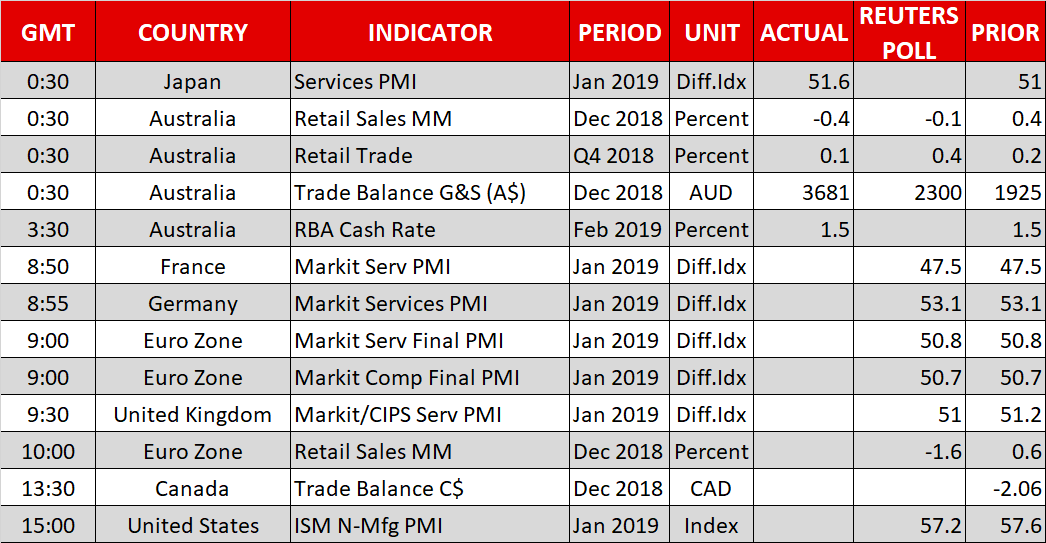

{kind=link}

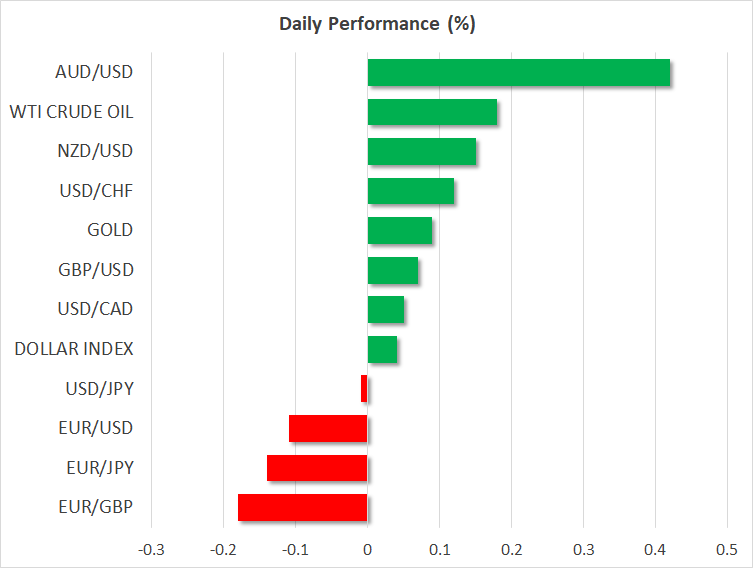

- Stocks climb while haven assets tumble, without any fresh catalyst

- Aussie outperforms after RBA wasn’t as dovish as markets expected

- Today, services PMIs from both the UK and US will dictate the action

Stocks advance, yen crumbles as “no news is good news”

Global risk appetite returned on Monday, in the absence of any material news or fresh fundamental catalysts to speak of. US stock markets recorded decent gains, with the benchmark S&P 500 (+0.68%) closing at a two-month high, while haven currencies like the Japanese yen surrendered ground across the board. Meanwhile, the dollar climbed alongside US Treasury yields, as the risk-on sentiment led to a rotation away from bonds, which are also considered a safe asset.

It’s worth mentioning that all these moves occurred in the midst of thinner-than-usual liquidity, as China and most of Asia are on holiday celebrating the Lunar New Year. Overall, the outlook for riskier assets like equities appears constructive in the near term following the Fed’s latest decision to hit the “pause” button, and amid elevated expectations that the US-China trade negotiations may bear fruit as early as this month.

Aussie celebrates after RBA stays neutral, doesn’t hint at rate cuts

The Australian dollar is outperforming early on Tuesday after the nation’s central bank kept its policy unchanged earlier, as was widely expected, and maintained a relatively neutral tone. Policymakers noted that downside risks have increased, but reiterated that growth will remain above-trend and wages will pick up eventually. Most importantly, the statement contained no hints whatsoever that officials discussed the prospect of cutting rates if the outlook deteriorates, which likely disappointed the bears.

Accordingly, investors unwound some of their rate-cut bets, pushing the aussie higher. Note though, that a quarter-point rate cut by October is still priced in with a 35% probability, so that action remains very much on the table according to markets.

British and American services PMIs coming up

The economic calendar is relatively busy on Tuesday. The UK will kick things off with the release of its all-important services PMI for January. The service sector accounts for 80% of British GDP, so this is a good bellwether for overall economic growth. The forecast is for a downtick, though if the disappointments in the manufacturing and construction indices for the month are anything to go by, the risks surrounding that projection may be tilted to the downside. It seems the UK economy started the year on the back foot as Brexit uncertainties curtailed business investment, and if today’s PMI confirms as much, that could ignite speculation for a dovish tilt by the BoE when it meets on Thursday, hurting the pound.

In the US, the ISM non-manufacturing PMI for January is due out. Expectations are for the index to decline, but to still remain at a very healthy level. The manufacturing index surprised to the upside last week, and if something similar occurs today, that could allay some recession fears, potentially providing a boost to both the dollar and US equities.

As for the speakers, US President Trump will deliver his State of the Union address during the Asian session on Wednesday (0200 GMT). While this is typically a non-market moving event, any hints on whether the government will shut down again soon or whether he will declare a national emergency could make for some interesting headlines