{kind=link}

Here are the latest developments in global markets:

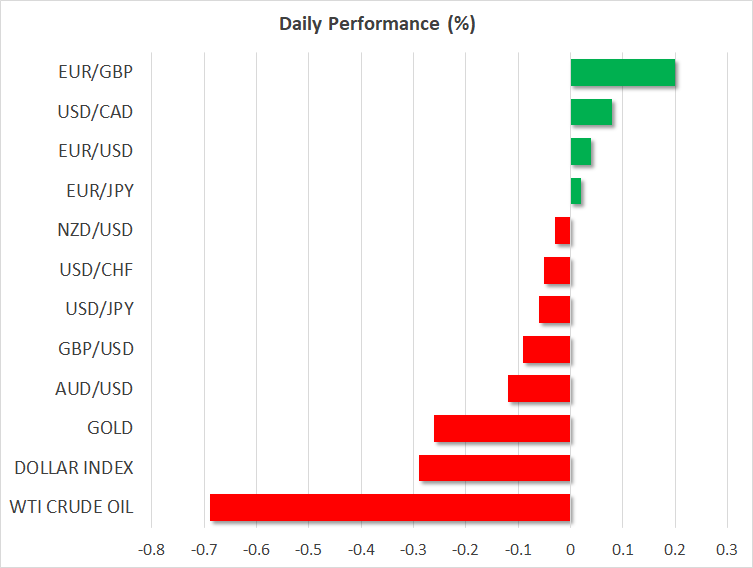

FOREX: The dollar is nearly 0.3% lower against a basket of six major currencies on Friday, looking set to post a third day of declines in a row, without any fresh catalyst behind these moves. Meanwhile, the British pound soared on Thursday, buoyed by news that EU and UK negotiators reached an accord on the draft political declaration, setting the stage for the deal to be approved by EU leaders over the weekend.

STOCKS: US markets remained closed on Thursday for Thanksgiving, though futures tracking the S&P 500, Dow Jones, and Nasdaq 100 are pointing to a lower open today. In Asia, Chinese indices closed significantly lower on Friday amid jitters around whether a ‘trade ceasefire” will ultimately be agreed next week. Meanwhile in Europe, all major benchmarks were expected to open higher today, according to futures.

COMMODITIES: Oil prices remained in the doldrums, with both WTI and Brent erasing their recent rebound to test once again the one-year lows they recorded earlier in the week. Both benchmarks appear ready to post their seventh consecutive week of declines, as oversupply concerns continue to weigh. The only bright spot on the horizon that could help prices stabilize at least, would be clear signals from OPEC that it intends to cut its production as we approach its next gathering on December 6. In precious metals, gold prices are lower by 0.27% at $1,222 today, even despite the US dollar being in the red as well.

Major movers: Sterling crawls higher on Brexit news; risk sentiment still fragile

The British pound was the best performer on Thursday, bolstered by news that EU and UK negotiators finalized the draft political declaration outlining how EU-UK trade, security, and other issues would function. This lays the groundwork for the deal to be approved by EU leaders over the weekend, before it is brought to the UK Parliament. While the EU appears practically certain to accept it, the same cannot be said for UK lawmakers, as nearly every faction of Parliament – including Labour, Tory Brexiteers, pro-EU moderates, and the DUP – has threatened to vote it down.

Hence, the picture remains highly uncertain, particularly since nobody can confidently predict how things will play out if UK lawmakers reject it. Accordingly, the pound will likely stay headline-driven and choppy for a while longer. As for the actual vote though, the risks surrounding sterling from it may be asymmetric and tilted to the upside, with a potential approval likely to generate a bigger positive reaction than the corresponding negative one in case of a rejection. Given the broad opposition to the deal, an approval would come as a surprise. Coupled with the fact speculative positioning in sterling is still heavily net-short, these imply the currency could explode higher if Parliament votes in favor of the accord, as numerous investors rush to unwind or cover their prior short bets.

In Europe, the single currency barely reacted to the ECB minutes yesterday, which contained nothing new. Elsewhere, there was little else in terms of news flow, with US traders having taken the day off to celebrate Thanksgiving. Risk sentiment remains in “risk-off” territory, with US equity futures pointing to a lower open today, albeit not significantly so. Consequently, the aussie and the kiwi are on the back foot, while the defensive yen is trading on a slightly stronger note.

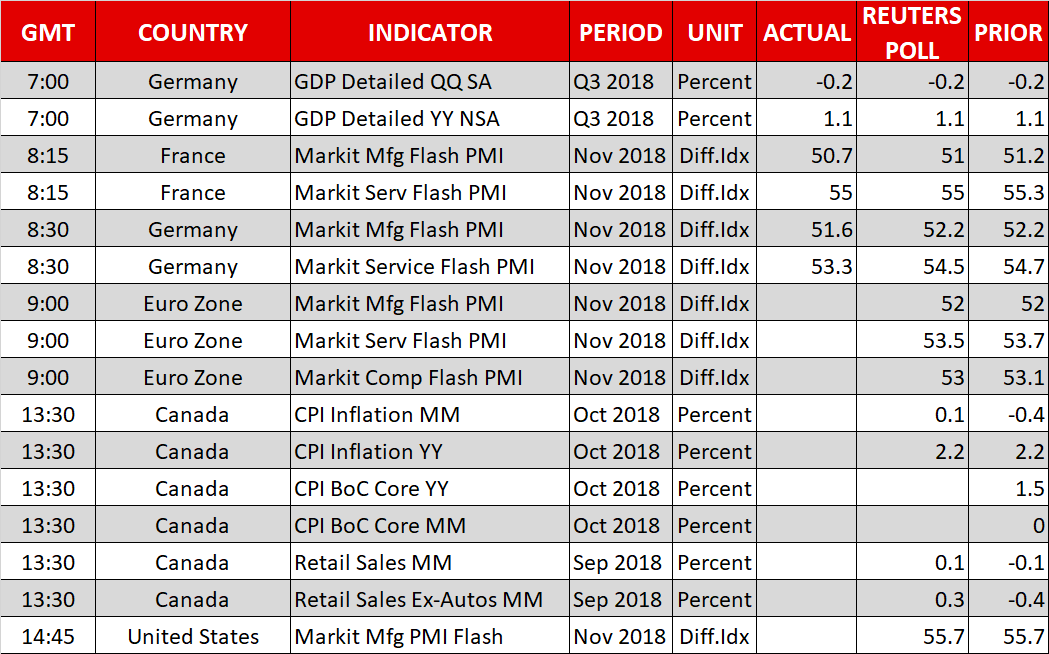

Day ahead: Eurozone flash PMIs, Canadian inflation & retail sales, Markit’s US manufacturing PMI due; Brexit developments eyed

Eurozone PMIs and key data out of Canada are on the agenda on Friday, while the US will be on the receiving end of Markit’s manufacturing PMI. Meanwhile, any Brexit headlines will be eyed after Britain and the EU agreed on a text setting out their future relationship.

Flash eurozone PMI estimates for November will be made public at 0900 GMT. The readings are not expected to reflect a pickup in euro area economic activity during Q4. Indicatively, the composite PMI, which is viewed as a good overall growth indicator for euro area economies, is anticipated at its lowest in more than two years. Still, all three measures are projected to remain in expansion territory above 50.

Another disappointment in eurozone data will likely spur speculation for a relatively dovish ECB during its December meeting. Evidently, investors are starting to increasingly challenge that the central bank will be able to deliver a 10bps rate hike during the latter part of 2019, with that outcome being priced out by markets, albeit only on the margin.

Elsewhere, Germany and France, the two largest economies in the eurozone, saw the release of their respective flash PMI prints earlier in the day, with the euro experiencing losses in the aftermath of worse-than-expected German numbers.

Remaining in Europe and turning to Brexit, despite Britain and the EU agreeing on a draft text, hurdles remain, and sterling – as well as the euro to an extent – will remain sensitive to developments. More specifically, PM May will be back in Brussels to talk with the EU’s Juncker on Saturday and address the EU heads of state on Sunday. EU leaders will need to sign off the agreement, but before that Spain needs to get on board, overcoming issues that have to do with Gibraltar. Given that the EU 27 endorse the deal, May would still need the support of the UK parliament and so far things don’t look that rosy for her on this front.

Out of Canada, important monthly data on inflation and retail sales will be made public at 1330 GMT. Better-than-expected numbers may fuel speculation for a rate increase by the Bank of Canada during its January meeting, something which would help the loonie; at the moment, swap markets assign a 75% probability for a January move by the BoC. It bears mention that the Canadian currency will also be turning its sights on oil prices for direction.

The US will be on the receiving end of Markit’s flash manufacturing PMI for November at 1445 GMT.

In terms of policymakers’ appearances, RBA Governor Lowe will be giving a speech at 2215 GMT.

In energy markets, Baker Hughes data on active oil rigs in the US are due at 1800 GMT.

In the meantime, today’s Black Friday, the day that marks the start of the US holiday shopping season. Retailers such as Amazon hope to cash in after running big discounts.

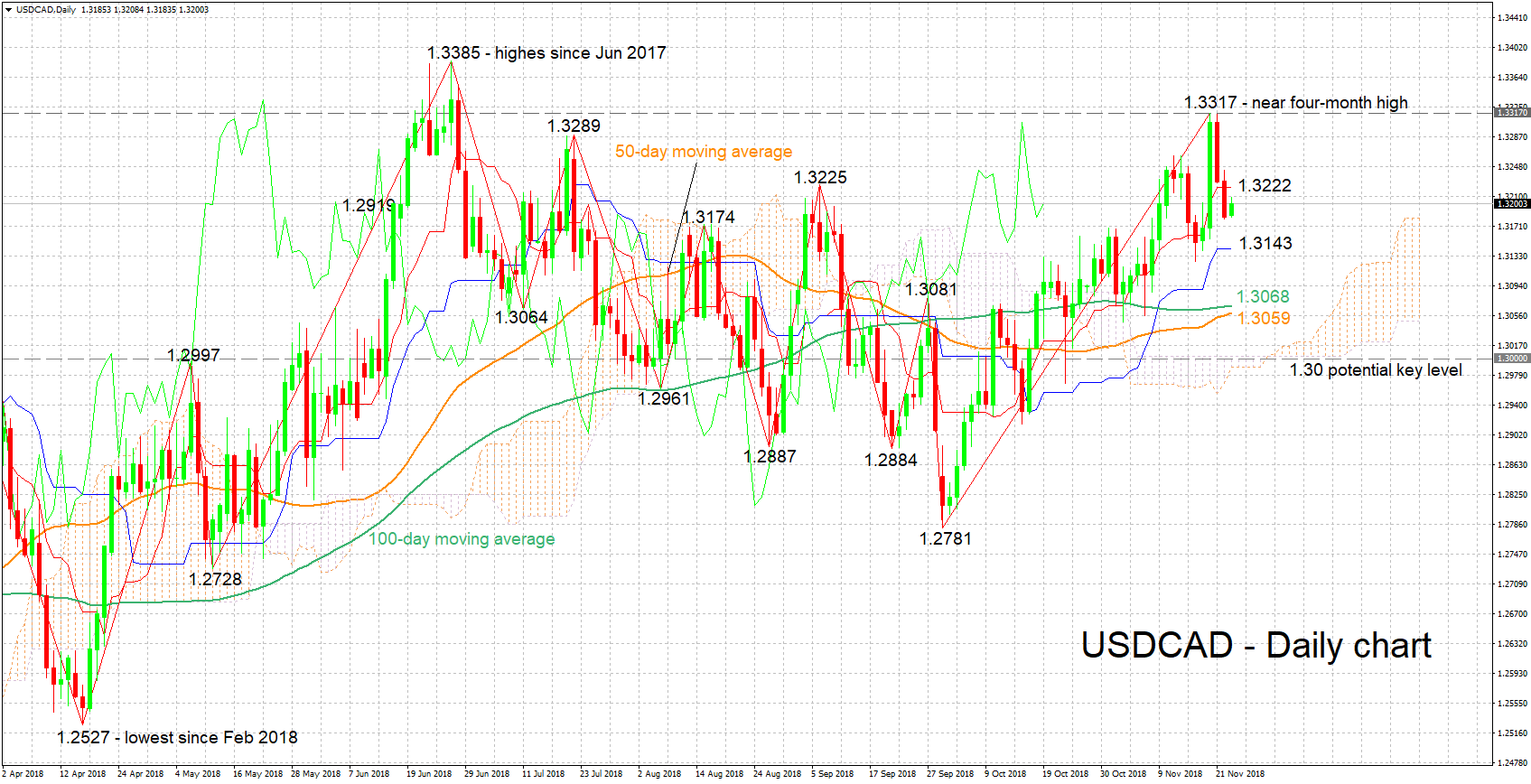

Technical Analysis: USDCAD bullish bias may be easing

USDCAD lost ground after touching a near four-month high of 1.3317 on Tuesday. Despite the fall, the Tenkan- and Kijun-sen lines remain positively aligned in support of a bullish bias in the short term. Notice though that the two have stalled their advance, the implication being that bullish momentum may be easing.

Upbeat data out of Canada can exert selling pressure on the pair. Support to losses may come around the current level of the Kijun-sen at 1.3143. Lower, the zone around the 100- and 50 day moving average lines at 1.3068 and 1.3059 respectively would be eyed for additional support.

On the upside and in the event of disappointing Canadian figures, resistance could occur around the Tenkan-sen at 1.3222. Higher still, Tuesday’s peak of 1.3317 would increasingly come within scope; the area around this includes the 1.33 handle, as well as another top from previous months at 1.3289.

The movement in oil prices can also affect the loonie, as Canada is one of the largest oil exporters in the world.