{kind=link}

- Brexit – All scenarios remain on the table

- Riksbank – Bye Bye Hikes

- Stocks – Mixed as markets await Trade and Brexit clarity

- Oil – US trims crude output forecast for first time in 6 months

- Gold – Rising on tame inflation and trade deal uncertainty

Brexit

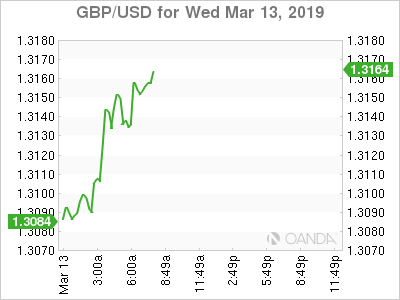

Following yesterday’s crushing rejection of Prime Minister May’s divorce deal, Parliament will vote on whether they will have a hard exit or allow themselves to vote on an extension and hope to negotiate a better deal. Current expectations are high for the UK members of Parliament to vote in support of blocking the UK leaving the EU without a deal on March 29th.

The EU believes May’s second defeat raises the risk of a no-deal Brexit. If Parliament’s votes go as planned, it will be up to the EU and all 27 members to approve an extension. This is the biggest uncertainty and we will find out exactly their position by the EU Summit on March 21st and 22nd.

PM May’s divorce bills have been defeated by margins of 230 and now 149. She has been resilient throughout Brexit and many are amazed she has last this long. There is no high certainty on how we will see the UK eventually agree on a divorce deal, but it may have to involve her offering to step down. The risk of second referendum is growing and Brexiteers do not want risk losing Brexit. After an extension is voted on, one scenario could see the UK agreeing on a deal in the coming months that is accompanied with May’s resignation. Everyone wants Brexit clarity, but a lengthy delay could see a second referendum that would take almost a couple of months to set up.

The British pound was the best performer this morning and could remain supported once Parliament rejects a no-deal Brexit and vote for an extension on Thursday.

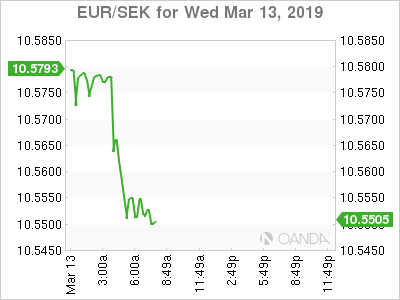

Riksbank

The Riksbank was one of the last remaining central banks that were still expected to deliver a rate hike this year. That ship may have sailed as inflation fell below the bank’s 2% inflation target. This morning, the Swedish National Financial Management Authority (ESV) cut their growth forecasts for both 2019 and 2020. With the ECB unleashing new stimulus, slower growth concerns, and inflation that can’t stay above target, the Riksbank will need to push back rate hike expectations to the middle of next year.

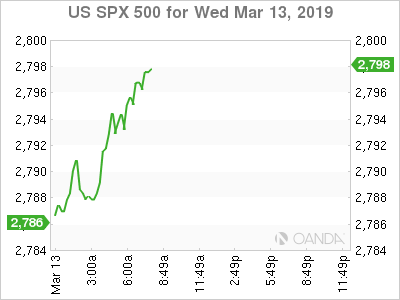

Stocks

European markets provided little excitement today following yesterday’s Brexit defeat and better than expected euro zone industrial production data. Asian equities were weighed down by disappointing Japanese core machinery order data and falling Australian consumer confidence. The global economy’s global growth concerns will unlikely be alleviated until we see further progress on both Brexit and the US-China trade war. Brexit remains a negative for business in Europe and any extended delays in yielding a conclusive outcome will continue to prevent growth returning somewhat to normal. The US-China trade war is still expected to be wrapped up soon, but if both sides can’t agree on enforcement, we could see this become a very negative catalyst for risk.

Tonight, Chinese data is expected to confirm global growth worries as industrial production and retail sales are expected to decline sharply. At the end of the week, the Bank of Japan is expected to keep policy unchanged, maintain both their JGB purchases and their forward guidance while possibly downgrading their views on the economy. Rate cut expectations are growing for the BOJ to act again this summer.

Even with some rising expectations that we could see an earnings recession, easy monetary policy is still the theme of 2019 and with most of the major central banks queuing up rates are going nowhere and that the next policy moves are likely to be cuts, equities may have support on any major selloff.

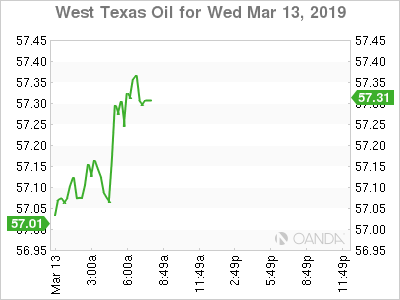

Oil

Crude prices are up for a third consecutive day and approaching the top of the range that has been in place since mid-February. Today’s rally was supported by the EIA cutting of both the 2019 and 2020 US production forecasts, which are still expected to deliver record levels. The reduction of just over 100,00 barrels is a sign that US production might see some headwinds as oil companies struggle being profitable with oil in the mid-$50s.

Continued rhetoric from OPEC members that production cuts will be extended to year end is still the main catalyst for keeping West Texas Intermediate crude above the $57.00 level. Ahead of today’s EIA crude inventory report, which is expected to deliver a build of 2.6 million barrels, the weekly API reading saw inventories decline by 2.6 million barrels. If today’s EIA reading shows inventories decline, that would be the second decline in three weeks. The longer we see crude unable to break above the February highs, the more impatient we could see bullish bets become.

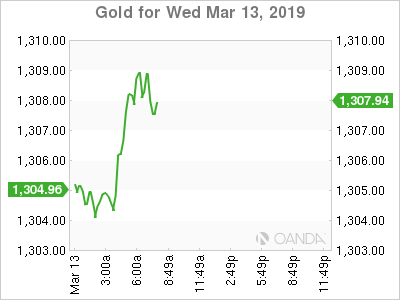

Gold

Benign inflation in the US was the spark plug needed to get gold back above the $1,300 an ounce level. The precious metal struggled for gains over the past couple weeks as optimism was high that we were going to see a trade deal delivered with a mid-March meeting between Presidents Trump and Xi. Financial markets are still pricing in a trade deal, but it appears the timeline is being pushed back towards April.