{kind=link}

- Reports the Fed may halt its balance sheet unwind hurt dollar, boost stocks

- Sterling marches higher ahead of decisive week for Brexit

- ECB President Draghi & BoE Governor Carney speak today

Dollar slumps, equities advance on Fed reports & trade optimism

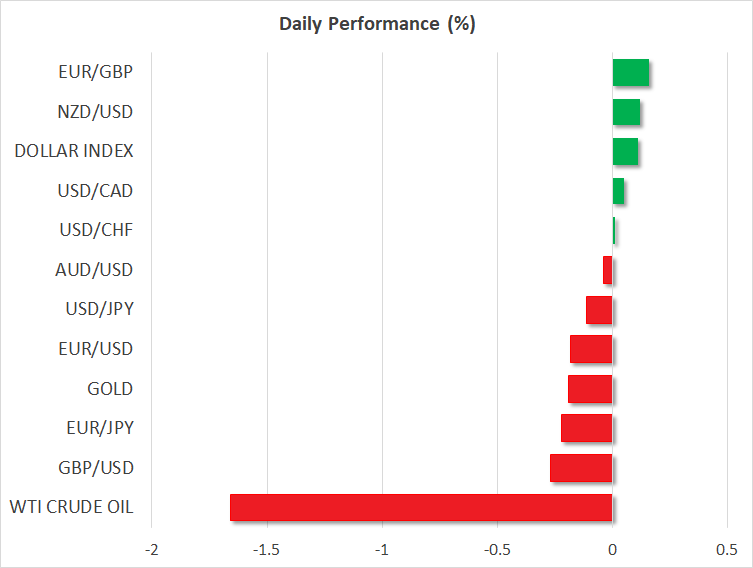

It was a lively session for both currency and equity markets on Friday. The dollar slumped while stock indices climbed, amid renewed speculation that the Fed may turn even more dovish and the US-China talks could bear fruit soon. On the former, a WSJ report suggested Fed officials are considering halting their balance sheet reduction early. The shrinking of the balance sheet amounts to tightening policy; since QE ballooned the Fed’s portfolio to stimulate the economy, it’s unwinding drains liquidity and has similar effects to rate hikes. Therefore, pausing this process is the equivalent of easing monetary conditions, and if this narrative is validated at Wednesday’s Fed meeting, similar market reactions could ensue. Namely, the greenback could suffer while stocks cheer.

On the trade front, sentiment was supported by headlines that Chinese vice-ministers are heading to Washington to lay the groundwork for top-level talks commencing on Wednesday. The early arrival of the Chinese delegation seemingly refueled hopes that a deal may be in sight, further diverting funds into equities and commodity-currencies such as the aussie and kiwi, and out of “safer” instruments like the yen and dollar. Besides these crucial trade talks and the Fed meeting, there is also a plethora of key economic data on the schedule this week, including a US employment report on Friday.

Pound outperforms ahead of deciding week for Brexit

Once again, the British pound was by far the best performer among the major currencies, without any major update on Brexit. Sterling/dollar briefly crossed above the 1.32 mark to record a fresh 3½-month high, as investors unwound more of their previous bearish bets on the UK currency, and amid broad weakness in the dollar.

It’s a critical week for Brexit, as Parliament will vote tomorrow on PM May’s Plan B, and the amendments to it. The narrative behind the pound’s recent rally has been that the risk of no-deal is diminishing as lawmakers get more involved, so for the currency to continue marching higher, it may require clear signals on that front. Specifically, whether MPs vote for the Cooper amendment could be key – this being a plan to avoid a no-deal outcome by extending the exit date. Overall, while the long-term outlook for the pound is clearly brighter, the magnitude and speed of the currency’s latest gains suggest some cause for caution, as the next step in Brexit remains uncertain and sentiment may reverse quickly on any discouraging news.

Coming up: ECB and BoE chiefs deliver remarks, earnings season fires up

While the week is definitely packed, Monday is relatively quiet in terms of data releases. ECB President Mario Draghi and BoE Governor Mark Carney will deliver remarks at 1400 GMT and 1430 GMT respectively. Focus could fall predominantly on Draghi, as the ECB appears to be turning more cautious in light of weakening economic data.

In stocks, the earnings season goes into full swing this week. Caterpillar will release its results today, two hours ahead of Wall Street’s opening bell. The guidance by management could prove crucial for broader market sentiment, as the company is often seen as the “canary in the coal mine” for global growth prospects.

Apple will report its own earnings on Tuesday, Microsoft and Facebook on Wednesday, while Amazon will be in focus on Thursday, among many others.