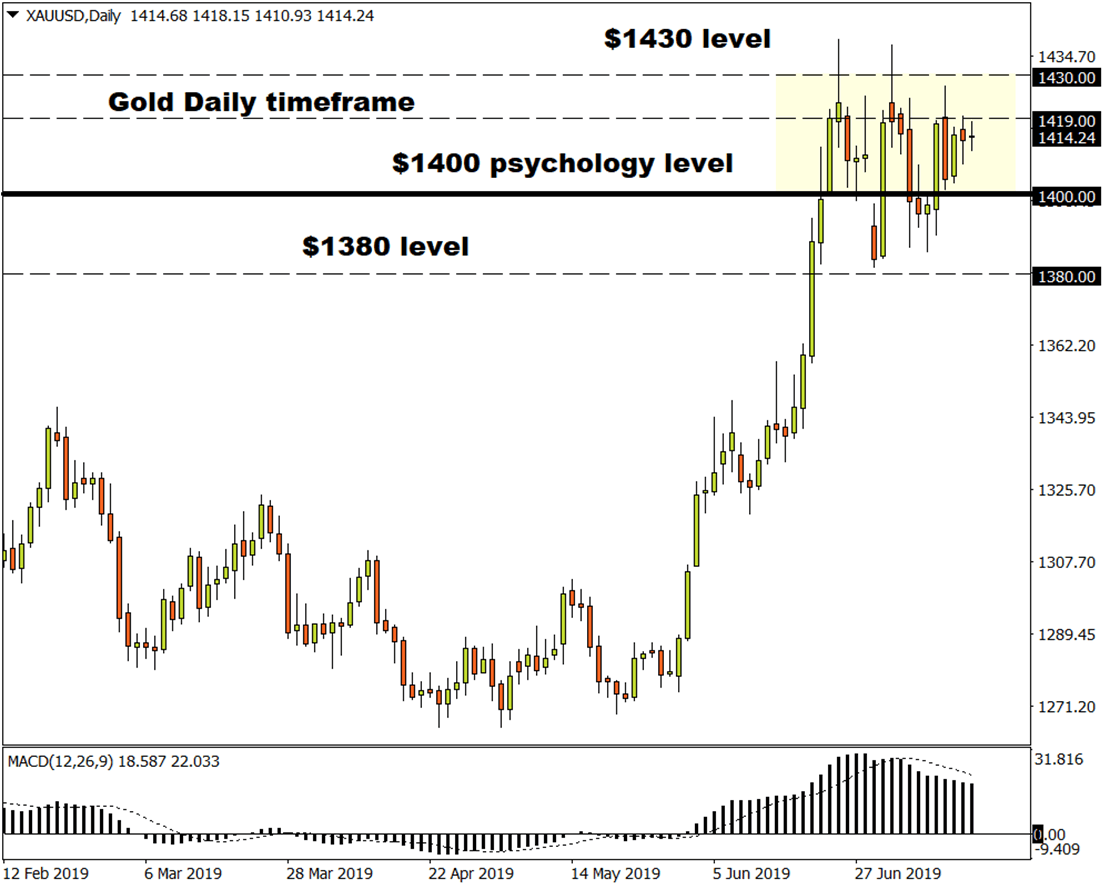

Commodity spotlight – Gold

Gold has the potential to shine with intensity this week if US corporate earnings disappoint and the tired Dollar depreciates.

Appetite for the yellow metal remains supported by expectations of a US rate cut this month, a timid Dollar and ongoing concerns over slowing global growth. For as long as these core themes weigh on global sentiment, bulls remain in a position of power. Focusing on the technical, an intraday breakout above $1419 should signal a move higher towards $1430 in the short to medium term.