{kind=link}

The global equity rally continues to be bolstered by optimism that the trade war could finally see a framework agreement. The US also avoided a second government shutdown as President Trump accepted the deal lawmakers worked on, only to declare a national emergency to secure additional funds for his border wall funding.

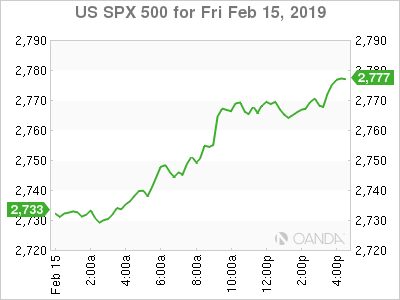

The S&P 500 rose to a 10-week high as trade talks continued to make constructive progress this week and US consumer sentiment showed signs of stabilizing. The main driver for equities remains the trade story and while global growth concerns are the other key risk, the current backdrop of accommodative stances with the Fed, PBOC, and ECB, may make it difficult to derail the bullish argument.

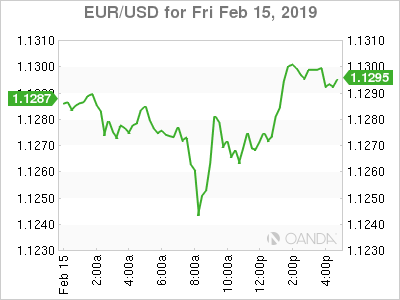

The US dollar continues to whipsaw on risk-off flows from softer US economic data and risk-on moves from continued progress on the trade front. The Fed has clearly signaled interest rates are not going up anytime soon and we could finally learn more in the coming weeks on when the Fed will end quantitative tightening. On Thursday, Fed’s Brainard noted that balance sheet normalization could come to an end this year. Next week, the markets will dissect the Fed’s Minutes on Wednesday and the Fed’s Monetary Policy Report on Friday, along from hearing from Fed members (Williams, Clarida, Bullard and Quarles).