{kind=link}

- Markets will focus on trade today, as another round of US-China talks wraps up

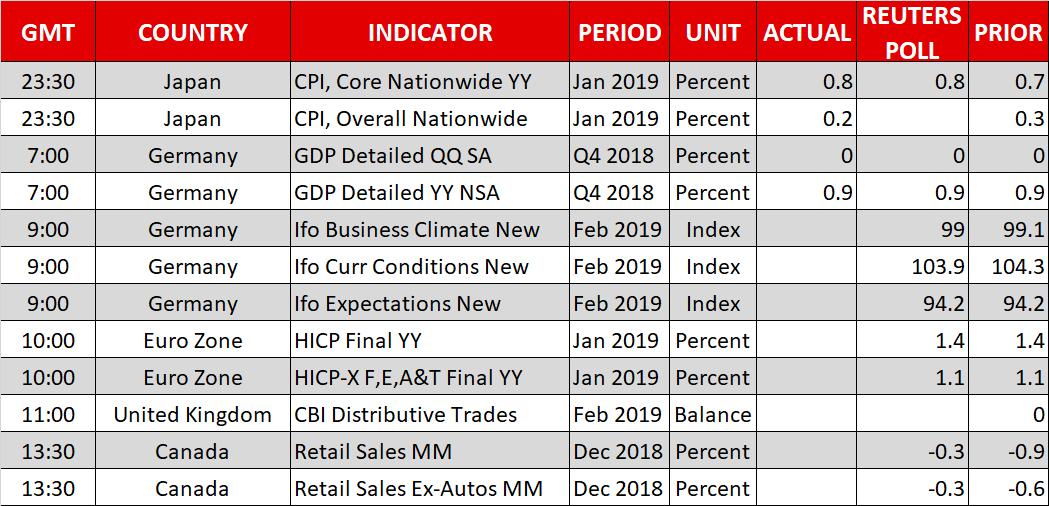

- Euro looks to Germany’s Ifo survey and remarks by ECB’s Draghi

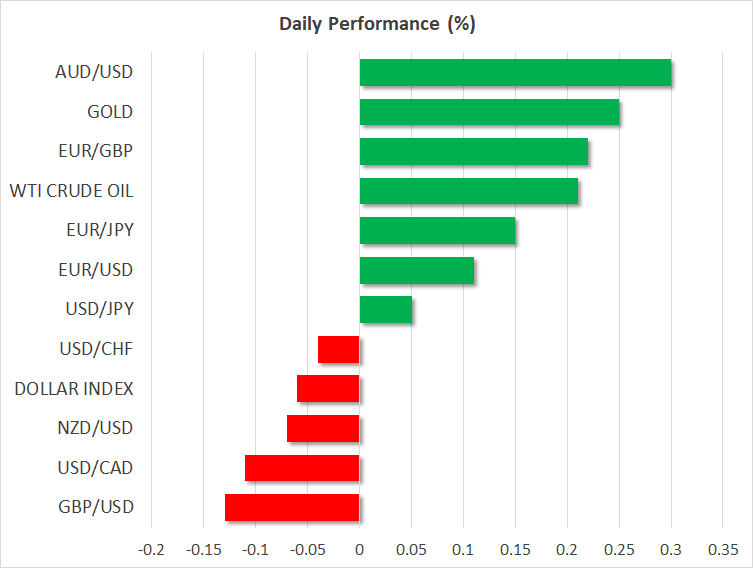

- Meanwhile, antipodeans are mixed amid headlines out of China and the RBNZ

All eyes on Washington as another round of trade talks concludes

Global risk sentiment turned sour on Thursday, with European and American equity markets closing in the red, following a string of disappointing economic data out of both regions. Accordingly, the defensive Japanese yen was the best performer in the G10 FX spectrum. Zooming in on the US, core durable goods orders for December were surprisingly soft, leading to another downgrade in Q4 GDP by models like the Atlanta Fed’s GDPNow, which now projects a mere +1.4% annualized growth. Manufacturing surveys for February pointed to weakness as well, suggesting this slowdown may have persisted through the new year.

As for today, markets will likely focus on the US-China trade talks, the latest round of which concludes in Washington. Expectations that a deal will be concluded soon are still riding high, following reports that the two sides are trying to sketch out the outline of an agreement. The worrisome part is that the only explicit signs of progress are on the ‘simpler’ issues, such as eliminating the trade deficit, with nothing – so far – suggesting a breakthrough on structural matters like IP protection and technology transfer. Hence, much of the optimism now baked into asset prices is likely premature, and for the market to rally further, traders may need to see something concrete – beyond mere rhetoric.

Euro shrugs off soft PMIs, looks to Ifo survey and Draghi

In the euro area, PMI surveys for February were mixed but disappointing overall, with the manufacturing index surprisingly entering contractionary waters amid weakness in Germany, the bloc’s traditional growth engine. A glimmer of hope was provided by the services print though, which rose by more than expected, allaying some concerns. The minutes of the ECB meeting didn’t reveal much either, largely reiterating that the fading market pricing for rate hikes is reasonable given the outlook.

The euro took the (relatively) bad PMI news in its stride, closing the day practically unchanged against the dollar. Today, the highlight on the European calendar will be Germany’s Ifo business survey for February. ECB President Draghi will also deliver remarks at 16:15 GMT. In the big picture, euro/dollar remains well supported by relative yield differentials, which are narrowing in the Eurozone’s favor, implying that any massive downside in the pair – for instance below 1.1213 – looks unlikely for now.

Antipodeans mixed amid conflicting news

In the antipodean sphere, the aussie is outperforming today, after China’s foreign ministry played down the ‘ban’ on Australian coal imports reported yesterday, indicating it’s a quota that applies to all states. Meanwhile, the kiwi is on the back foot, albeit only slightly, after the RBNZ said the increase in bank capital requirements it plans to implement could lead to an eventual interest rate cut, to offset the negative impact on financial conditions.

In the immediate term, how the US-China talks play out may be crucial for both of these trade-sensitive currencies.

Day ahead: Canadian retail sales and Fed speak

Besides Germany’s Ifo survey, the economic calendar is relatively light on Friday, with Canadian retail sales being the only other tier-one release.

As for the speakers, in addition to ECB President Draghi, we will also hear from three Fed policymakers: Atlanta President Bostic (13:40 GMT), New York President Williams (15:15 GMT) and Vice Chairman Clarida (17:00 GMT). Focus may fall mainly on the latter two, who are permanent voting members of the FOMC.