{kind=link}

Here are the latest developments in global markets:

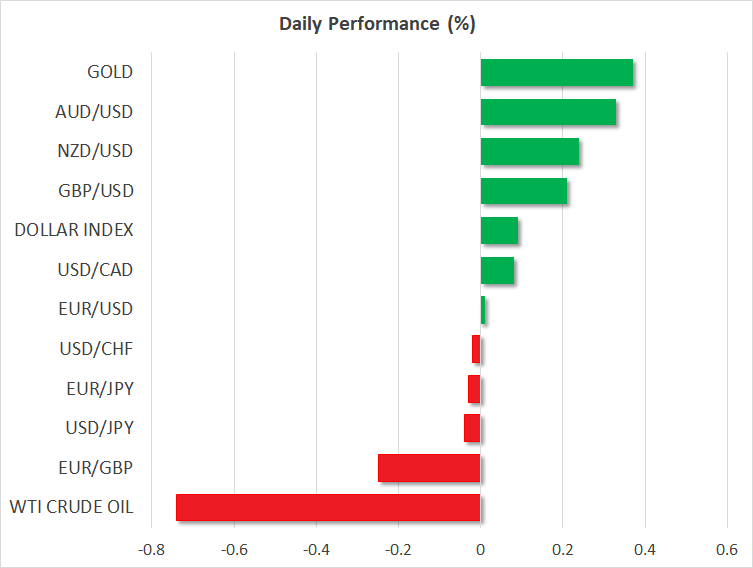

- FOREX: The US dollar hit one-month highs against the yen at 113.44 on Tuesday but it soon lost ground returning to 113.13 (-0.06%) before US midterm elections take place later today. The US dollar index, however, managed to climb by 0.14%, erasing some of yesterday’s losses on the back of a weaker euro and pound. Euro/dollar retreated by 0.10% despite the upward revision in final Markit Services PMI figures for October out of Germany and the Eurozone. Eurozone producer prices appeared better-than-expected as well in September, while August PPI readings were revised upwards. Regarding the Italian budget Eurozone finance ministers asked Italy to rethink its fiscal demands yesterday, while the European commissioner, Piere Moscovici argued today that sanctions can be applied if Italy shows no compromise. Pound/dollar reversed back down to 1.3036 after Jeffrey Donaldson, a DUP lawmaker, twitted that Britain “looks to be heading for no deal Brexit”. Earlier the pair had touched a new two-week high at 1.3084. As long as there isn’t anything concrete regarding the progress of negotiations, downside corrections are likely in the market. Euro/pound and pound/yen are in negative territory, inching down by 0.02% and 0.15% respectively. Turning to the antipodean currencies, aussie/dollar increased by 0.33% at 0.7231 after the Reserve Bank of Australia (RBA) left the cash rate unchanged at 1.5% for the 25th consecutive meeting as widely anticipated. Aussie/yen traded higher as well by 0.28%. Kiwi/dollar followed aussie’s upside structure, gaining 0.11% at 0.6668. Dollar/loonie climbed by 0.11% to 1.3122.

- STOCKS: European equities extended lower on Tuesday except for the Italian FTSE MIB which was up by 0.20% at 1100 GMT. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 declined by 0.29% and 0.47% respectively. The German DAX 30 moved lower by 0.31%, the French CAC 40 fell by 0.31%, while the British FTSE 100 weakened by 0.35%. The worst performer was the Spanish IBEX 35, tumbling by 1.02% thanks to significant losses in consumer non-cyclicals. Among Spanish companies, the retailer Distribuidora Internacional de Alimentacion SA was downgraded by Deutsche Bank. In Asia, the majority of stocks closed strongly positive, while futures tracking US indices such the S&P 500, Dow Jones and Nasdaq 100 were slightly down, pointing to a softer negative open as investors await the US midterm elections.

- COMMODITIES: Oil prices were on the back foot amid fears US sanctions imposed on November 4 would disrupt oil supply in Iran, OPEC’s third largest producer. Yet waivers granted to some of Iran’s main oil buyers, provided some relief to investors, curbing steeper declines in the market. Meanwhile Iran asked OPEC’s Secretary general to scrap two committees which monitor a deal between OPEC and other countries led by Russia, saying that some of the OPEC members participating in the deal have taken sides with the US. WTI crude and Brent were changing hands lower at $62.92/barrel (-0.30%) and $72.92/barrel (-0.34%) respectively. In precious metals, gold advanced by 0.34% to $1,235/ounce.

Day ahead: US midterm elections kick off; New Zealand to report on employment

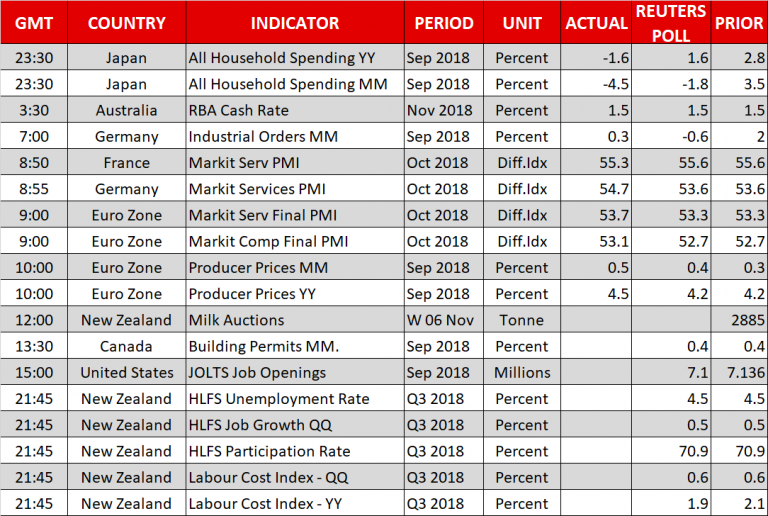

After two years since Trump’s victory in presidential elections, the US will head to the polls on Tuesday to choose members for each of the 435 House seats and 35 out of 100 Senate positions in Congress. While Trump’s Republicans are currently in charge in both chambers, polls suggest that the opposition Democrats have a decent chance to take the House of Representatives. If that comes true, Democrats could derail the president’s agenda, restricting Trump’s ability to pass new laws. On the other hand, if Republicans maintain control in the Congress, which is a less likely outcome, it would be another checkpoint for the US president and a dollar-positive event. Note that a party needs to win 218 seats out of 435 in the House to take power.

As vote results are not expected until Wednesday, US JOLTs job openings might attract attention at 1500 GMT. Forecasts are for available positions to have increased by 7.1 million in September, slightly less than in August when the measure showed an increase of 7.13mn.

In the meantime, employment figures for the third quarter will be a hot spot in New Zealand before the Reserve Bank meets to set monetary policy late on Wednesday. Analysts believe that employment grew by 0.5% q/q in the three months to September as in the previous quarter, while the unemployment rate steadied at 4.5%, which is the second lowest rate recorded since the end of 2008. In terms of costs payed to employees excluding overtime, benefits are said to have risen at the Q2’s pace of 0.6% in a quarterly basis, while year-on-year these are expected to have slowed down, showing an expansion of 1.9% compared to the 2.1% growth identified previously, which was the highest advance in six years. Should the data appear better than projections, the kiwi could see additional gains and vice versa. Encouraging numbers may also bring smiles to the RBNZ policymakers who target employment in addition to inflation to achieve a sustainable growth in the economy.

Besides the above, the outcome of the bi-weekly milk auctions is highly expected to bring volatility to the kiwi at a tentative time given that dairy products are a top export in New Zealand. China’s Premier Li Keqiang will be meeting the heads of IMF, World Bank and World Trade Organization in Beijing as part of an annual meeting.

Any headlines regarding the trade story, Brexit and the turnoil around the Italian budget will be valuable to the markets during the day.

Elsewhere, September’s building permits will come in public at 1230 GMT.

In energy markets, the API weekly report on US crude inventories will be closely watched for direction at 2130 GMT.