{kind=link}

- US stocks stage comeback as markets doubt Trump’s tariff threats

- Aussie soars after RBA remains on hold

- RBNZ decides next – may also disappoint those looking for a cut

Stocks bounce back as traders doubt Trump will escalate

All eyes remain on the US-China trade conflict. Risk sentiment recovered yesterday as the session progressed, with US stock markets recouping most of their early losses to close only modestly lower. It seems investors didn’t really ‘buy’ Trump’s tariff threats, perhaps concluding that this is merely posturing aimed at raising the pressure on China. Yet, the top US trade negotiator – Robert Lighthizer – confirmed after Wall Street’s closing bell that the existing tariffs will indeed be raised on Friday.

That sent futures tracking the likes of the S&P 500 back down, but only briefly, with sentiment bouncing back again after headlines reaffirming that China’s Vice Premier Liu He will visit Washington on Thursday, as planned. The fact that his trip was not cancelled probably rekindled some hopes for a de-escalation of the situation.

As for what happens next, it appears increasingly likely that the existing tariffs may indeed be raised this week, though the bar for introducing new levies on the remaining imports from China may be quite high. Trump wants to walk that fine line between pressuring Beijing, but not so much that China walks away from the negotiating table entirely. The bottom line is that recent price action suggests another escalation will probably be avoided, which seems like an overoptimistic conclusion for now.

Aussie jumps as RBA keeps its easing powder dry

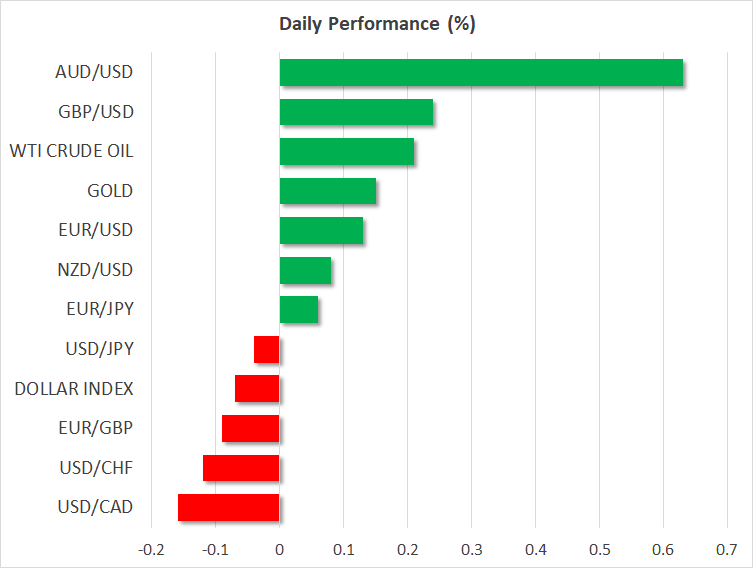

The Australian dollar is outperforming on Tuesday, after the RBA kept its policy unchanged, disappointing those looking for an immediate rate cut. Even though the central bank kept a future rate cut very much on the table, highlighting it will pay close attention to developments in the labor market, the aussie still soared given that investors were pricing in roughly even odds for a rate cut today.

A full quarter-point cut is still priced in by August, which shows that traders believe it’s a matter of when, not if, the RBA will ease. Combined with the prospect for further escalation in the US-China trade conflict soon, the outlook for the aussie doesn’t appear especially bright in the near term – though a lot will depend on incoming data.

RBNZ could follow in the RBA’s footsteps

Now, the central bank torch is passed to the Reserve Bank of New Zealand (RBNZ), which concludes its own policy meeting early on Wednesday. Even though the forecast from economists is for a rate cut, investors are not convinced, with market pricing assigning only a ~45% chance for one. Indeed, it’s a close call but on the margin, it seems more likely that the RBNZ could also keep its easing powder dry and perhaps postpone any action for the summer months, effectively buying itself some more time to examine incoming data.

If that is the case, the immediate reaction in the kiwi may be higher. That being said, the Bank is also likely to accompany any on-hold decision with clear signals that rates will probably be cut soon, so any positive reaction in the kiwi could prove short-lived, and may even reverse before long.