{kind=link}

Traders will be turning to quarterly employment numbers out of New Zealand on Wednesday (21:45 GMT, Tuesday) to decide whether the kiwi’s rebound from the October lows can be extended. More significantly, the jobs data could provide an indication as to whether the Reserve Bank of New Zealand will maintain a dovish tilt or turn a little hawkish at its policy meeting a day later on Thursday.

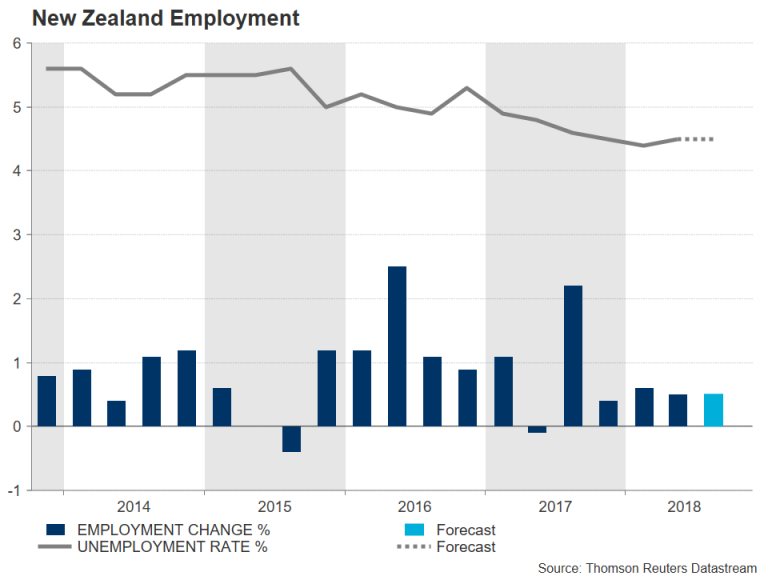

Economic indicators out of New Zealand have been a bit more encouraging in recent months following the moderate deterioration of the economy seen during and after the September 2017 general election. GDP expanded by more than expected in the second quarter to the highest rate in two years, surging by 1% over the period, and inflation accelerated by more than anticipated during the third quarter. Annual inflation hit 1.9% in the three months to September, taking the CPI rate closer to the middle of the RBNZ’s 1-3% target band. Although the core price gauges remained subdued, the inflation data overall helped trim the odds of a near-term rate cut by the RBNZ.

Wednesday’s employment report could further diminish talk of a possible rate cut if, as expected, the jobless rate holds steady at 4.5%. The rate of jobs and wage growth will also be watched for assessing the health of the labour market. Jobs growth stood at 0.5% in the second quarter and a similar pace of growth is forecast for the third quarter. An unexpected slowdown in employment growth would not bode well for third quarter GDP performance.

Even more significant will be the quarterly wage figures. New Zealand’s labour cost index rose by 0.6% quarter-on-quarter in the April-June period, taking the annual rate to a 6-year high of 2.1%. Wages will likely rise again by 0.6% on a quarterly basis but the annual rate is forecast to slow slightly to 1.9%. A sharper deceleration would weaken the outlook for inflation and, while the base case scenario for the next RBNZ move is still a hike, it would keep open the prospect for a rate cut.

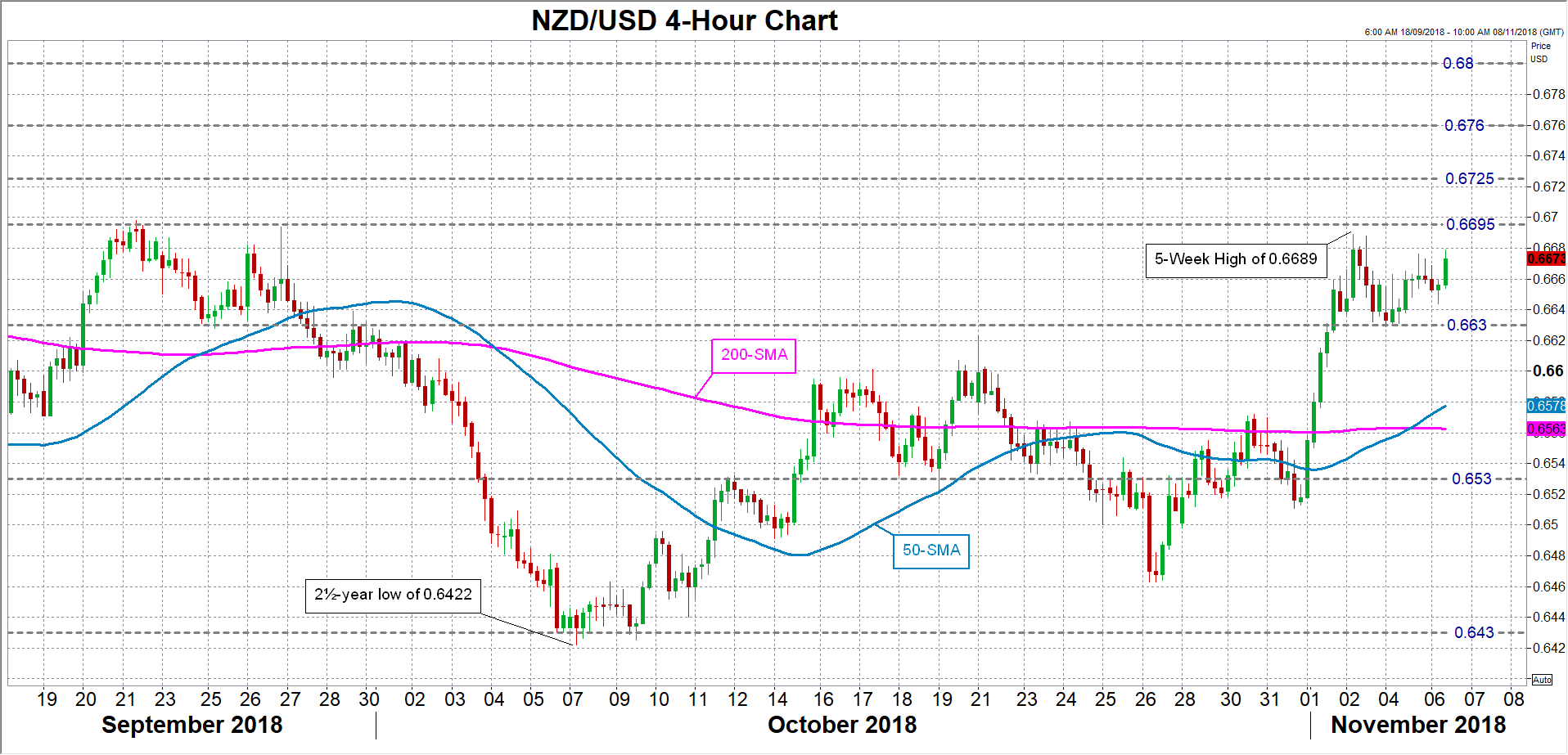

The New Zealand dollar is vulnerable to negative surprises in Wednesday’s data, especially as risk sentiment remains fragile given the receding expectations of a quick resolution to the Sino-US trade dispute and a choppy recovery in global equities. Kiwi/dollar could break above immediate resistance at around 0.6695 if the employment figures beat the consensus forecast. A rise above the 0.67 handle could see the pair stumbling at the 0.6725 and 0.6760 hurdles before attention turns to the critical 0.68 level.

However, should the jobs numbers disappoint or raise doubts about the economic outlook, kiwi/dollar could seek support initially around the 0.6630 level. A drop below this mark would take the pair towards the 0.6565 region, which is where the 50- and 200-period moving averages intersect. Further down, the 0.6530 level could stall further declines as this area has acted as support in the past. A breach of this support would open the way for October’s 32-month low of 0.6422 and reinstate the pair’s medium-term bearish structure.