{kind=link}

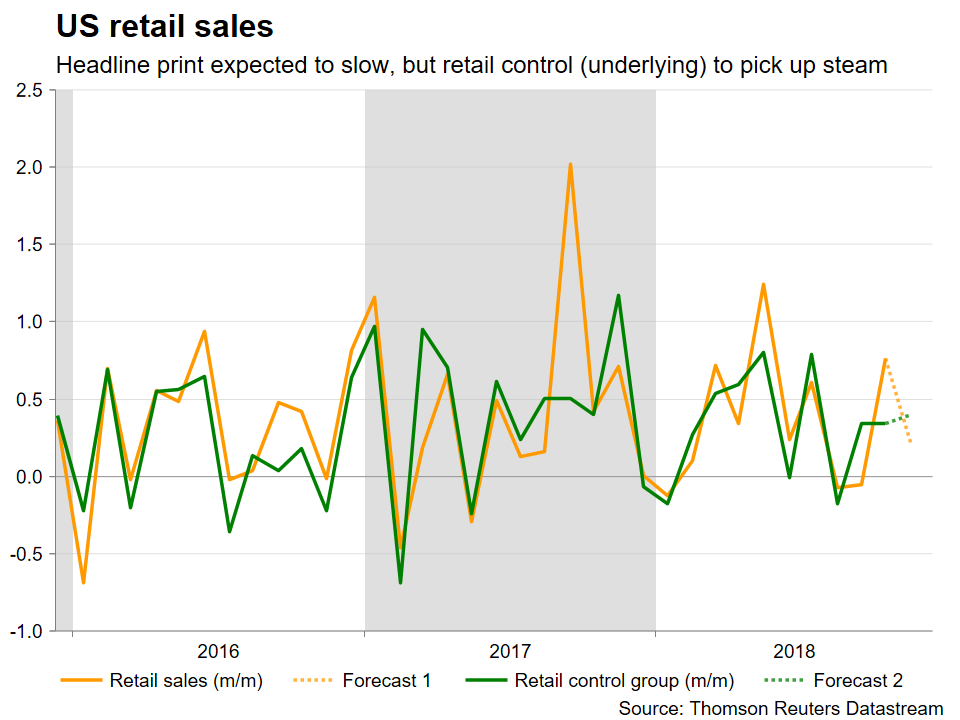

The US will see the release of its latest retail sales figures on Friday, at 1330 GMT. This will be the final tier-one data set ahead of the Fed’s highly anticipated meeting next week, so it may prove especially important for the dollar.

Retail sales are expected to have slowed to 0.2% m/m in November, from 0.8% previously. Likewise, the core print that excludes automobile sales is expected to rise by 0.2%, after clocking in at 0.7% in October. Yet, a ray of hope is provided by the retail control group – the measure that excludes autos, gasoline, and construction materials, and which is used in GDP calculations. That is anticipated to have ticked up to 0.4% in monthly terms, from 0.3% previously. If confirmed, it would signal that the anticipated weakness in the other metrics is owed mainly to volatile items, and thus isn’t an ominous sign for economic growth.

Turning to the greenback, it has held up quite well recently, with the dollar index trading near 18-month highs, even despite a considerable dovish repricing in Fed rate hike expectations. Markets have grown skeptical of whether the Fed will actually raise rates at all next year in the face of a slowing economy, to the point where Fed funds futures now suggest a mere 70% probability for just one quarter-point hike for the whole of 2019.

The currency’s resilience in such conditions suggests it may not require much support from monetary policy to stay in demand, especially since most of its major peers are facing troubles of their own, and hence aren’t particularly attractive at this stage.

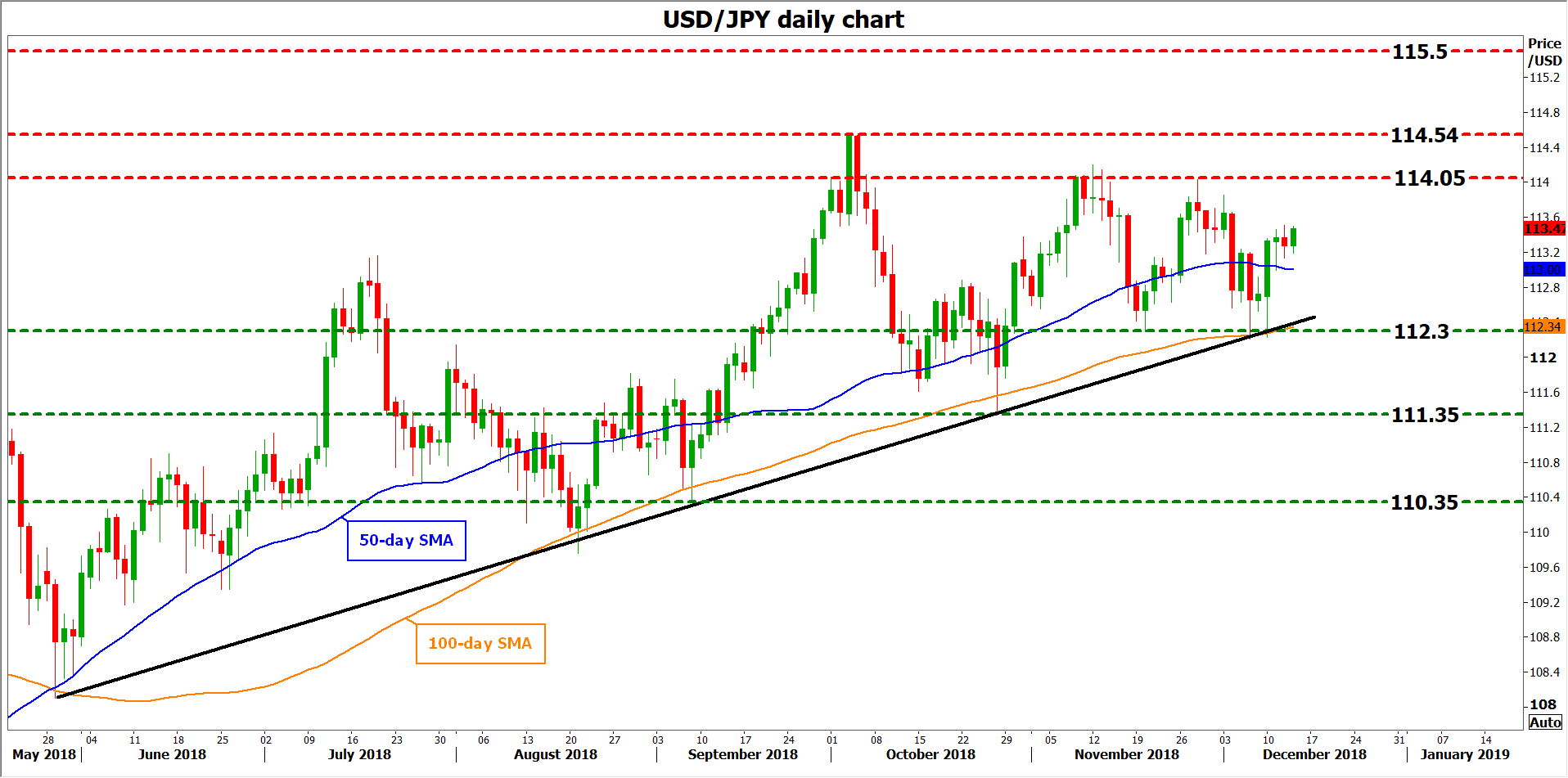

A solid set of data could make investors more confident that a rate increase next year will indeed take place, and perhaps help the dollar regain some ground. Looking at dollar/yen technically, resistance to advances may be found at 114.05, the high of November 28, before the 1-year peak of 114.54 comes into view. Even higher, the top of March 2017 at 115.50 would attract attention. On the other hand, immediate support to declines may come near the 50-day simple moving average (SMA), at 113.00. A downside break could open the way for a test of 111.35, the October 26 low.

In the big picture, the signals the Fed sends next week will probably be the most crucial determinant for the currency’s direction. Assuming the central bank does raise rates as expected, attention will turn to the 2019 rate projections, where investors seem to anticipate a downward revision to signal two hikes during that year, from three currently. Note, however, that the risk of those projections remaining unchanged at three hikes may be greater than perceived, as survey-based measures of the economy like the ISM PMIs remain at very healthy levels, while “hard” economic data have not really deteriorated much. The implication is that if the Fed “stays the course”, the dollar could soar.