{kind=link}

- Markets barely react after US raises tariffs, may be too complacent

- US inflation data coming up, may weigh on the dollar a little

- UK GDP and Canadian jobs figures also due for release today

Trump hikes tariffs, but complacent markets still see it as posturing

As threatened, the US raised its tariffs on $200bn of Chinese goods to 25% overnight, from 10% previously. Beijing immediately responded it will be forced to retaliate, though did not provide any specifics. Yet, markets took the news in the stride, with Chinese stock markets actually recording substantial gains today and safe havens like the Japanese yen trading a touch lower. What gives?

Investors seem to have concluded this is indeed only a negotiating ploy by Trump and remain hopeful that the situation won’t escalate further. Behind this optimism lies the fact that talks will continue in Washington today, as well as some soothing remarks by Trump, who said earlier that a deal is still possible this week, adding he may hold a phone call with the Chinese President soon. Separately, the increased tariffs will only apply to goods shipped from China as of today, meaning that there’s still a small time window to reach a deal and avert them before they truly come into effect.

Markets are right in the big picture: a deal is still the most likely endgame, despite this escalation. Both sides have too much to lose by not reaching an eventual compromise. However, to believe that a deal can be sealed in a couple of weeks and that matters won’t escalate any further before we get there seems like wishful thinking. To be clear, investors seem too complacent, and it wouldn’t be surprising to see risk aversion return soon, depending of course on the scale of China’s retaliation and how today’s talks conclude.

US inflation data could hurt the dollar

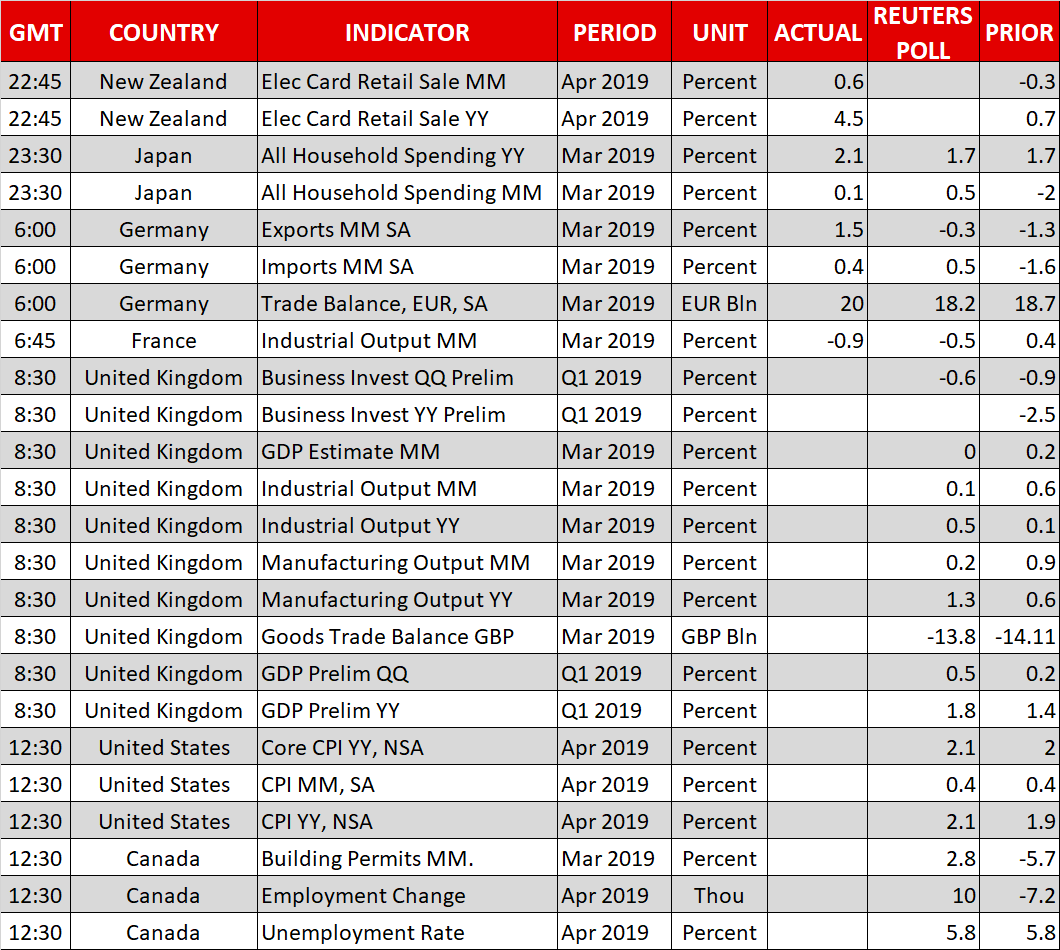

On a more familiar note, the US will release its CPI inflation data for April today. A softening inflation outlook is among the primary reasons that market pricing currently points to a ~75% probability for a Fed rate cut by December, so these figures will be closely watched.

Both the headline and the core CPI rates are expected to have ticked up, though the risks surrounding those forecasts may be tilted to the downside, judging by what the nation’s Markit PMIs for the month signaled. Both the manufacturing and service-sector surveys noted that inflationary pressures softened to multi-month lows in April, which in isolation implies that a downside surprise may be more likely than an upside one in today’s CPI prints. A disappointment could amplify expectations for Fed rate cuts, and consequently weigh on the dollar.

There’s also a slew of Fed speakers on the agenda, including Board Governor Brainard (12:30 GMT) and New York President Williams (14:00 GMT), both of which are permanent votes and highly influential.

UK GDP and Canadian jobs figures on tap too

It’s a relatively busy data on the data front, as besides the US inflation data, we will also get preliminary GDP estimates for Q1 from the UK and Canada’s employment figures for April.

In the UK, growth is expected to have accelerated, but the pound is unlikely to move much on the data. Economics barely impact sterling nowadays, which instead takes its cue entirely from political headlines. On that front, cross-party talks between Conservatives and Labour seem to be going nowhere, which implies that there’s still no clear way to break the Brexit deadlock.