{kind=link}

- US dollar not far from highs as Fed poised to hike later in the week

- Risk sentiment under pressure from signs of global slowdown

- Volatile sterling in wait-and-see mode on possible Brexit holiday pause

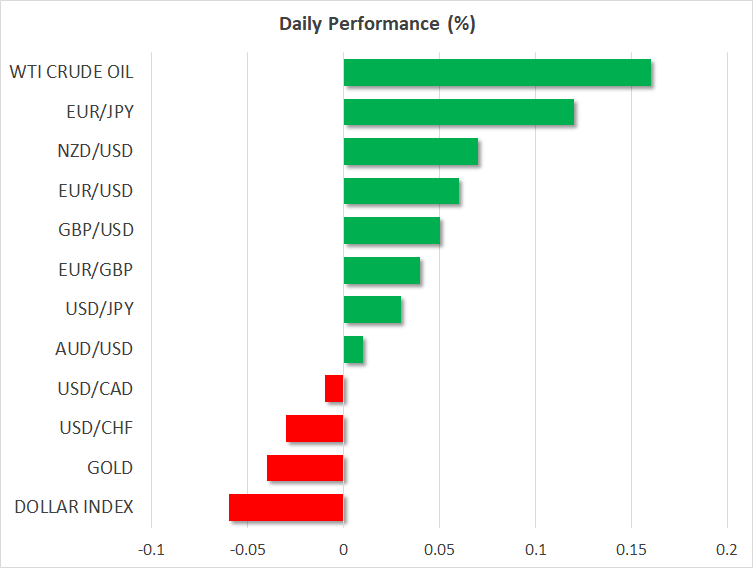

US dollar keeps most of its gains on robust retail sales

The US dollar was helped by a buoyant November retail sales report on Friday, which were in contrast to weaker-than-expected data and business surveys out of Europe and China. A strong consumer should help the US economy post a strong 4th quarter, which in turn could provide the Fed with some ammo in order to hike rates at least one more time in the beginning of 2019. Otherwise the market is bracing itself for a quarter-point rate hike following the Fed’s 2-day meeting starting this Wednesday, but the focus will be on the forward guidance and whether the Fed will lower its forecast for three additional rate hikes next year.

Trade tensions and signs of slowdown keep away Santa Claus rally

Stocks and generally risk sentiment seem to be depressed heading into year-end. The S&P 500 was down almost 2% on Friday and the index is hovering not far from its lows for the year. This during a traditionally strong season for stocks, as December is more associated with stock market rallies rather than declines. The S&P’s decline during December is a sizeable 5.8%. The depressed risk sentiment is also a factor that is helping the dollar for now, as the greenback is seen as a safe haven. In this environment, the dollar has even managed to stand well against the Japanese yen, which is traditionally one of the most attractive choices in times of market stress. Although risk assets have been under pressure, their declines have been ‘orderly’ more or less, in the sense that despite the much higher volatility, there haven’t been signs of panic. Panic could in turn create conditions for a sharp rebound. For risk sentiment to improve, maybe the market needs to see some real signs that the US and China are resolving some of their differences and less vague rhetoric about just how well the talks are progressing. Maybe hopes for a more dovish Fed are also preventing risk sentiment from deteriorating too much.

Impasse causes sterling to sideline for now

Having made 20-month lows versus the US dollar last week on reports that prime minister May would not risk putting her deal with the EU to the country’s Parliament, sterling has since sidelined. The pound even refused to react much to news that May would keep her job for now as she won her party’s vote of confidence. While the clock to the end of March is ticking, the situation seems to be deadlocked. May’s deal stands little chance to pass through Parliament, while the EU is refusing to make extra concessions in order to help May to get the deal approved. There are various scenarios about how this deadlock could break; ranging from a second referendum, general elections, parliament approving a slightly modified deal under the duress of a no-deal Brexit (seems to be May’s gamble for now) or indeed the no-deal option. Barring big surprises, not much clarity is expected before the New Year. In the absence of fresh concrete developments – despite furious backstage deliberations – sterling could enter into a holding pattern near the present lows. In this context, sterling traders could turn their attention to this week’s important economic events and data such as inflation, retail sales, 3rd quarter GDP and last but not least the Bank of England meeting.

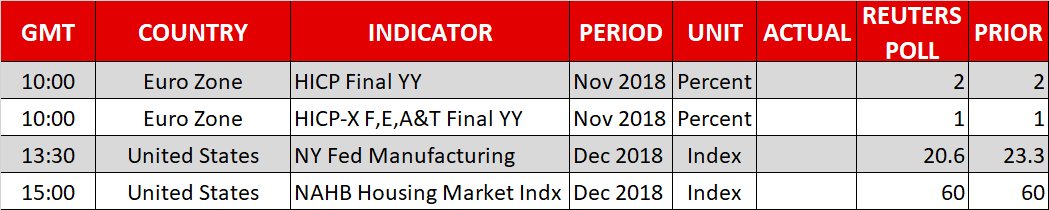

Day ahead: final Eurozone inflation, Empire state manufacturing and US housing index

The day ahead is unlikely to provide much excitement for traders as the key release will be final Eurozone inflation for November – usually a confirmation of the preliminary estimates. Headline inflation is expected to be confirmed at 2%, while core inflation, which mainly excludes fuel and energy, should come in half of that at 1%, showing that inflation is not really an issue for the ECB. In the United States, the Empire State manufacturing index is expected to cool a little to 20.6 from 23.3, while the National Association of Home Builders (NAHB) housing market index is expected to hold steady at 60.