{kind=link}

An air of caution is lingering across financial markets as investors huddle on the sidelines ahead of Fed Chair Jerome Powell’s highly anticipated testimony on Capitol Hill later in the day.

Equities across the globe are likely to hold their breath as markets ponder whether Powell would confirm or downplay expectations for a potential US rate cut this month. Given how financial markets remain extremely sensitive to rate cut speculation, there is a lot at stake today with Powell handed the mammoth task of pleasing investors without overpromising. Although last Friday’s strong US jobs report has certainly thrown a monkey wrench into rate cut hopes, the Fed is likely to move ahead with an insurance 25 bps rate cut this month. To prevent markets getting ahead of themselves beyond July, Powell may articulate that future US policy easing will be dependent on US economic fundamentals and ongoing trade developments.

The Dollar was practically drowning in rate cut speculation a few days back before the latest jobs report offered a lifeline. This week, King Dollar is trampling against every single G10 currency excluding the Swiss Franc while treating most emerging market currencies without mercy. Should Powell sound less dovish than expected during his testimony, the Dollar Index could push higher with 97.80 acting as a level of interest.

Sterling becomes the sick man in G10 space as Brexit stings sentiment

This has been a sad week for the British Pound which has weakened against every single G10 currency excluding the Australian Dollar thanks to persistent fears of a no-deal Brexit.

According to the British Retail Consortium (BRC), UK retail sales experienced their “worst June on record” as total sales fell 2.3% year-on-year in June compared with the increase of 2.3% in June 2018. With Brexit uncertainty negatively impacting consumption which is an engine for growth in the United Kingdom, this is certainly bad news for the British Pound.

On a brighter note, official reports this morning have confirmed that the UK economy rebounded in May as GDP rose 0.3% after a decline in the previous month. Manufacturing production which nosedived 4.2% in April rose 1.4% in May slightly easing concerns over the UK economy.

While the Pound may ride higher on the positive report, it does not change the fact that other risks in the form of heighten political risk in Westminster and Brexit uncertainty have left the Pound vulnerable against its G10 counterparts.

Focusing on the technical picture, the GBPUSD is bearish with prices trading around 1.2470 as of writing. Sustained weakness below 1.2500 should encourage a decline back towards 1.2420.

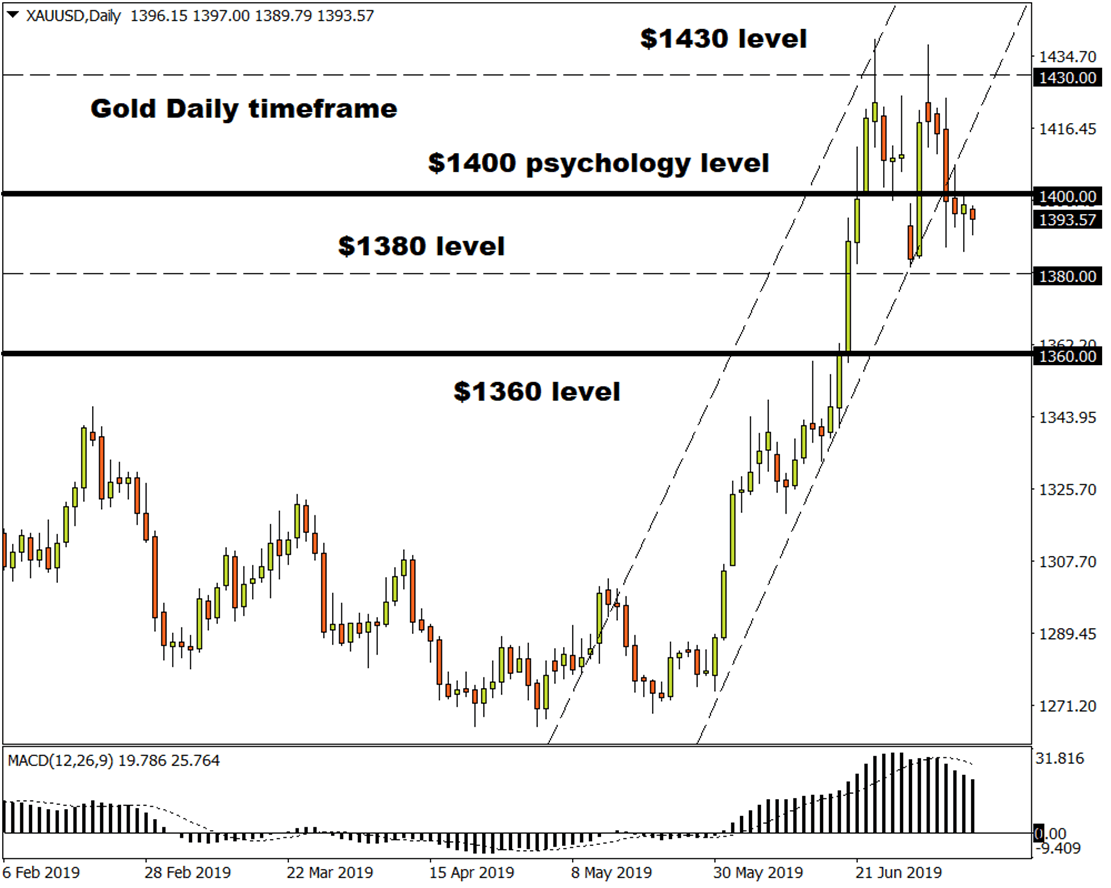

Commodity spotlight – Gold

A broadly stronger Dollar has repeatedly sabotaged Gold’s effort to reclaim the psychological $1400 level this week.

The precious metal has made an effort to push back above the $1400 level but this was cut short by investors re-evaluating whether the Federal Reserve will cut interest rates this month. While Gold may face some obstacles in the near term, bulls are unlikely to lose any sleep in the medium to longer term given how global growth concerns, ongoing trade developments and geopolitical tensions remain core market themes. Where Gold concludes the trading week, will be influenced by Powell’s testimony and the FOMC meeting minutes later this evening.

For bulls to jump back into the game, Gold needs to secure a daily close back above $1400.