{kind=link}

- US equities stage a major comeback late in the session, close higher

- Dollar edges lower as Fed rate-hike expectations are almost fully priced out

- Yen shines, loonie and aussie flirt with lows amid broader risk-off mood

US stocks stage an impressive late comeback, but skepticism lingers

It was another session characterized by sharp moves in both the currency and equity markets on Thursday amid thinner-than-usual liquidity, and with little in the way of fresh news to drive the price action. The lion’s share of attention was once again on US stocks, which managed to stage a remarkable comeback late in the session, with the likes of the S&P 500 recovering the substantial losses it had recorded until then to close 0.86% higher.

While this was undoubtedly an encouraging development for the bulls, as a second day of gains in equities suggests the latest rebound may not have been a so-called “dead cat bounce”, some skepticism lingers. The broader narrative of a looming slowdown in economic growth hasn’t changed, and reading too much into market moves so late in the calendar year may be ill-advised, as they could be driven mainly by year-end rebalancing flows. The bottom line is that the same themes are still at play, so it may be more prudent to judge the bigger picture by how sentiment develops early in the New Year, when liquidity will start returning to more normal levels.

Dollar sags as Fed expectations get priced out; euro and yen capitalize

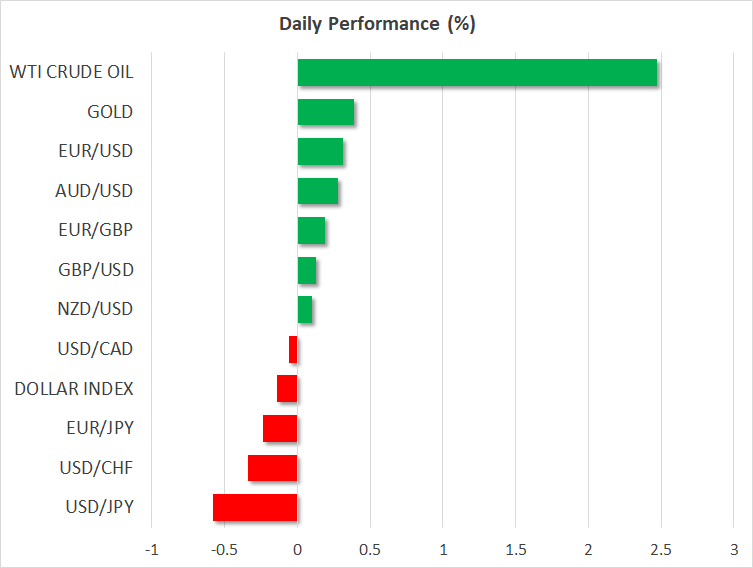

In the currency market, the dollar underperformed most of its major peers, with the euro and the yen being the main beneficiaries of that weakness. The US currency continues to surrender ground overall, as the latest bout of weakness in stock markets was seemingly the “straw that broke the camel’s back” with respect to market expectations around future Fed hikes. To explain, investors have now priced out practically all rate-hike expectations for 2019, effectively betting that the Fed will not dare touch the hike button at all in the face of a slowing economy. This stands in stark contrast to the two rate hikes that the central bank itself penciled in for the same year just last week.

Back to FX markets, the Japanese currency is also outperforming early on Friday amid a generally risk-off mood, paying little attention to a raft of mixed Japanese data released overnight. The Japanese currency has shined in the latter part of December, reclaiming its status as the preferred haven asset in times of market turmoil.

Commodity currencies crumble, aussie flirts with 2-year low

Arguably the hardest hit currencies in the G10 space have been the commodity-linked ones, and in particular the loonie and the aussie. The former tumbled to a 1½-year low versus the dollar yesterday, while the latter briefly touched a 2-year low, both of which are particularly striking considering that the greenback was a major underperformer itself.

The loonie has of course been battered by the broad collapse in oil prices. Separately, the aussie seems to have been battered primarily by the broader risk-off environment, though the fact that markets now foresee a small probability (~20%) for a rate cut in Australia next year amid disappointing data likely contributed too.

Day ahead: German inflation figures due

The highlight on the economic calendar will be Germany’s preliminary inflation figures for December, due at 1300 GMT. Note that the nation’s regional CPIs will be released ahead of the nationwide print, so any moves in the euro may begin even earlier.