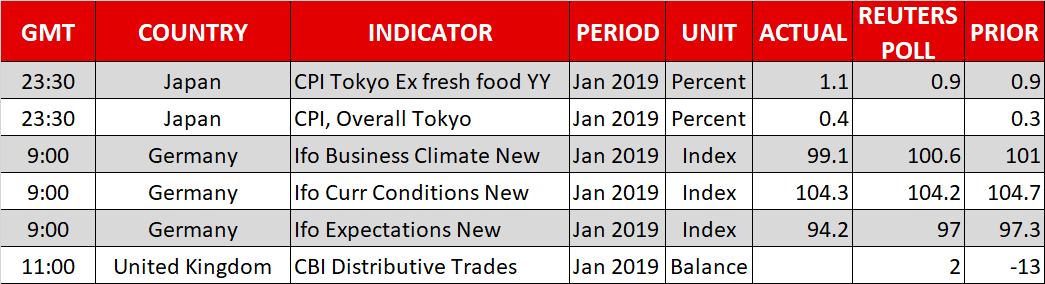

{kind=link}

- Euro closes lower on soft PMIs and ‘vigilant’ Draghi

- Stocks struggle amid conflicting trade signals

- Sterling advances on fresh Brexit reports

Euro caves in after PMIs sink, Draghi ‘keeps his options open’

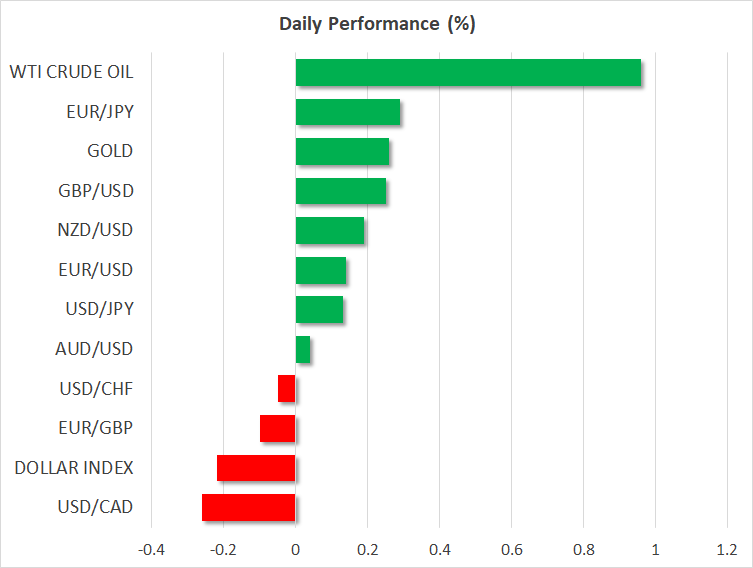

Euro/dollar had a particularly turbulent session on Thursday, before ultimately closing lower, caving under the weight of disappointing PMIs out of the Eurozone and cautious commentary by the ECB. The preliminary manufacturing PMIs out of both Germany and France signaled contraction, revitalizing euro-area growth concerns, while a few hours later the ECB officially downgraded its assessment of risks to the growth outlook.

Draghi maintained a balanced-to-cautious tone. He acknowledged the weakness in growth but counterbalanced that with optimism around wages. Likewise, although he highlighted the Bank’s readiness to act if need be, he seemed hesitant to signal new measures. The message was that while the slowdown is worrisome and may delay any rate hikes should it persist, it’s still not enough to entirely derail the ECB’s normalization plans. Hence, as far as the euro is concerned, everything hangs on incoming data now, as markets try to decipher whether the Bank will hike rates at all this year. Euro/dollar closed below the uptrend line taken from November’s lows and posted a lower low on the daily chart, which technically suggests the short-term bias has turned neutral.

Stocks undecided as Secretary Ross plays both good and bad cop

US equity markets struggled to make headway yesterday, with the S&P 500 (+0.14%) ticking higher but the Dow Jones (-0.09%) inching lower, as mixed signals on the trade front kept traders cautious. The confusion emanated from US Commerce Secretary Ross, who said that the US and China are still “miles and miles away’ from a resolution. Yet, he followed that up by indicating he still thinks there’s a “fair chance we do get to a deal’.

His comments come ahead of a crucial meeting next week between high-level US and Chinese officials. The signals that come out of these talks could be pivotal for market sentiment. Specifically, given recent reports of little progress on key issues such as intellectual property protection, will the US press on for a deal anyway, or use the negotiating leverage it has built up and “wait it out’ until China makes concessions on those fronts? Recall that the agreed deadline for the talks runs out in roughly one month, and there’s still little to show in terms of progress.

In the more immediate term, sentiment seems to have rebounded today, as futures tracking the major US stock indices are pointing to a higher open, while the safe-haven Japanese yen is on the back foot. Asian markets were a sea of green as well, with little in the way of fresh catalysts behind this reversal.

Pound lifted further by Brexit reports

The British pound touched a fresh 11-week high against the dollar earlier today, after UK media reported that the DUP will support PM May’s revised Brexit plan next week, assuming the Irish backstop will be time limited. Markets seemingly interpreted this as improving May’s odds of pushing her deal through Parliament.

Yet, considering the dramatic margin of her previous defeat, and how few MPs the DUP has in Parliament, that may be wishful thinking. To be clear, May will need much more than the DUP’s support to get her deal approved. It’s also a long shot that the EU will accept a time-limited backstop, as it has firmly denied such calls so far. As for the pound, while the long-term picture is unquestionably improving, there’s little clarity on what the next Brexit step will be, implying it probably won’t be all smooth sailing higher from here.