{kind=link}

James Comey to Testify in Russia probe

The US dollar is lower across the board and has given all the 2017 gains to end up near pre-elections levels. The turmoil in Washington continues to be the main driving factor for markets with the potential testimony of former FBI Director James Comey on Wednesday the biggest event risk for the greenback. The U.S. Federal Reserve has sent mixed signals via non-voting members on the path of rate hikes but the market still holds a 78.5 probability of higher rates when the US central bank meets in June.

The Bank of Canada (BoC) will release its rate statement on Wednesday, May 24 at 10:00 am EDT. The central bank is heavily expected to hold rates unchanged despite growing pressure from a heating up house market in major cities. The CAD has been caught between a falling dollar and the more aggressive tone of the US regarding NAFTA renegotiation. The US has set in motion the process needed to renegotiate the deal in late August. The Fed will release the minutes from the April Federal Open Market Committee (FOMC) meeting on Wednesday at 2:00 pm. The Fed hosted no press conference in April, leaving the market to wait for the minutes to gather insights into the views of the central bank on the path of rates for the reminder of the year.

Organization of the Petroleum Exporting Countries (OPEC) members met on Wednesday, Thursday and Friday, as part of a panel to discuss the different scenarios ahead of the Thursday, May 25 meeting with non-OPEC members. Sources said that there is no agreement on the final scenario with additional cuts an option as US shale production continues to ramp up.

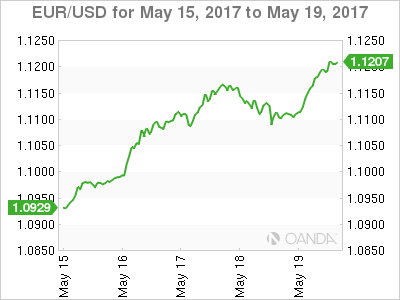

The EUR/USD gained 2.466 percent in the last five days. The single currency is trading at 1.1190 after the USD had a dismal week as more information around US President Donald Trump’s communications were shared after the dismissal of FBI Director James Comey. There has been limited economic data in Europe and the US with the currency pair trading on investor’s risk aversion as political risk focus shifted from Europe to the US.

The U.S. Federal Reserve was active in the markets via the comments of Cleveland Federal Reserve President Loretta Master who was hawkish calling for more rate hikes and warning about waiting too long to hike. On the other side was James Bullard President of the St Louis Fed that called the current path overly aggressive and that the market hasn’t quite bought in to the central bank messaging. The minutes from the FOMC in April will shed more light into what are the different viewpoints inside the rate setting board ahead of the June 13/14 two day meeting that is anticipated will end with higher rates, but current political turmoil and underperforming economic data has put the rate policy decision into question.

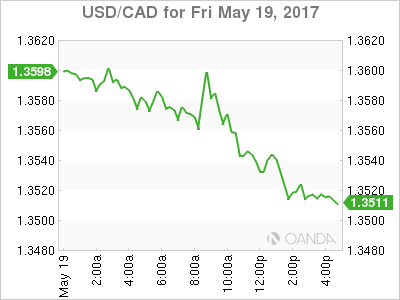

The USD/CAD lost 0.267 percent in the last 24 hours. The pair is trading at 1.3560. The USD has retreated versus the loonie by 1.077 on a weekly basis as political drama has engulfed the Trump administration and President’s Trump handling of information with Russia. The price of oil is rising after a 1.8 million barrel drawdown in weekly US crude inventories and the continued press releases by OPEC members supporting the extension of the production cut agreement.

The financial troubles at alternative lender Home Capital Group was responsible for Moody’s downgrading the six Canadian banks as their risk has grown. Canadian household debt is reaching record levels as historic low rates have fuelled an appetite for credit that has turned the real estate market into a bubble. There has been multiple warnings but its almost a running joke as home owners dismiss the statements from the OECD, World Bank, ratings agencies, the government and the central bank as the boy who cries wolf. The reality is that without higher rates the wolf will certainly not come, but rates will be higher as macro conditions could force the BoC into a raising rates and then it will find Canadian households even deeper in debt.

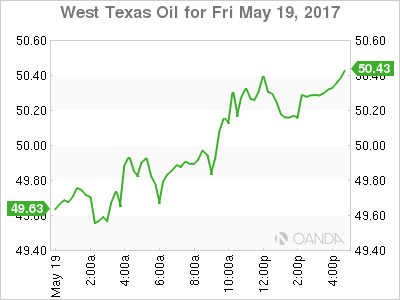

Oil prices gained 2.81 percent on Friday. The price of West Texas Intermediate is trading at $50.19 closing a week where crude gained 5.4 percent after the Saudi Arabia and Russia press release on the OPEC cut extension and the drawdown in weekly oil inventories in the US. The market will be watching next week’s inventories released on Wednesday at 10:30 am and the OPEC meeting on May 25 where more details about the extension will be announced. The oil market has been caught between the OPEC’s efforts to reduce the glut of oil in the market, but as prices have risen so has the levels of US shale production.

Gold has gained 1.741 in the last five days. The yellow metal is trading at $1,251.23 after risk aversion has driven investors to seek a safe haven. The gold rally lost momentum on Friday but is on target to book one of the best weeks for the metal. The uncertainty around the US President and Russian contacts is a developing story that has driven VIX higher and boosted gold as a result. Next week will be an important one for the commodity and the USD as former FBI director could appear before congress to answer questions regarding what Trump did and didn’t tell him about the FBI’s investigations into his campaign connections to Russia.

Market events to watch this week:

Tuesday, May 23

- 4:00 am EUR German Ifo Business Climate

- 5:00 am GBP Inflation Report Hearings

Wednesday, May 24

- 8:45am EUR ECB President Draghi Speaks

- 10:00 am CAD BOC Rate Statement

- 10:00 am CAD Overnight Rate

- 10:30 am USD Crude Oil Inventories

- 2:00 pm USD FOMC Meeting Minutes

- 10:00pm NZD Annual Budget Release

Thursday, May 25

- 4:30 am GBP Second Estimate GDP q/q

- All Day ALL OPEC Meetings

- 8:30 am USD Unemployment Claims

Friday, May 26

- 8:30 am USD Core Durable Goods Orders m/m

- 8:30 am USD Prelim GDP q/q

*All times EDT