{kind=link}

With market anxiety heightened about the direction of the US-China trade talks, economic data might struggle to distract traders next week given the shortage of top-tier releases. Still, there will be several major indicators that investors should keep an eye on, including Australian employment and wage figures, Chinese industrial output and retail sales readings, revised GDP estimates from the Eurozone, the UK jobs report and retail sales numbers out of the United States.

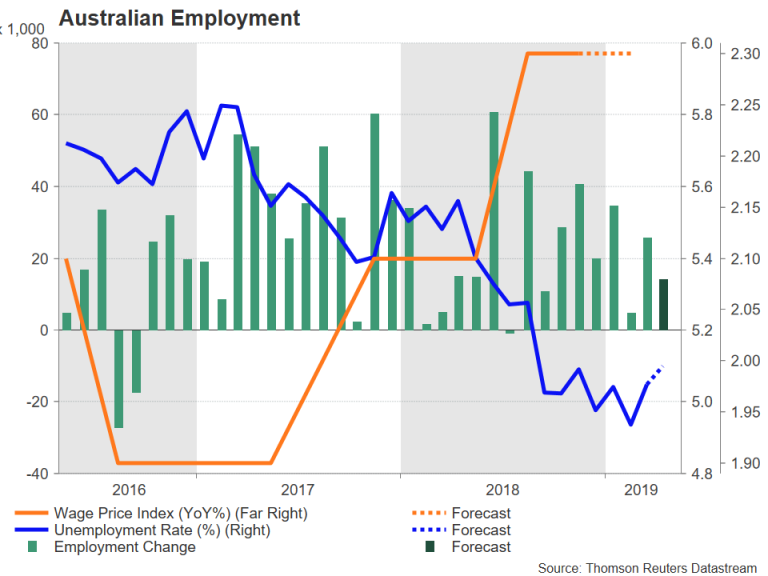

Australian jobs stats could be key for rate clues

The Reserve Bank of Australia held its cash rate unchanged at its policy meeting in the past week but signalled it will be keeping a very close watch on the labour market to assess whether a rate cut will be needed at one of its upcoming meetings. This means the April employment report, due on Thursday, will probably attract more attention than usual, but just as important will be the quarterly wage growth figures out a day earlier. Australia’s wage price index is expected to remain unchanged at 2.3% year-on-year in the first quarter. A weaker number would add pressure on the RBA to lower borrowing costs soon. However, if jobs growth continues to hold up – forecasts are for a gain of 14k positions in April – there would not be the urgency for the RBA to act early.

The Australian dollar, which is currently wallowing near 4-month lows, could extend its losses if next week’s labour market indicators are on the soft side. Politics could also influence the aussie next week as Australians go to the polls on May 18 for federal elections. The opposition Labour party are currently ahead in the polls but the race is tightening. The aussie could appreciate slightly if the polls change in favour of the incumbent coalition government led by Scott Morrison, who is promising bigger tax cuts.

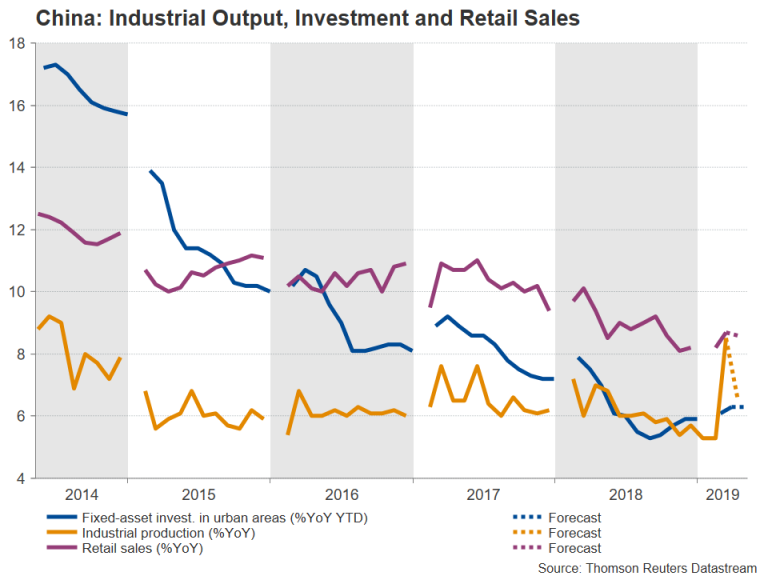

Chinese data to be overshadowed by re-emerging trade tensions

A month ago, industrial output figures for March, which were published alongside the upbeat first quarter GDP print, caused much cheer in the markets as they pointed to a strong rebound in growth. That’s not looking to be the case for the April release coming up on Wednesday as apart from apparent signs that the March bounce back might have been a blip, trade frictions have returned, cutting short the market optimism.

Industrial output is expected to ease from the 8.5% y/y surge seen in March to 6.5% in April. Investment in urban areas is forecast to remain unchanged at 6.3% y/y in the year to April, while growth in retail sales is projected to moderate slightly to 8.6% y/y.

If industrial and retail activity slow by more than expected, it would raise fresh concerns about the growth outlook not just in China but globally as well, especially as a trade deal between the US and China is now in doubt. Investors will be hoping that American and Chinese negotiators will be able to get the talks back on track following this week’s setback. And while a complete breakdown in talks is looking less likely, it remains a real possibility and has the potential to deal a much bigger blow for risk assets than currently seen, in particular, for equities and the China-sensitive Australian dollar.

Eurozone calendar unlikely to provide much direction for euro

As China scrambles to prevent the trade talks from collapsing, European Union officials will be monitoring developments carefully as not only would higher tariffs hurt the Eurozone economy indirectly, but an ever-elusive deal would not bode well for EU-US negotiations, which have yet to formally start. A protracted trade war poses a danger to the Eurozone’s feeble economic recovery.

Growth in the euro area unexpectedly doubled to 0.4% quarter-on-quarter in the first three months of the year according to the preliminary reading. The second estimate of GDP growth, due on Wednesday, is anticipated to confirm this pace. Inflation figures are also expected to remain unrevised. The headline rate of CPI jumped to 1.7% in the flash estimate for April, which was the highest since November 2018. No change is forecast to the final reading out on Friday. Other Eurozone data to look at will be March industrial production on Monday and first quarter employment numbers on Wednesday.

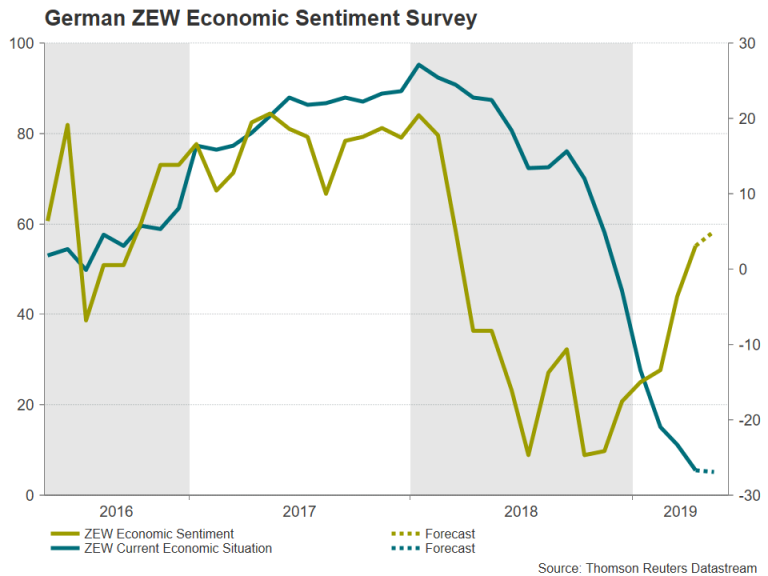

A more forward-looking indicator to watch, though, will be the German ZEW economic sentiment gauge on Tuesday. The index has been steadily recovering from 6-year lows hit in 2018 but remains far below previous peaks, underlining the cautious mood among export-orientated German businesses. Economic sentiment is forecast to improve further in May, rising to 5.0.

While next week’s data are unlikely to be enough to break the euro outside of its recent tight range against the US dollar, they could provide a modest boost if they support the view of a slowly improving economic picture.

UK to publish jobs numbers; Brexit talks continue

The only highlight for the pound next week will be the latest labour market report due on Tuesday. The UK jobs market has been fairly resilient even though economic growth has slowed notably from the ongoing Brexit uncertainty. Employment continues to expand at a healthy rate, lifting average earnings. Wage growth in the UK is currently at a 10-year high, which is good news for consumers who have been the main drivers of the British economy amid weakening overseas demand and falling business investment from Brexit.

If that trend is maintained in March, the pound might just be able to hold on to the $1.30 handle. Growing doubts about whether the cross-party talks aimed at breaking the Brexit deadlock will yield any results pushed cable to more than one-week lows this week, briefly dragging it below 1.30. Those loses could be more substantial should the opposition leader, Jeremy Corbyn, call off talks with Theresa May in the coming days, throwing the Brexit process into fresh turmoil.

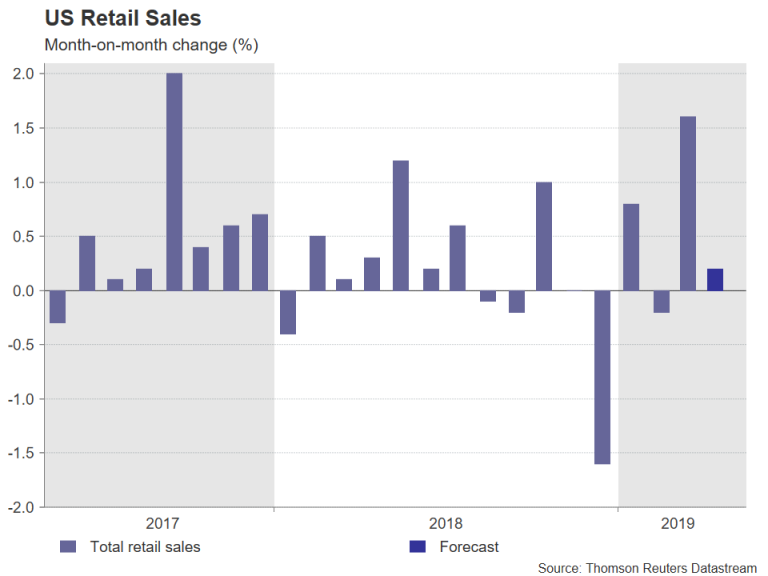

US retail sales to cool after March surge

Over in the US, it will be a relatively busier week for data, but apart from retail sales, there may not be much else to excite the markets. The week will not really kick off until Wednesday when there will be a barrage of releases. Manufacturing activity will be in focus as the Empire State manufacturing index for May and industrial output figures for April are out. But most of the attention will fall on the retail sales report.

After soaring by 1.6% in March, retail sales are forecast to have risen by a more moderate 0.2% month-on-month rate in April. With consumption making up about 68% of US GDP, a negative surprise in the retail sales data would not do the US dollar any favours, especially now that investors have started to once again raise their expectations of a Fed rate cut by year-end as a US-China trade deal hangs in the balance.

On Thursday and Friday, there will be more business surveys for May with the release of the Philly Fed manufacturing index and the University of Michigan’s preliminary print of the consumer sentiment index, respectively. Housing figures will also be under the spotlight; building permits and housing starts for April are both out on Thursday.

Loonie eyes Canadian inflation

North of the border, the main focal point for the Canadian dollar will be the April inflation numbers. The headline CPI rate jumped to 1.9% in March, while underlying measures of inflation also ticked higher. Further strength in consumer prices in April would certainly catch the attention of the Bank of Canada, which has not ruled out resuming its rate hike cycle, contrary to what the markets think. Investors are pricing in about a 50% probability of a rate cut before the year is out despite the bullish oil market and a neutral BoC. This suggests the loonie has room to move significantly in either direction should the incoming data support a rate cut or take it off the table.