{kind=link}

- Markets hopeful the US and Mexico can reach a deal on migration to avert tariffs

- Dollar inches higher ahead of May nonfarm payrolls report

- Euro firmer after ECB meeting as Draghi fails to provide strong easing signals

Optimism about US-Mexico talks lifts markets

Global stock indices were headed for weekly gains as expectations that the US Federal Reserve and other central banks around the world would soon cut interest rates to counter the damaging impact of rising trade tensions lifted sentiment. Traders were also hopeful that US and Mexican officials will be able to resolve the issue of illegal migration across the two countries’ border.

There were some encouraging signs from yesterday’s talks, with US Vice President Mike Pence saying Mexico had come back to the table with “more” but added that the final decision was still with President Trump. Negotiations are set to continue today but unless major progress is made, the US looks set to increase tariffs on all Mexican imports by 5% on Monday. Trump also again raised the prospect yesterday of introducing tariffs on $300 billion worth of imports from China but said he will wait until after the G20 summit later this month before deciding.

Wall Street’s leading indices managed to close between 0.50-0.75% higher and futures were pointing to small gains when US markets open later today. European equities were also looking to stretch their weekly gains but hopes of stimulus wasn’t enough to boost Chinese stocks as intensifying trade worries pushed the main indices around 1% lower today.

Dollar to take its cues from US jobs report

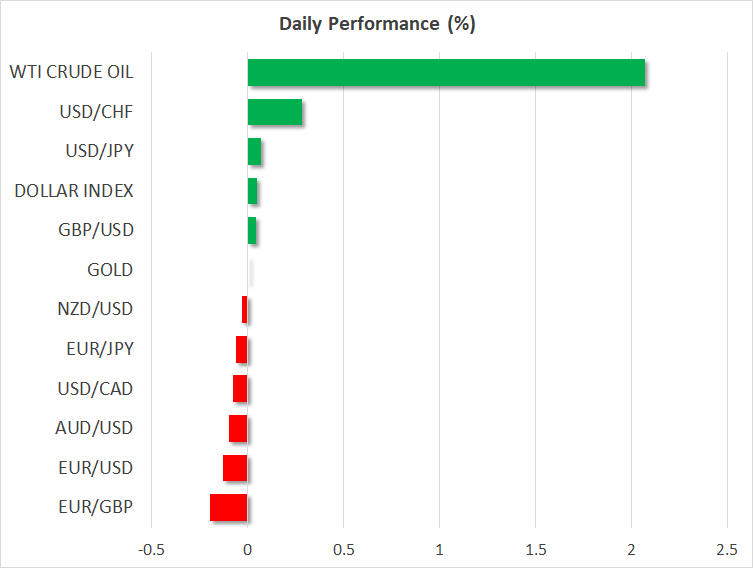

The US dollar was steady on Friday but remained not too far from the multi-month lows plumbed earlier in the week. It was last trading marginally higher at 108.45 versus the yen, in line with the moves in Treasury yields.

New York Fed President John Williams became the latest senior Fed official to open the door to a possible rate cut. In comments in New York, Williams said the Fed may need to be prepared to “adjust” its views on the economy given the rising headwinds from trade frictions.

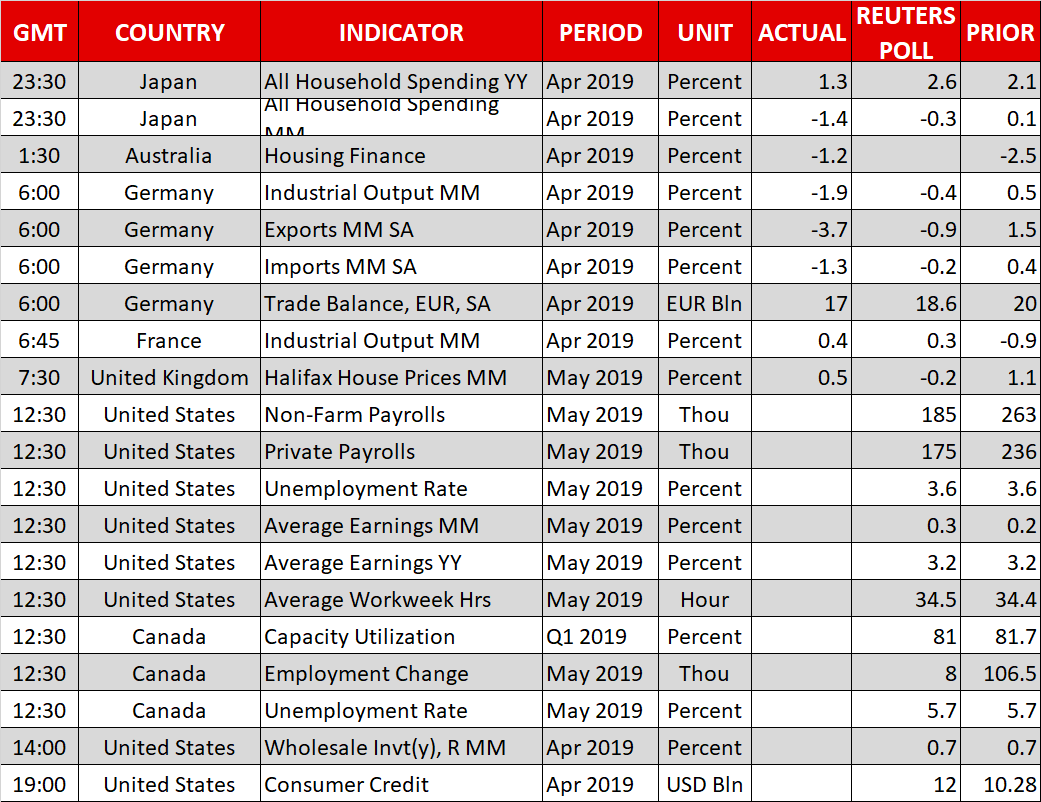

All eyes will now be on the nonfarm payrolls report for May due at 12:30 GMT. Any weakness in the jobs numbers will likely fuel bets of a rate cut in the coming months. But with investors already fully pricing in a 25bps rate cut by September, a poor jobs report may fail to generate a significant sell-off for the dollar and a positive surprise in the figures potentially pose a bigger upside risk for the US currency.

Canada will also publish employment numbers for May today. The loonie, which is on track to finish the week more than 1% firmer against the greenback, could extend its advances beyond today’s 1½-month high of C$1.3341 to the dollar if there’s another month of solid jobs gains.

Euro heads higher on Draghi disappointment

The European Central Bank, as expected, kept policy unchanged on Thursday and gave more details about its latest round of cheap loans for banks. The terms of the loans were not quite as generous as had been speculated, suggesting the ECB is not as gloomy about the outlook as some had been anticipating. The ECB also revised its forward guidance, saying it now expects interest rates to stay at current levels until the middle of 2020 as opposed to the previous guidance of end of 2019.

However, with markets now pricing a rate cut rather than a rate increase, the ECB’s dovish tilt failed to impress traders and the euro ended the day sharply higher, eying the $1.13 level. More crucially, though, although ECB chief Mario Draghi didn’t hesitate to reassure markets that the bank stands ready to increase monetary stimulus if needed, he remained confident about the outlook, saying the risk of a recession was low. This indicates the ECB is far from considering a rate cut just yet and raised concerns the bank could be slow to respond to any new downturn in the Eurozone economy.

Another currency to benefit from a not-so-dovish central bank was the pound. Sterling rose slightly to around the $1.27 level after the Bank of England’s governor, Mark Carney, reiterated that UK interest rates would need to rise at a limited and gradual pace over the coming period. But with Brexit still unresolved, investors remain doubtful of the Bank’s projections.

British prime minister Theresa May is due to officially step down as Conservative party leader today and her replacement could be elected by the end of July, setting the stage for a volatile few weeks for the pound.