{kind=link}

- Stocks in the red as Huawei story ramps up trade concerns

- Pound on the back foot ahead of GDP growth data; May could delay Brexit vote in Parliament

- OPEC-Non-Opec members set supply cut but global growth concerns weigh

Huawei story continues, pushing stocks lower

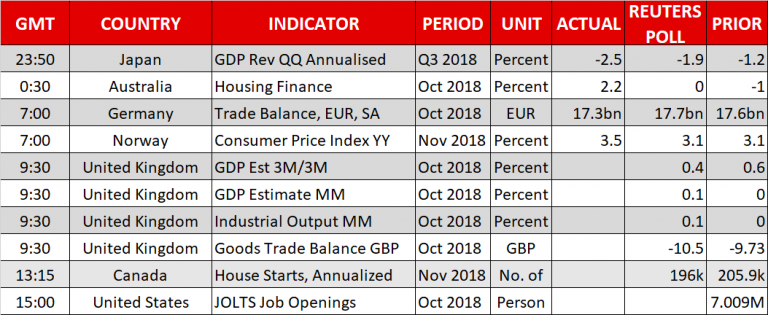

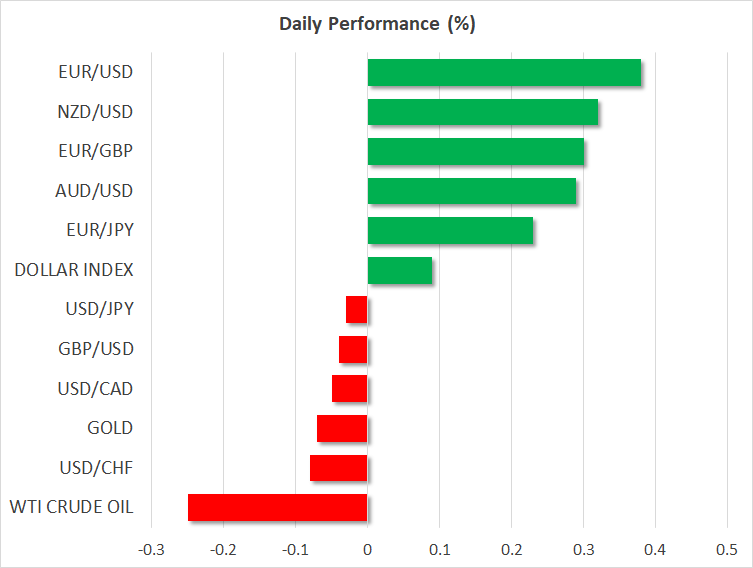

On Sunday, the Chinese government summoned the American ambassador in protest to the arrest of Huawei’s Chief Financial Officer in Canada on December 1, ramping up tensions between Washington and Beijing. Stocks in Asia opened in the red on Monday, with Japanese ones losing the most as an unexpected downward revision in Japanese Q3 GDP growth readings caused sales from funds in the market. Despite its safe-haven feature, the dollar was also trading lower by 0.22% against the yen after Friday’s disappointing Jobs report, which indicated a weaker-than-expected rise in nonfarm payrolls, added further evidence that the Fed might not rush to raise interest rates next year; growth in average hourly earnings stood flat on a yearly basis but in monthly terms it appeared softer. Given the inflamed trade turmoil and worries that monetary tightening in the US will take a pause in 2019, the dollar might face more pressure in coming months. Wall street is on track to open 0.50% lower later today according to US stock futures.

Meanwhile in China, the surprising pullback in consumer and producer prices on Sunday, reflected reluctance from both consumers and businesses to spend,and reduced confidence that the US-Sino trade dispute could end sooner than later. The latter was also echoed by the US Trade Representative, who said yesterday that there is a hard deadline in March and the US President is not planning to delay tariffs on Chinese products beyond that day.

Pound awaits GDP growth data for support but Brexit in the center stage

While investors are fully concentrated on Brexit, eagerly awaiting a negative vote on May’s Brexit plan at the Parliament on Tuesday, the National Bureau of Statistics is expected to say later today that the British economy has slowed down in the three months to October compared to the previous three-month period, from 0.6% to 0.4%. On a yearly basis, GDP growth is anticipated to have ticked up from 1.5% in September to 1.6% but traders will likely remain cautious and show patience instead until the Brexit issue gets resolved. Yet, chances for a solution are currently minimal as divisions within the UK’s political environment about how Brexit should happen threaten to humiliate the British Prime Minister on Tuesday and destroy her political career. In an attempt to avoid these negative consequences, the UK leader could attempt to postpone Tuesday’s Brexit vote today and head to the EU summit on Thursday with scope to seek for some kind of compromise from EU leaders. In FX markets, the pound is consolidating last week’s losses against the dollar around 1.2727, while versus the euro, the currency is facing strong pressure today, falling near to two-month lows.

OPEC agrees production cut levels

After a tumultuous meeting on Thursday, OPEC and other no-OPEC members including the heavyweight Russia agreed to cut production by 1.2 million barrels per day from January (measured against October 2018 levels), with an 800,000 bpd reduction coming from the former and 400,000 bpd decline planned from the latter. The London-based Brent crude closed 2.60% higher on Friday and continued to gain today, last seen around $61.80/barrel (+0.21%). WTI crude though failed to extend upside, reversing back to $52.42 (-0.53%) as disappointing data releases out of China and Japan as well as trade conflicts between Washington and Beijing signal a growth slowdown in global economy.

Other highlights

In other events of interest, Eurozone Sentix investor confidence could affect the euro at 0930 GMT, with analysts anticipating the measure to slowdown for the fourth consecutive month, while political risks in Italy and in France are likely to keep buying interest subdued.

In the US, the calendar features JOLTs Job openings at 1500 GMT, whilst in the neighbor Canada, building permits at 1330 GMT could provide support to the loonie which rallied significantly on Friday in the wake of an upbeat employment report.

Elsewhere, kiwi traders will likley pay attention to electronic card retail sales out of New Zealand at 2145 GMT.