{kind=link}

The US dollar is higher across the board across major pairs as US disappointing data triggered anxiety that lead to a drop in stock markets. As positions were liquidated there was demand for the greenback. US durable goods came in under the forecast but the a more forward-looking indicator the Philly Fed manufacturing Index fell to a negative reading highlighting worsening conditions.

The US central bank has already stressed patience after holding rates unchanged and pausing its balance sheet normalization program. Mixed data has validated their view on the economy, the stock market took the negative indicators as a signal that darkening clouds are more prevalent in the horizon and sought refuge in the US dollar.

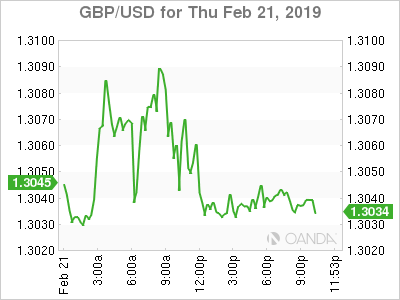

GBP – Pound Lower With no Brexit Breakthrough

The British pound fell 0.11 percent as there was no breakthrough in the talks between PM Theresa May and European Commission chief Jean-Claude Juncker. Talks are ongoing and there will be a parliamentary vote next week. May will work through the weekend meeting with more EU leaders to get a better sense of where they stand. There is still plenty of optimism floating about as spokespersons from both sides stress that a successful deal as soon as possible is the common goal.

Despite the goodwill there hasn’t been much progress as the Irish backstop remains a hurdle keeping the two sides from moving forward. There has been some lateral motion regarding what the backstop is and could be, but so far, no major announcements have been made.

The currency will remain sensitive to Brexit headlines as without details, the comments from policy makers will influence the direction of the market.

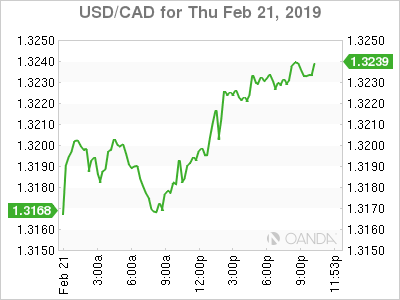

USD/CAD – Loonie Lower Despite Hawkish Poloz

The Canadian dollar fell 0.38 percent on Thursday despite the hawkish rhetoric from Bank of Canada (BoC) Governor Stephen Poloz and wholesale sales data beating expectations. Analysts are looking beyond a potential rate hike by the BoC and economic headwinds beating down on the loonie.

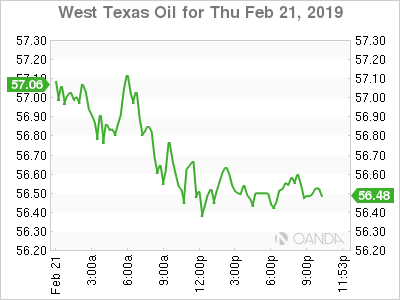

Oil prices have remained stable thanks to the efforts of the OPEC+ by limiting production. The rise of US production has been kept in check, but it remains to be seen for how long those major producers will be able to curb their much-needed revenue to keep prices

US-China trade talks remain on track, but with little details on what the next moves are as the March 1 deadline approaches, the market paid more attention to the lower than expected US data on Thursday.

OIL – Stronger Dollar Puts Pressure on Oil Prices

Oil prices were lower on Thursday as the balance between OPEC+ cuts and rising US production was disrupted by the rising US dollar. Demand for the greenback rose economic headwinds were evident as manufacturing data was softer than expected in the US.

Weekly US crude inventories reported by the EIA came in higher than forecasted at 3.7 million barrels also putting pressure on prices.

The US-China trade talks boosted prices with the promise of higher energy demand if global growth gets back on track, but data this week out of China, Europe and the United States still points to continued weakness and unless there is a major announcement soon the headwinds could push energy prices lower.

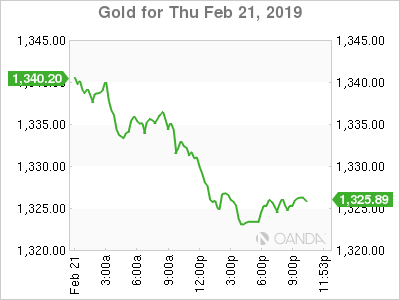

GOLD – Gold Drops as USD Soaks Safe Haven Flows

Gold fell 1.42 percent on Thursday as a strong dollar put pressure on the yellow metal. Gold is still 0.50 higher on a weekly basis, but lower than expected data and positive trade talks between the US and China did not add to a rise in the value of the metal.

The $1,350 price level proved too strong and gold lacked the momentum ahead of the end of the week to go above it. With Brexit and US-China trade talks reaching the final stages as deadlines approach the metal will remain part of investors portfolio as a safe haven. Until there are major breakthroughs or breakdowns in both negotiations gold could remain in consolidation mode.

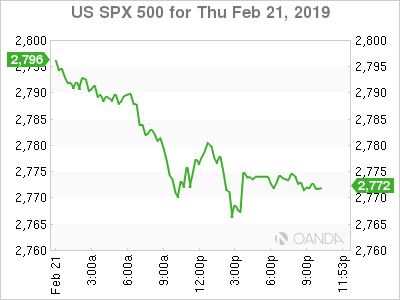

STOCKS – Market Sells News After Weaker US Indicators

Major stock indices were lower on Thursday despite US-China trade talks still remain on track after rumours of imminent agreements in principle are being prepared. Economic data has been weaker, putting a more short-term effect as future risk events have lacked details.

The market sold on the news of disappointing data in the major economies, while trade talks will continue for at least two weeks and could be extended further.