{kind=link}

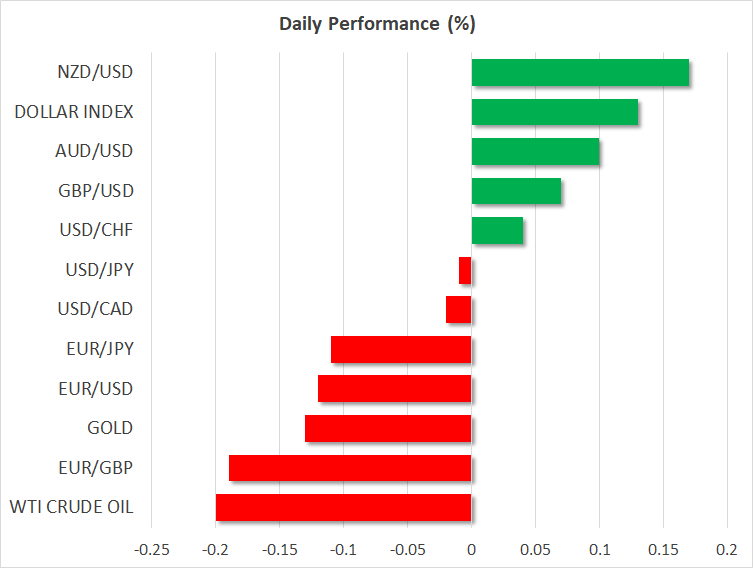

- Euro slips back below $1.12 on reports the EU could fine Italy with $4 billion penalty over high deficit

- Dollar supported by risk-off even as Treasury yields fall back towards 19-month lows

- Stocks buoyed by M&A news, hopes of more Chinese stimulus

Euro on the backfoot again as Italy faces EU fine

The euro’s bounce from yesterday’s results of the election for the European Parliament proved short-lived as the row over Italy’s high budget deficit came back to haunt the single currency. There was widespread relief on Monday when Eurosceptic and populist parties failed to grab control of the European Parliament in EU-wide votes held last week. Although mainstream parties in many EU states suffered badly, the gains made by populist parties weren’t as significant as had been feared.

There were exceptions, however, as anti-EU parties came top in both the UK and Italy. The far-right League party in Italy, which comprises one half of the governing coalition, may see their victory as strengthening their hand in negotiations with the European Commission to allow the country to run excessive budget deficits to help boost growth.

But all the indications are that Italy is headed for another big showdown with the Commission, which yesterday warned that the country could be fined $4 billion for not bringing down its budget deficit and national debt levels. The Commission could begin disciplinary procedure as early as June 5 when it will be reviewing Italy’s finances.

The yield on Italy’s 10-year government bonds jumped higher on the reports and surged again today to a 1½-week high of 2.727%. In contrast, German 10-year bund yields fell to fresh 2½-year lows, with the euro coming under pressure from the widening yield differential.

Dollar reverses upwards, along with yen

Ongoing uncertainty about a US-China trade deal and the possibility of a trade dispute with Japan provided broad-based support for the greenback and the yen, while driving down sovereign bond yields. US 10-year Treasury yields slumped to 19-month lows and the 5-year yield remained inverted with the 2-year one. The dollar index climbed back above 97.80, while the yen was firmer against most of its major peers, including the US currency.

President Trump cast fresh doubt about striking an agreement with China anytime soon after he told reporters on a state visit to Japan that the US was “not ready” to make deal. There was also some confusion about the timeframe of a deal with Japan as Japanese officials played down Trump’s remarks that suggested an announcement could come by August.

Some positives for stocks amid risk aversion

With no let-up still in trade tensions, equity investors focused their minds on the possibility of further policy stimulus by Chinese authorities. Another drop in Chinese industrial profits in April raised hopes that more stimulus could be on the way. The next clue on China’s economy will come on Friday from the latest manufacturing PMIs.

Meanwhile, news that Fiat Chrysler has proposed a merger with French carmaker Renault lifted auto stocks in Europe and Asia. Most Asian indices closed in the green today, though European equities were slightly lower at the open as traders were awaiting direction from UK and US markets, which were closed yesterday for a public holiday.

US housing and consumer confidence data coming up

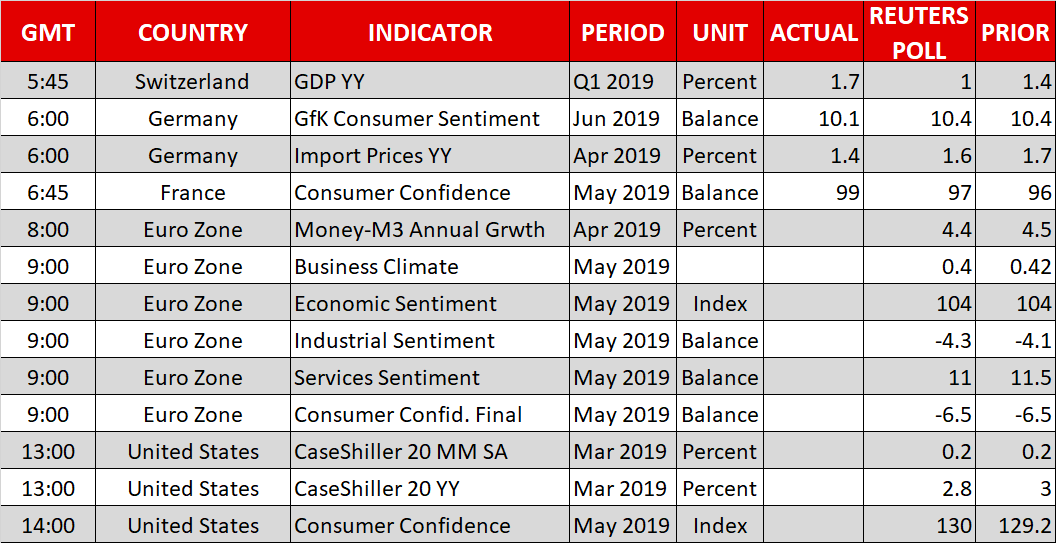

Data on the US house prices and consumer confidence will be watched later today. Any disappointment in those figures that adds to concerns about the US growth outlook could hurt the dollar.

The New Zealand dollar will also be in focus as a speech by RBNZ Governor Adrian Orr at 23:00 GMT could provide hints on further rate cuts by the bank. The kiwi, along with its aussie cousin, were both firmer on Tuesday, helped by higher commodity prices, particularly in iron ore prices.