{kind=link}

Overnight, equities have advanced as the global selloff in technology shares showed signs of easing, while sterling has found some support as PM May tries to secure the votes needed to prop up her minority government and on stronger than expected U.K CPI data this morning.

Despite the tech selloff and political uncertainties, on either side of the Atlantic, stocks are still trading atop of their respected all-time highs.

Later today, U.S AG Jeffrey Sessions will testify publicly before the Senate Intelligence Committee to explain his role in the firing of James Comey and contacts that he and associates of President Donald Trump had with Russian officials.

Also, the Fed begins its two-day meeting where it’s expected to raise their benchmark interest rate for the second time this year tomorrow (2:00 pm EDT) and provide more information on its balance sheet wind-down.

Nonetheless, with stalling U.S inflation, the market is becoming increasingly doubtful that the Fed will be able to stick to their anticipated pace of tightening of three interest rate rises this year and next.

Note: Bank of Japan (BoJ), Swiss National Bank (SNB) and Bank of England (BoE) are also scheduled to weigh in with policy decisions this week.

1. Stocks mixed results

In Japan, the Nikkei share average trimmed a bulk of this week’s early losses and steadied overnight, as the impact from a slide in U.S technology stocks eased. The Nikkei inched down -0.05%, while the broader Topix rallied + 0.1%.

Down-under, Australia’s benchmark S&P/ASX 200 climbed +1.7%, with energy and financial shares leading the way as investors returned from a holiday.

Elsewhere in Asia, South Korea’s Kospi added +0.7%, while Hong Kong’s Hang Seng increased +0.4% and the Shanghai Composite Index advanced +0.4%.

In Europe, the main indices have rebounded this morning after yesterday’s selloff being led by the FTSE MIB (Italy), which is higher, by +1%. Tech names are leading the charge.

U.S stocks are expected to open in the ‘black’ (+0.2%).

Indices: Stoxx50 +0.5% at 3560, FTSE +0.2% at 7528, DAX 0.5% at 12758, CAC-40 +0.5% at 5263, IBEX-35 +0.6% at 10907, FTSE MIB +0.9% at 21105, SMI +0.6% at 8863, S&P 500 Futures +0.2%.

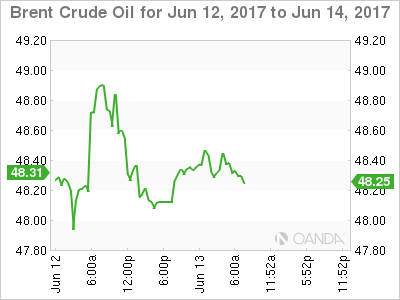

2. Oil rises on Saudi pledge to make real supply cuts, gold steady

Oil prices are better bid ahead of the U.S open after Saudi Arabia said it would make significant export cuts in July, though increasing U.S output, in particular shale producers, continues to weigh on the market.

Brent crude futures is at +$48.64 per barrel, up +35c, while benchmark U.S crude (WTI) is at +$46.38 per barrel, up +30c.

Note: In H1, there were doubts over OPEC’s compliance with its own pledges, however, Saudi officials now say they are making real cuts, including -300k bpd to Asia for July.

Trade data shows OPEC shipments averaged around +26m bpd in H2, 2016, while they are set to average around +25.3m bpd in H1, 2017.

The drive to find new oil has pushed up U.S output by over +10% since mid-2016, to +9.3m bpd. The EIA expects this number to push above the +10m benchmark next year.

For the oil ‘bear’ U.S production undermines any effort led by OPEC to cut almost -1.8m bpd of production until the Q1, 2018 in order to prop up global prices.

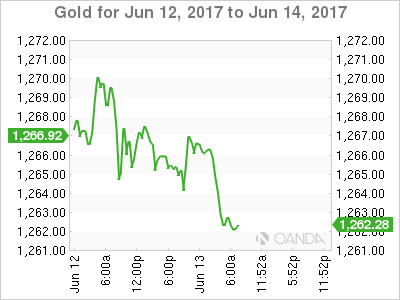

Ahead of the U.S open, Gold is holding steady (-0.1% at +$1,264.01 per ounce) as investors remained cautious ahead of the Fed meeting that is likely to provide hints on the central bank’s interest rate policy for the remainder of the year.

3. Yields back up ahead of Fed announcement

Hectic new U.S debt sales had yields backing up stateside Monday – Treasury sold more than +$100B new debt via four offerings with maturities spanning from 3-months out to 10-years.

Note: A +$12B sale of 30-year bonds along with a four-week bill auction are due this morning.

The Fed is scheduled to announce its rate policy decision tomorrow afternoon, followed by Fed Chairwoman Janet Yellen’s press conference.

Yesterday’s three-year notes attracted the strongest overall demand since December 2015. The +65.6% indirect bidding was way above the average of +51.1% for the past six sales.

The result suggests many investors are looking beyond tomorrow’s expected hike and anticipate a slow path of tightening from the Fed going forward.

The yield on U.S 10’s fell less than -1 bps to +2.21%, after rising for four straight sessions.

Elsewhere, U.K, Germany and French benchmark yields all rose one basis point, while the Aussie benchmark yield is little changed at +2.40%.

4. Dollar’s mixed feelings

The ‘mighty’ dollar is little changed overnight ahead of tomorrow’s Fed decision.

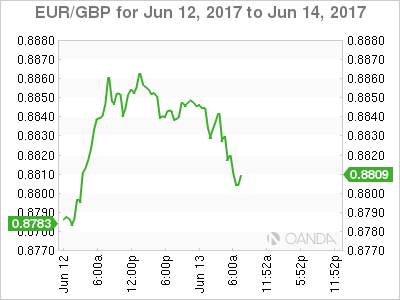

The pound (£1.2704) has found some support in early trade after U.K May CPI data was higher than expected this morning (see below). It remains above the Bank of England’s (BoE) target for a fourth consecutive month to its highest level in four years. Sterling ‘bulls’ believe that last week’s snap election results have reduced the odds for a “hard” Brexit actually occurring is also supporting the pound.

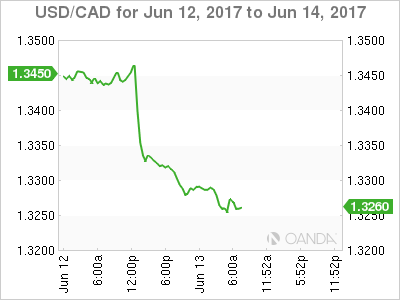

USD/CAD (C$1.3268) continues to trend lower, trading atop of its two-month lows following ‘hawkish’ comments from Bank of Canada’s Deputy Governor Carolyn Wilkins yesterday pointing out that the central bank may consider curtailing its accommodative monetary policy in view of the broadening economic growth.

5. U.K inflation jumps in May, German sentiment falls

Data this morning showed that consumer prices in the U.K rose last month at the fastest annual rate for almost four-years, intensifying a squeeze on households just as the country faces a prolonged spell of political uncertainty.

Annual inflation in May jumped to +2.9%, the fastest rate of price-growth since June 2013. The market consensus was expecting inflation to hold steady at April’s +2.7% rate.

Note: The U.K consumer has been feeling the squeeze from rising prices since last June’s Brexit vote caused a sharp fall in the pound (£1.50 to £1.2707). Making it more difficult is that U.K wage growth is not keeping pace with inflation.

Digging deeper, the pickup in inflation in May was driven by rising prices for packaged vacations, toys and games and computer equipment. Clothing, footwear and household electricity prices also rose.

Note: The BoE is expected to keep the U.K.’s benchmark interest rate steady on Thursday.

Elsewhere, according to the ZEW think tank this morning, German economic sentiment dropped in June – expectations fell to 18.6 from 20.6 in May, which is below the indicator’s long-term average of 23.9. The market was expecting a slight increase in the expectations component to 21.5.