{kind=link}

Industrial production out of Germany, the UK and France will dominate the economic calendar next week, keeping investors’ attention firmly on the growth outlook for 2019. The Bank of Canada will be the first of the major central banks to hold a policy meeting this year, while the highlight in the US will be the ISM non-manufacturing PMI and speeches from Fed policymakers. However, with market moves being mostly driven by jitters about the growth outlook at the moment, economic indicators may struggle to generate much reaction in currency markets. Instead, the market tone could be set by the planned trade talks between the US and China early in the week.

After flash crash, aussie to seek reprieve from data

The Australian calendar will get busier next week after a quiet start to the new year. But with Australia’s economy showing some signs of weakness and futures markets pricing about a 30% probability that the RBA will cut interest rates before the end of the year, the Australian dollar is unlikely to get a significant lift from any positive indicators, while disappointing numbers could push the currency back below the $0.70 handle.

Opening the week on Monday will be the AIG manufacturing index for December and will be followed by the November trade balance on Tuesday. Building approvals for November will be looked at on Wednesday and rounding up the week on Friday will be retail sales figures, also for November.

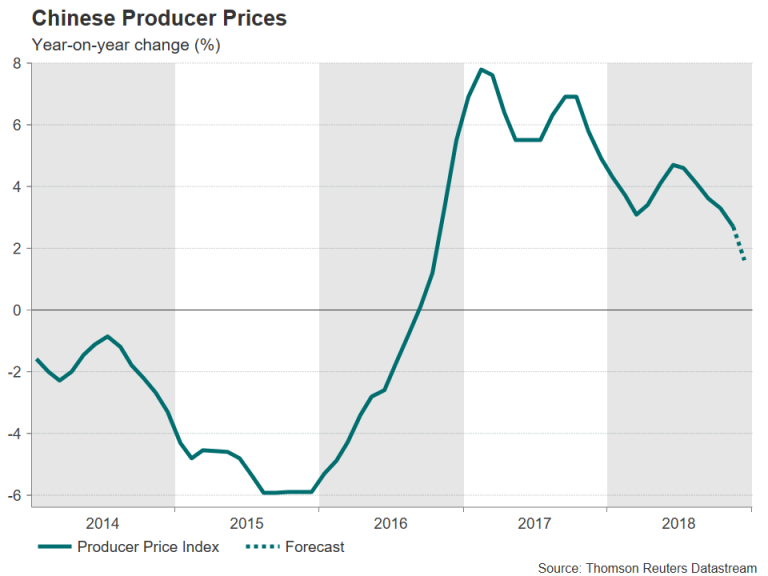

In addition to domestic data, aussie traders will also be keeping a watch on Chinese producer and consumer inflation numbers due on Thursday. China’s producer price index (PPI) is expected to have moderated further in December to an annual rate of 1.6%, highlighting the weakening factory demand for raw materials.

Japanese data could take some shine off safe-haven yen

The yen has had a strong start to 2019 as traders have sought safety in less risky assets amid the darkening outlook for world growth. As Japan’s economy feels the strain of the global slowdown, incoming data is more likely to disappoint than impress, though yen strength should persist as long as markets remain in risk-off mode.

The main releases that will be watched over the coming week are wage figures on Wednesday and householding spending on Friday, both for November. Total cash earnings picked up to 1.5% year-on-year in October, though they remain below the peak of 3.3% scaled back in June. Another quickening in wage growth in November, along with higher household spending, could provide some cushion to the economy as exporters face challenging times.

Eurozone slowdown fears to prevail

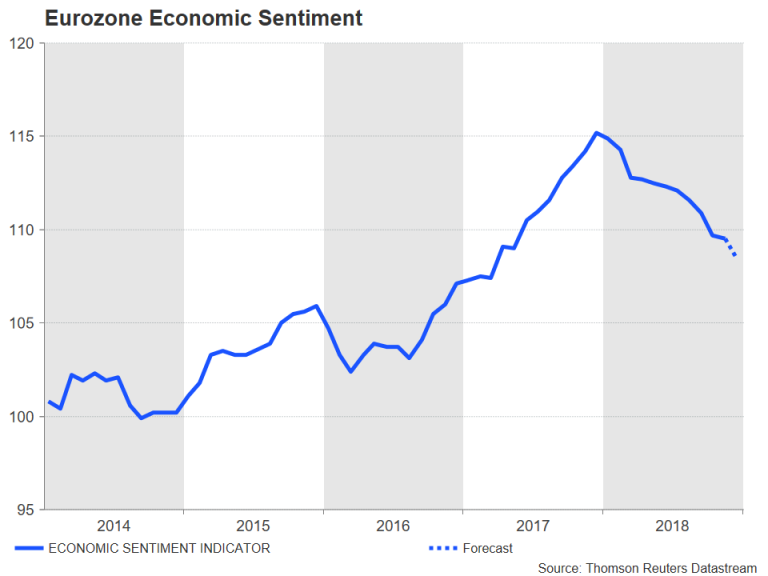

It’s going to be a relatively quieter few days for the euro area with only a handful of major releases. Business surveys will kick off the week, with the Eurozone sentix index due on Monday and the economic sentiment gauge on Tuesday. The economic sentiment indicator slumped to a 1½-year low in November and is expected to fall further to 108.5 in December.

Also attracting attention next week will be industrial output numbers out of Germany and France. Although the figures will be for November and manufacturing PMI prints for December have already been published, they could nevertheless add to the negative sentiment weighing on the euro if they confirm the deteriorating economic backdrop across the single currency bloc. The German industrial output data are out on Tuesday and will be preceded by industrial orders on Monday, while the French figures are due on Thursday. Moreover, November trade numbers are scheduled for release in both France and Germany on Tuesday and Wednesday, respectively.

UK monthly GDP eyed as Brexit stalemate continues

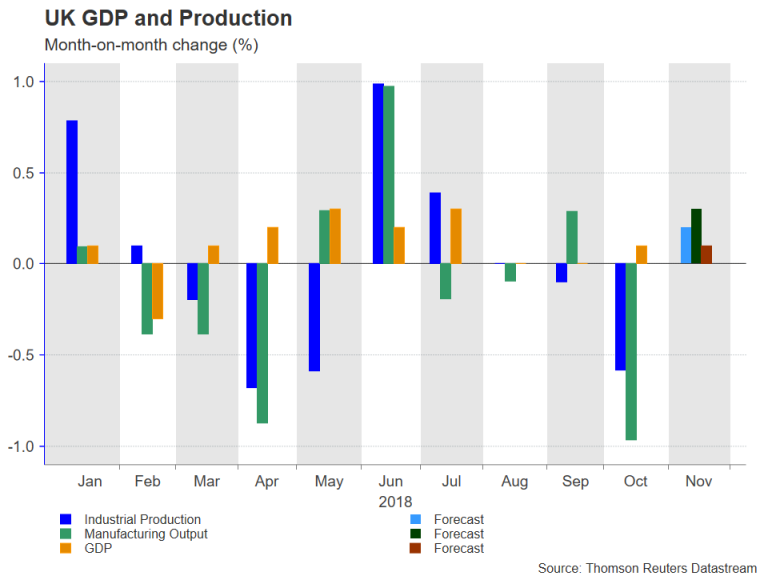

The UK will also publish industrial output and trade stats next week, along with monthly GDP data. Despite the Brexit gloom and the gridlock in Parliament on the withdrawal deal, the UK economy does not appear to have slowed down any more than its European counterparts and probably managed growth of 0.1% month-on-month in November, GDP estimates on Friday are anticipated to show. Friday’s numbers will also include services, industrial and manufacturing output, along with the trade balance.

Industrial production is forecast to have posted its first increase in four months in November, rising by 0.2% m/m. The manufacturing sector, meanwhile, is expected to have expanded by 0.3% m/m, rebounding somewhat from a 0.9% drop in the prior month.

The pound may find some support from potentially better-than-expected figures, but any upside is more likely to come from dollar weakness or positive Brexit headlines.

Bank of Canada meets as rate hike odds evaporate

While the US Federal Reserve has been garnering all the attention on the shifting expectations of interest rate hikes in 2019, the odds of rate increases by the Bank of Canada have also dwindled dramatically since the last meeting. That, along with the slump in oil prices, explains why the Canadian dollar hit a 19-month low of 1.3664 to the US dollar this week. The loonie could face further downside pressure on Wednesday if the Bank of Canada adopts a more dovish view.

The BoC is widely anticipated to hold its overnight rate unchanged at 1.75%. However, should the Bank keep its options open for possible rate hikes in the next few months, the loonie could correct higher.

US-China trade talks on the radar

Moving south of the border, the Fed will also be in the headlines on Wednesday as the minutes of the December 18-19 FOMC meeting are published. But with several Fed speakers on the agenda, including Chairman Jerome Powell on Thursday, the minutes are unlikely to have a big impact on the greenback.

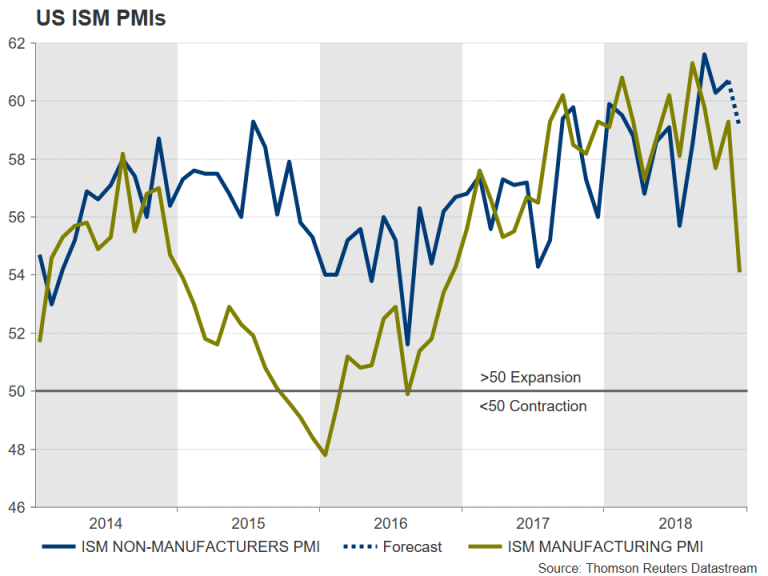

In terms of data, November factory orders will start the week on Monday together with the ISM non-manufacturing PMI for December. The closely-tracked non-manufacturing PMI is forecast to decline to 59.1 in December. After the unexpected big drop in the ISM manufacturing PMI, a similarly weak reading for the non-manufacturing composite could fuel concerns that the US economy may be slowing down sharply and drag the dollar to fresh multi-month lows versus the yen.

Trade figures for November will follow on Tuesday, where the trade balance is forecast to have narrowed slightly. That could be good news for the Trump administration while senior officials from the US and China meet on January 7-8 to discuss how to implement the points agreed between President Trump and President Xi at the G20 summit. Should the meeting prove fruitless, market sentiment could take another turn for the worse, however, if the two sides make substantial progress, risk appetite could receive a massive boost.

Also due on Tuesday is the JOLTS job openings for November and ending the week on Friday is the CPI report for December. Headline inflation based on the consumer price index has eased significantly from the summer high of 2.9% y/y and is projected to moderate further in December, slipping below the 2% mark to 1.9% y/y. The core rate of inflation is forecast to stay unchanged though, at 2.2%. A bigger-than-expected fall in the CPI rate would add to the pressure on the Fed to pause or end its rate hike cycle.