{kind=link}

The near 30% rally in WTI Oil during the first quarter of 2019 is difficult to justify when taking into account the progressive concerns that are mounting regarding a global economic downturn. The rally has been supported by improved market confidence that efforts from OPEC+ have tightened the supply in the market, but whether this encouraging sentiment can continue would likely depend on whether Russia continues to support production cuts.

As such, a result to an unprecedented 30% rally over the last quarter, the commodity is going to enter the new quarter as a prime contender to suffer from a market correction. The probability is high that fears over a deceleration in world economic momentum will only get louder as the year progresses, meaning Oil investors will need to re-assess into expectations what impact a global slowdown will have on future demand. A plethora of evidence through data releases from different economies across the globe has already pointed out that a downturn in growth is impending – if the slowdown hasn’t already arrived.

Market perception is that OPEC cuts areworking but demand outlook at risk

One of the major risks for the price of Oil in the second quarter is the increased probability that world economic forecasts for 2019 will be revised lower. While a great volume of noise in the Oil atmosphere is created around headlines involving production, OPEC or even more recently OPEC+, it often gets underlooked just how important Oil demand is for its valuation. Reduced demand is a negative for Oil price and the prospect of further lower demand on global economic health fears will risk re-igniting oversupply concerns that have dominated headlines since the spectacular price crash first occurred in 2014, despite repeated measures and attempts by OPEC and co to rebalance the market.

Iran waivers a wildcard, Saudi Arabia to remain committed to output cuts

If you were to take the contrarian view, there are a few reasons to remain optimistic that Oil can resume its price rebound in Q2. This would however, include some unpredictable risk elements around politics for a commodity that has historically behaved with an extreme level of sensitivity to politics.

Waivers on Iranian sanctions are set to expire over the coming months and if President Trump adopts a hardline approach that results in the taps for Iranian Oil supply being turned off, the subsequent change in the production outlook would prove tempting for potential buyers. Venezuela is another market that has come under the threat of sanctions following recent domestic unrest, while suspicions remain that Saudi Arabia will maintain its underlying commitment towards tightening the available supply of Oil to achieve stronger valuations to help the Kingdom achieve its fiscal targets.

Do not underestimate risk Trump speaking against Oil rally will have on future outlook

Another factor that needs to be taken into account when factoring in potential risks that can swing the hammer of the Oil price in either direction is President Trump.

The President of the United States has made it perfectly clear on numerous occasions that his desire is for Oil prices to return to lower levels for a prolonged period. He has already commented via social media feeds that the Oil price is too high and while he might not be President of a nation that is either a traditional member of OPEC nor OPEC+, he carries the ability to influence world financial markets. When it comes to President Trump’s influence on financial markets it is never an occasion that investors can prepare for when it will happen, but Trump has proven in office that he has a tendency of getting his way in the end, and I would personally not want to be on the wrong side of the trade when the President of the United States is demanding for lower Oil valuations.

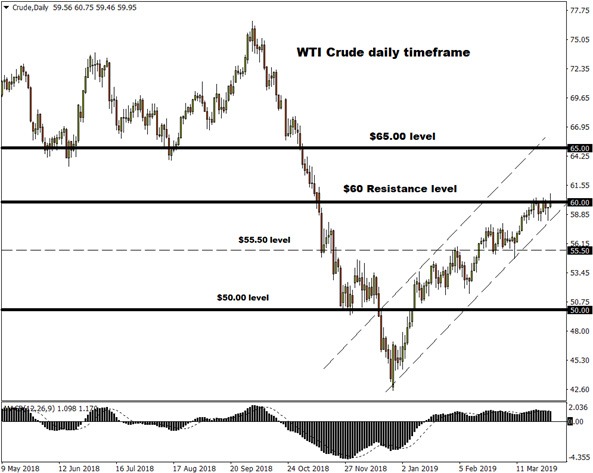

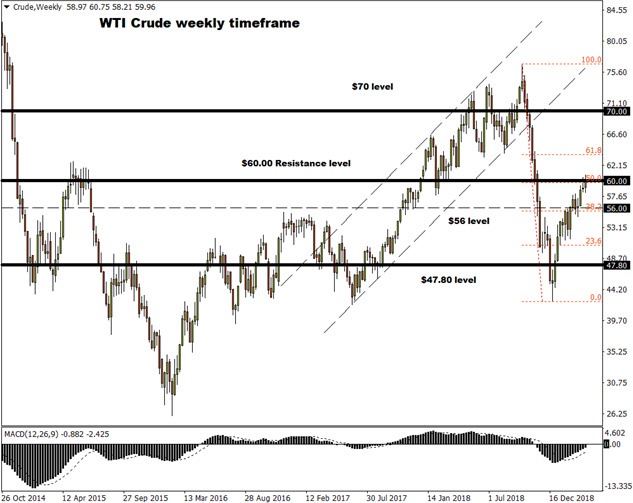

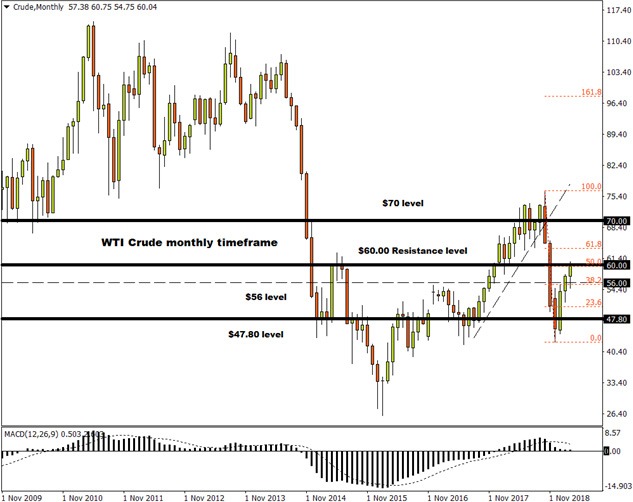

WTI knocking on the door at $60, but is anyone home?

Focusing on the technical picture, WTI Crude has reached tough resistance on the monthly charts with $60 acting as a barrier for bulls preventing prices by being pushed higher. The $60 level ironically also reflects the 50% Fibonacci retracement level of the October -December 2018 downtrend, which helps explain why we are noticing a trend of selling pressure jumping back in the market close to $60.

Until Oil is able to secure a decisive monthly close above $60, it looks like a ceiling is in place for Oil bulls and selling rallies below this level is going to remain as a tempting strategy for bearish investors. A weekly close below $56 will act as a signal for further downside with $52, $50 and $47.80 acting as key points of interest.

If prices are able to conquer $60, Oil has scope to challenge $65