{kind=link}

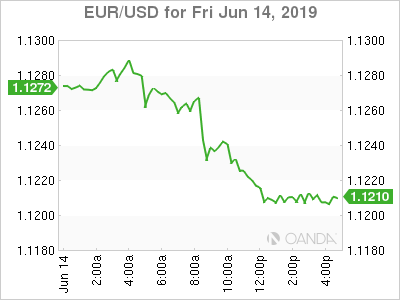

Markets are bracing for updates on tactical trade war positioning and central bank rate decisions. The dollar’s recent rally stemmed on better than expected economic data that could convince Fed officials that the economy is healthy enough and might not require an immediate rate cut. US stocks are struggling resuming the recent rebound until we see further progress on the trade front and a confirmation that the Fed will deliver a rate cut.

On Monday, we will see if China is dumping US Treasuries and public hearings begin in Washington on President Trump’s proposed tariffs on $300 billion more in Chinese goods. The focus for the trading week will fall on the upcoming rate decisions from the Fed, BOJ, and BOE, which should further cement easing money flowing through financial markets. The Fed will meet on Wednesday and is expected to pave the way for July rate cut by downgrading their forecasts and removing their patient stance. The BOJ is not expected to announce anything new, but possibly highlight the growing of the risks to the downside on both their growth and inflation forecasts. The BOE is expected to remain on hold until further clarity is delivered on Brexit. The outlook for the UK economy is worsening and rate hike expectations have been dwindling since February.

- FOMC Meeting: Powell to setup July rate cut

- China’s Treasury Holding Update and Hearings on Trump’s proposed tariffs

- Crude volatility on high alert as Geopolitical Risks Remain and on OPEC meeting uncertainty

Fed

It appears bond markets got their way. After sending the yield on US 10-year Treasury down from just below 2.60% all the way down towards 2.00%, the Fed appears ready to capitulate on cutting rates. With inflation remaining muted and growth vulnerable due to the trade war, the Fed is expected appears set to signal to markets that a rate cut is coming at the July meeting. Fed fund futures see a 21.3% chance that rates will be cut at the June 19th meeting, while the July 31st meeting has an 84.3% expectation for a rate cut. The Fed is widely expected to tweak their stance on being patient, which would signal they are ready to ease.

Historically the dollar weakness is strongest at the beginning of an easing cycle and the Swiss franc has been the strongest beneficiary. If we see the Fed signal a one and done approach to easing, we however could see limited dollar weakness. The Fed owes the market a rate cut to fix the policy mistake at the end of last year and they should keep the door open for further easing to deliver a soft landing for the US economy.

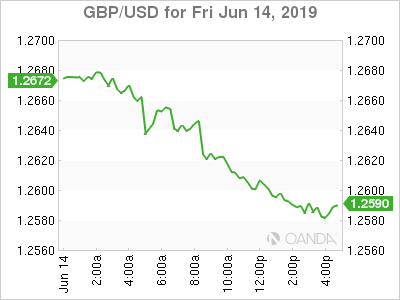

GBP

The Bank of England is expected to keep rates steady as policymakers will unlikely be able to deliver any clear messages on future policy until we have Brexit clarity. While the recent banter has been calling for rate hikes, BOE officials will struggle to deliver a rate hike as economic growth has softened and despite inflation running above target.

Brexit remains the key driver for the British pound and expectations are growing for Boris Johnson to win the Tory leadership. Johnson had a strong showing at the first round of Conservative Party Leadership vote. While Johnson has begun downplaying a hard Brexit, that risk will grow if he wins the top spot and that should cap any sustained rebounds with cable.

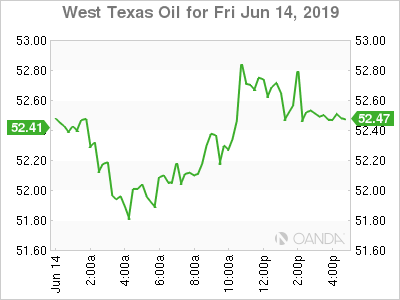

Oil

Crude prices are expected to remain volatile as tensions remain high in the Middle East and as OPEC scrambles to coordinate their next meetings to solidify a continuation of production cuts. Crude remains around bear market territory as global growth concerns from recent escalations in the trade war are flipping the demand argument for higher prices on its head. Rising crude inventories have not done any favors for the supply argument as well.

Next week, should see OPEC and allies finally agree on when they will meet. Russia was hoping to push the meeting back from the scheduled Ministerial meeting from June 26th in to early July. Iran did not want to change any of the dates, with OPEC meeting on the June 25th and the next day being the OPEC and allies meeting. Once the oil producing countries agree upon when to meet, the complicated task in reorganizing production cuts will be difficult to appease both the Russians and Iranians. A failure however in continuing the production cuts could prove catastrophic for crude and could warrant Brent and WTI falling below the $60 and $50 a barrel levels respectively.

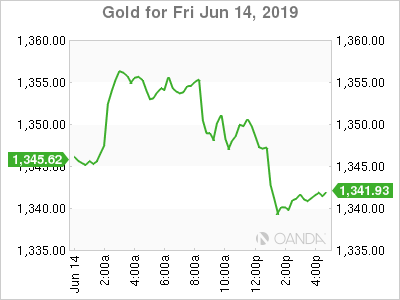

Gold

Gold bulls made their return in June after initially struggling to benefit from strong risk aversion flows in April. Softer economic data globally and expectations the markets will see most of the advanced economies provide easy money have helped the yellow metal gain some traction. The Fed’s FOMC meeting should cement a July cut and that could provide the beginnings of a dollar reversal, which could be bullish for gold.

Deflationary conditions worldwide, rising tensions in the Middle East and trade uncertainty are likely to support gold’s rally. Next week both the BOJ and Fed will update markets on their outlooks for inflation and the overall risks to their respective economies. Dovish messages are widely expected from both central banks.

Bitcoin

Facebook is expected to announce Libra, a new cryptocurrency that has key partnerships with Visa, Mastercard, Paypal and Uber. Mainstream commerce is important for the success with digital currencies and the social media giant’s digital coin could re-energize crypto fans. Libra is expected to launch next year but we could see cryptocurrencies continue to rally as continued acceptance in the financial world will improve retail demand.

Monday, June 17th

- 8:30am ET USD Empire State Manufacturing Index

- 2:00pm ET USD TIC Long-Term Purchase

- 9:30pm ET AUD RBA Minutes of June Policy Meeting

- 9:30pm ET AUD Q1 House Price Index q/q

- 9:30pm ET CNY New Home Prices m/m

Tuesday, June 18th

- 2:00am ET EUR Germany PPI m/m

- 3:00am ET TRY Turkey Industrial Production m/m

- 5:00am ET EUR Germany ZEW Current Situation Survey

- 5:00am ET EUR Eurozone ZEW Survey Expectations

- 5:00am ET EUR Final CPI y/y

- 8:30am ET USD Housing Starts & Building Permits

- 8:30am ET CAD Manufacturing Sales m/m

- 7:50pm ET JPY Trade Balance

Wednesday, June 19th

- 3:30am ET SEK Unemployment Rate

- 4:00am ET ZAR CPI y/y

- 4:30am ET GBP CPI y/y

- 7:00am ET USD MBA Mortgage Applications

- 8:30am ET CAD CPI y/y

- 2:00pm ET USD FOMC Rate Decision

- 6:45pm ET NZD Q1 GDP q/q

Thursday, June 20th

- JPY BOJ Interest Rate Decision and Press Conference

- 4:30am ET GBP Retail Sales m/m

- 7:00am ET GBP BOE Interest Rate Decision

- 8:30am ET USD Q1 Current Account Balance

- 8:30am ET USD Initial Jobless Claims

- 8:30am ET USD Philly Fed Manufacturing Index

- 10:00am ET USD CB Leading Index m/m

- 10:00am ET Eurozone Advance Consumer Confidence

- 7:30pm ET JPY National CPI y/y

- 8:30pm ET JPY Preliminary Manufacturing PMI

Friday, June 21st

- 3:15am ET EUR France PMI data

- 3:30am ET EUR Germany PMI data

- 4:00am ET EUR Eurozone PMI data

- 4:30am ET GBP Public Finances (PSNCR)

- 8:30am ET CAD Retail Sales m/m

- 9:45am ET USD Markit PMI data

- 10:00am ET USD Existing Home Sales