{kind=link}

Trade disputes do not subside, putting pressure on financial markets. Against the background of negative sentiment regarding the trade deal, more and more markets are involved in this “tornado”. The United States announced that China had abandoned some previously agreed concessions, which fundamentally changed the basis for the agreement. Such an approach finally destroys hopes for a deal before the end of this week, despite the formal assurance of the Chinese side that they intend to arrive in Washington at the end of the week.

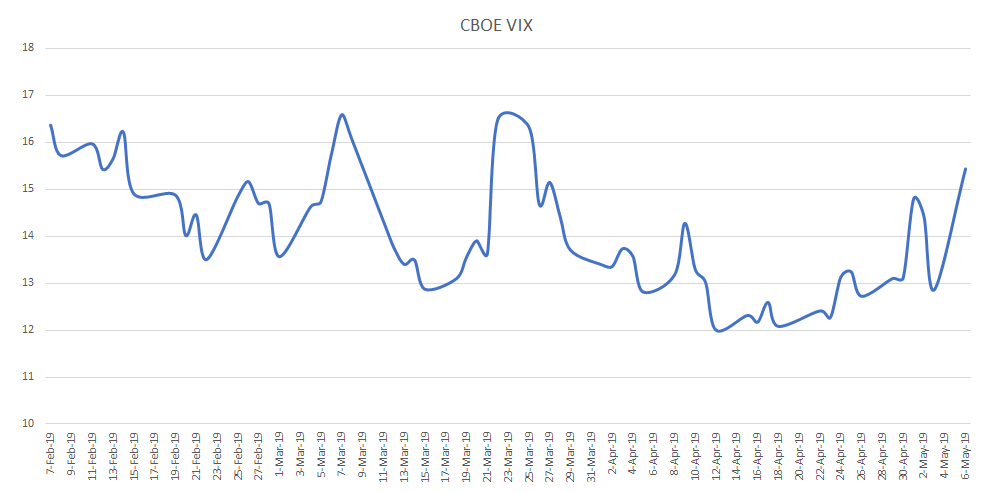

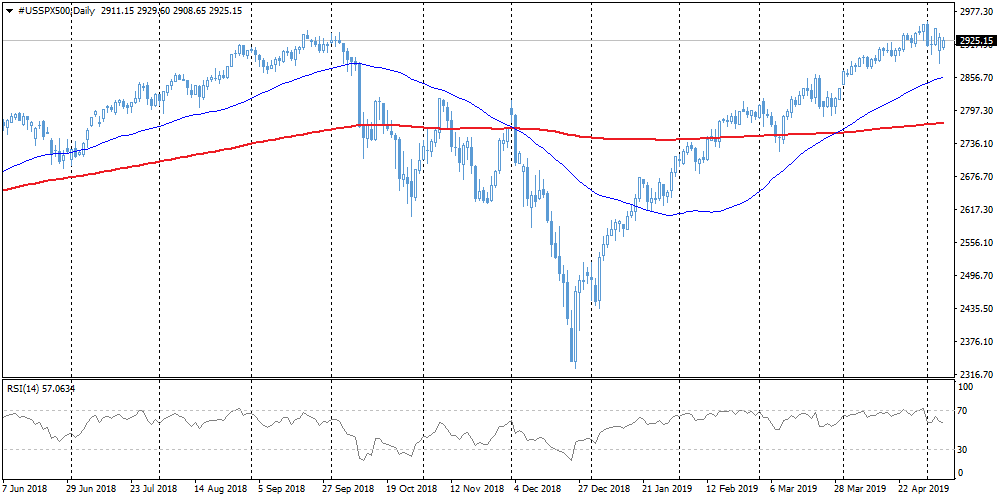

China A50 Shanghai Blue Chips Index turned to a decline, dropping by about 1% against Tuesday’s opening levels, being under pressure due to concerns about deal prospects. Futures on the S&P 500 show increased volatility since the end of last week, opening the day lower by 0.45%. The VIX index, the so-called “fear index,” rose to 15.55, the highest level since the end of March, pushing off from levels near 12 at the end of last month. This is a moderately negative signal for the market combined with RSI decline from the overbought area, which increases the chances of a corrective pullback.

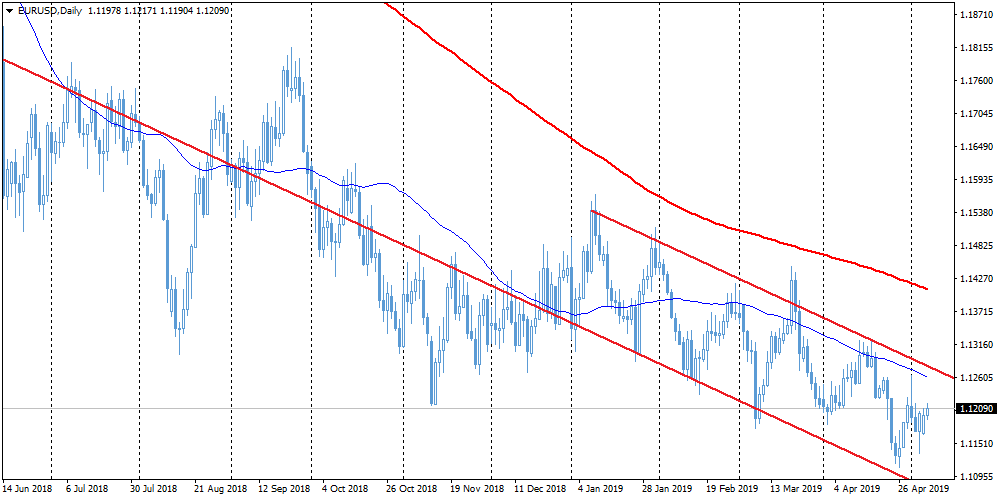

It seems that the series of bad economic data in the eurozone has been left behind. Monday’s PMI indices in the service sector exceeded expectations in addition to strong inflation data at the end of last week. Due to this data, the EURUSD managed to return above 1.1200. Today, the focus of investors with positions in the euro is the publication of the European Commission forecasts. Optimistic forecasts can further support the euro.

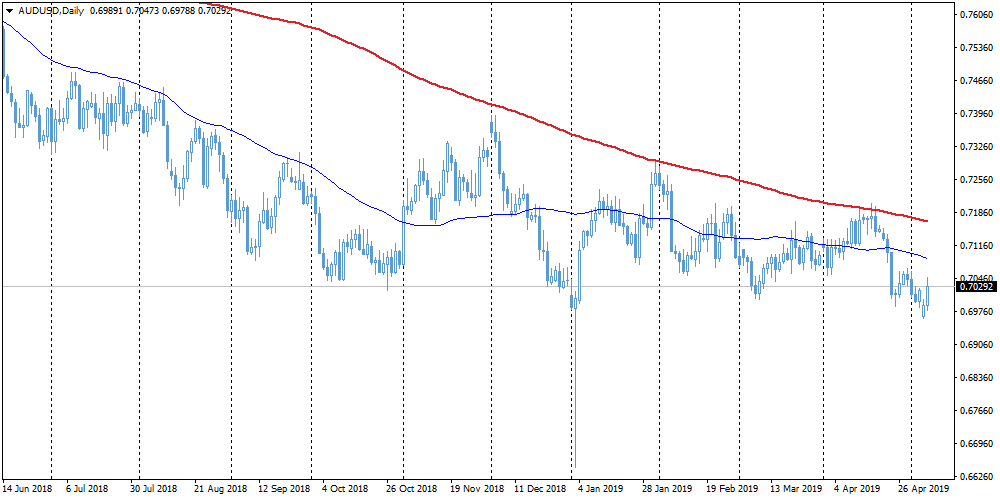

The Reserve Bank of Australia decided not to cut the interest rate, which was expected by most of the surveyed analysts. As a result, AUDUSD jumped 0.6% to 0.7040. The recovery of the pair, however, is restrained by concerns about the US / Chinese trade deal. Next on the agenda is tomorrow’s meeting of the RBNZ. The economies of Australia and New Zealand are tied to exports to China, so the actual and planned steps of the PBOC related to monetary policy since the beginning of the year have somewhat relieved the pressure on the RBA and RBNZ.