{kind=link}

The mood across financial markets was cautious this morning as rising geopolitical tensions in the Middle East and persistent uncertainty over US-China trade developments capped risk appetite

Asian stocks were subdued on Friday after China’s industrial output dropped to its lowest levels for more than 17 years in May. The risk-off tone and disappointment from Asia have already infected European markets which are trading lower this morning. With a sense of caution also kicking in ahead of next week’s Federal Reserve meeting, Wall Street may struggle to maintain gains this afternoon as investors adopt a guarded approach towards riskier assets.

Although global equity markets have performed relatively well in June thus far, the quarter-to-date (QTD) gains across the board are nothing to celebrate. One must really question the sustainability of the stock market rally, given the storm of headwinds weighing on global sentiment. It must be kept in mind that the fundamental ingredients for a selloff across stock markets are bubbling dangerously in the cauldron. Equity bears remain in the vicinity and may be simply waiting for the perfect opportunity to make their move.

Dollar waits for US retail sales report

The main risk event for the Dollar today will be the highly anticipated US retail sales report for May which will be closely scrutinised by investors for signs of trade tensions negatively impacting domestic consumption.

Sizzling trade tensions and disappointing economic data from the States have fuelled speculation over the Federal Reserve cutting interest rates this year. Since the Federal Reserve will be meeting next week, the retail sales data will play an important role in shaping expectations for the central bank’s forward guidance. Should retail sales disappoint by printing below 0.6% month-on-month forecast, the Dollar will feel the pain, as the 75% probability for a Fed rate cut in July will potentially tick higher.

Looking at the technical picture, the Dollar Index is trading around 97.00 as of writing. Prices have scope to retest 96.50 is retail sales disappoint.

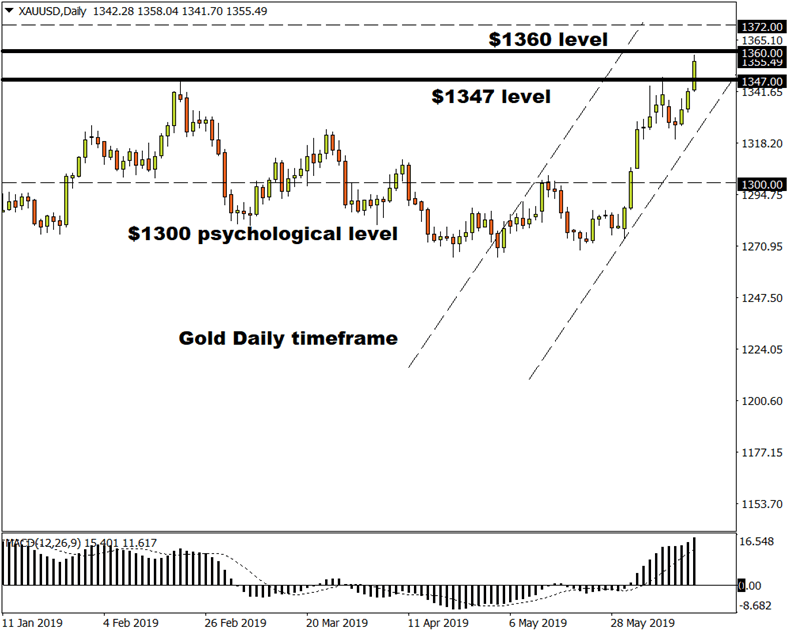

Commodity spotlight – Gold

It has been an unquestionably bullish trading week for Gold which has rallied to a yearly high above $1355.

The forces behind Gold’s aggressive appreciation revolve around geopolitical tensions in the Middle East, ongoing US-China trade tensions and rising expectations over the Fed cutting interest rates. With these key fundamental drivers straining investor confidence and souring appetite for riskier assets, Gold is set to shine as investors sprint to safe-haven assets. From a technical perspective, Gold bulls are in the driver’s seat with a weekly close above $1360 opening the doors towards $1372 and $1390, respectively.