{kind=link}

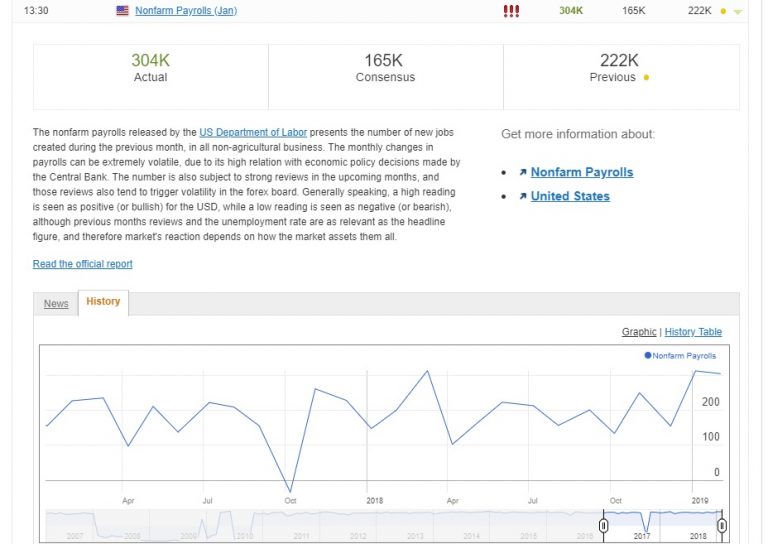

Payrolls well above expectations

The U.S. sprung a blockbuster Non-Farm Payrolls on the markets on Friday, payrolls rising 304,000 vs 165,000 expected.

If the lack of traffic around my neighbourhood in Singapore is anything to go by this weekend, Asia has well and truly settled into Lunar New Year holiday mode. Most of the region will be closed, at least for part of the week as the Chinese welcome the Year of the Pig. This likely means quiet Asian trading sessions.

The region’s highlights will likely come from Australia. Today the Royal Commission releases its findings on the banking sector and tomorrow we have the RBA rate decision. It will be watched closely given the ructions in the housing market.

FX

The U.S. Dollar had a positive Friday session buoyed by the payrolls data. It wasn’t a spectacular rally though, implying that a dovish Federal Reserve continues to be the main story in town.

The Australian Dollar (AUD) may struggle to continue its stronger gains due to tomorrow’s RBA decision and also retail sales. The street will be eagerly searching for any dovish change from the RBA on rates. A shift in stance could bring AUD’s recent rally to an abrupt end.

Regionally, Asia FX trading will be quiet due to holidays with the only highlight being a Philippines rate decision which we expect to be unchanged.

Gold

Gold gave up some of its gains on Friday in the face of a resurgent dollar. Asia will be quiet today with traders content to pick up gold on dips, only a break of 1,300 support would send alarm bells ringing.

Oil

Both Brent and WTI rallied some two dollars on Friday post the sparkling Non-Farm Payrolls. WTI looks the more bullish of the two as cold weather and Venezuela continue to potentially effect the supply situation.