{kind=link}

- ECB’s Draghi hints at more stimulus, but euro tumbles only modestly and recovers quickly

- Dollar pulls back after disappointing US CPI data, looks to Fed speakers today

- EU grants Brexit extension – Varadkar’s remarks indicate way forward

Euro tumbles as Draghi hints at more stimulus, but only modestly

As expected, the European Central Bank (ECB) kept both its policy and forward guidance unchanged yesterday. President Draghi maintained a cautious tone, highlighting that incoming data remain weak, especially in the manufacturing sector, and that the risks are still tilted to the downside. Most importantly, Draghi stressed – repeatedly – that the ECB stands ready to ‘use all instruments’ to return inflation to its target.

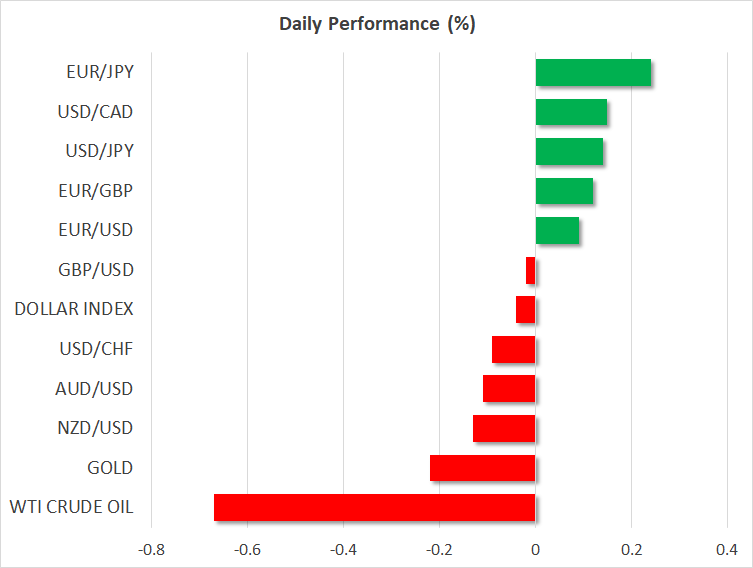

This was a clear signal that if the economy deteriorates further, all options are on the table, ranging from abandoning plans for rate hikes to restarting QE. The euro fell, but not substantially, and certainly by less than one would have expected given hints that more easing may be on the way. Perhaps this illustrates that after years of loose policy, the effectiveness of verbal intervention – even by someone as credible as Draghi – has been exhausted, and that markets may need to see concrete action before pushing the euro lower.

Dollar retreats as underlying US inflation disappoints, equities climb

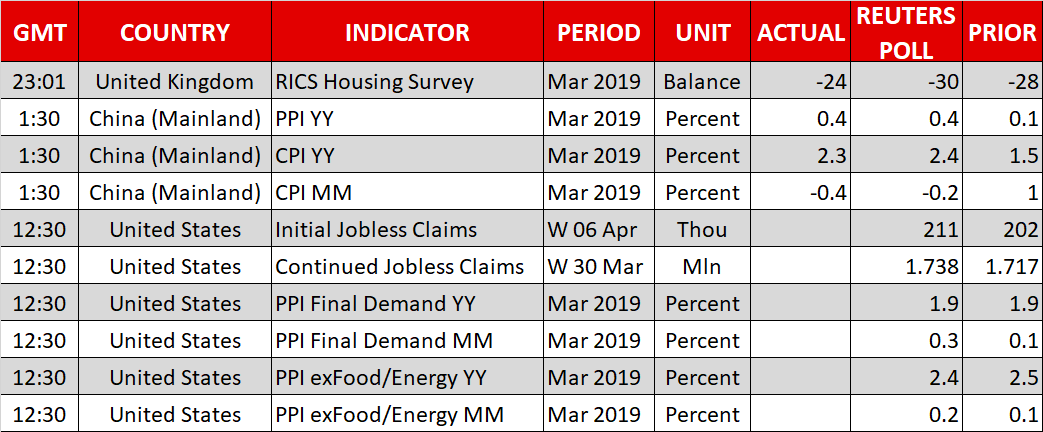

Euro/dollar quickly recovered all its ECB-related losses yesterday to trade even higher, with the move reflecting broad-based dollar weakness, as investors digested the disappointing US CPI data for March. Even though headline inflation beat expectations, the yearly core CPI rate ticked down to 2.0%, missing the forecast for holding steady at 2.1%. The underwhelming figures probably reinforced expectations that the next move by the Fed will be a rate cut; the implied probability for one by December now stands at roughly ~65%. The minutes from the March FOMC meeting didn’t reveal anything new.

Expectations for lower borrowing costs boosted US stock markets though, with the benchmark S&P 500 adding 0.35%. To be fair, some optimistic remarks by Treasury Secretary Mnuchin that the US and China have ‘pretty much agreed on an enforcement mechanism’ likely helped as well, as this was one of the sticking points. Alas, the market reaction on this headline was relatively limited, which implies that most of the ‘good news’ are likely priced in already.

Today, both the dollar and stocks may take their cue from a plethora of Fed speakers, including Vice Chairman Clarida (13:30 GMT) and New York President Williams (13:45 GMT).

EU grants Brexit extension, but the real news come from Ireland’s Varadkar

The EU leaders granted the UK an extension of the Brexit data until October 31 yesterday, with the option of leaving earlier if the British Parliament ratifies a deal in the interim. The delay was conditional upon the UK participating in the upcoming EU Parliament elections, and not reopening negotiations on the withdrawal agreement. The pound liked the news, outperforming most of its peers as the threat of a no-deal exit was taken off the table.

The most important news though, came from the Irish Prime Minister, Leo Varadkar. He hinted that if the UK remains in the EU customs union, he would be open to giving the nation ‘a say’ on future trade deals. If his view is echoed by EU officials, that could boost the chances of the UK staying in the customs union, something that would solve the Irish border issue and hence pave the way for May’s deal – or something similar – to pass through the Commons.