{kind=link}

Here are the latest developments in global markets:

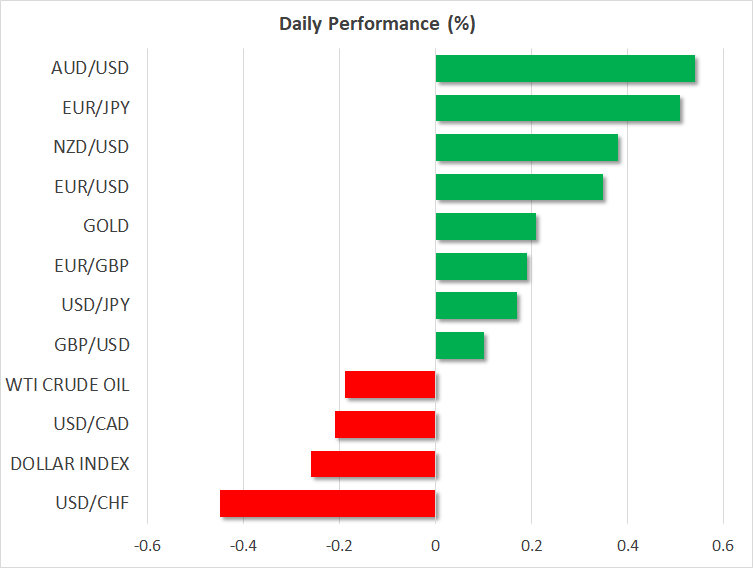

FOREX: Dollar/yen eased to 112.81 but remained up on the day (+0.12%) after rising as high as 113.10 early in the European session as investors were looking for details to confirm that the US President and the Chinese leader will attempt to reach a trade agreement at the G20 summit in Argentina later this month. This came after reports that the government heads had a constructive phone call yesterday, with China’s foreign ministry providing some support to the optimism today, saying that the sides want to enhance their trade relations. The dollar index, though, was weaker around 96 (-0.24%) as the euro and the pound continued to strengthen. The NFP job report is likely to give further direction to the dollar later today. Euro/dollar increased positive momentum towards 1.1443 (+0.32%), shrugging off disappointing manufacturing PMIs out of Eurozone; October’s index was revised slightly downwards to 52 from 52.1 forecasted and 53.2 seen in September, to the lowest since August 2016. Euro/yen posted stronger gains, jumping by 0.43%. In the UK, prospects that the EU and the UK have trucked a tentative deal to allow British financial services companies to access European markets after Brexit were somewhat downplayed. Yet governmental officials said that negotiations continue progressively. On Wednesday a letter revealed that the British Brexit Secretary is hoping for an agreement by November 21. Pound/dollar extended yesterday’s bullish move to 1.3045 before inching down to 1.3024 (+0.12%). The trade-sensitive antipodean currencies were overperforming at one-month highs, with aussie/dollar bouncing by 0.60% and kiwi/dollar winning 0.38%. Dollar/loonie and dollar/swiss franc were on the back foot, losing 0.45% and 0.25% respectively. In emerging currencies, the Chinese onshore yuan was in bullish mode, crawling up by 0.75%.

STOCKS: European equities joined the rally in Asian stock markets on Friday on hopes that the US and China are looking to resolve their trade standoff despite worse than expected earnings results from the giant tech Apple on Thursday. The pan-European STOXX 600, climbed by 1.04% to two-week lows at 0940 GMT, while the blue-chip Euro STOXX 50 gained 0.75%. The German DAX 30 improved by 1.15%, the French CAC 40 rose by 1.20% and the Italian FTSE MIB added 1.33% to its performance. UK’s FTSE 100 was up by 0.67%. In the US, futures tracking Dow Jones. Nasdaq 100 and S&P 500 were in the green, pointing to a positive open.

COMMODITIES: Crude markets are set to close lower for the fourth straight week as concerns over rising inventories keep sentiment subdued. News that the US government has spared waivers to some of Iran’s closest trade partners such as South Korea, Japan and India before US sanctions take effect on Sunday added pressure to prices today. WTI crude and Brent were mixed, trading at $63.49/barrel (-0.36%) and $72.92/barrel (+0.04%) respectively. In precious metals, gold is on track to post its fifth weekly gain today, last seen at $1,236/ounce (+0.25%).

Day Ahead: US nonfarm payrolls & wage data and Canadian jobs figures on the agenda

US nonfarm payrolls will take center stage on Friday with the potential to shake the US dollar which has been losing ground against a basket of six major currencies so far in the day. Canadian employment figures will attract interest as well.

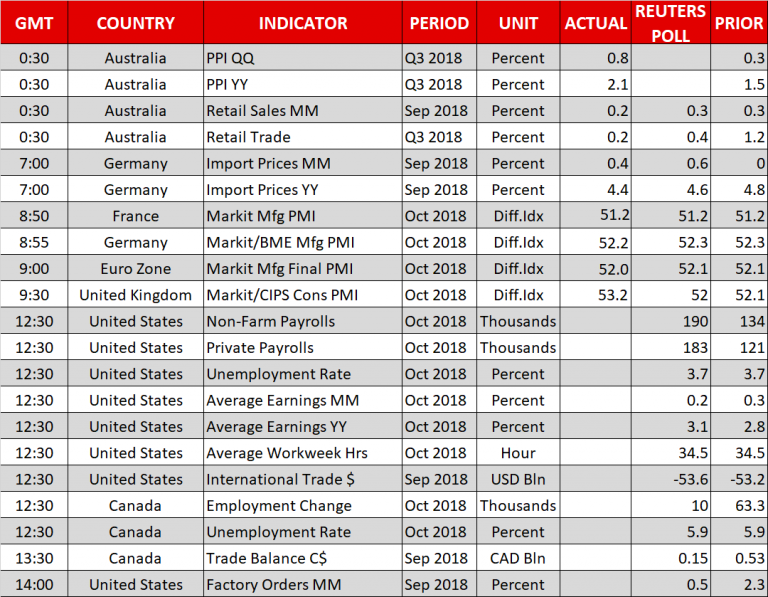

Following Wednesday’s upbeat ADP employment report which tracks changes in the private sector, the government’s comprehensive nonfarm payrolls due at 1230 GMT are expected to come higher at 190k new positions in October compared to 134k seen in September. The unemployment rate is forecast to have stayed unchanged at 3.7%, at the lowest since 1969. Analysts believe that average hourly earnings have risen by 3.1% y/y compared 2.8% in the previous month, reaching the highest growth pace since April 2009, while on a monthly basis they see a softer increase of 0.2% m/m versus 0.3% before. Should the report beat expectations especially on the wage front, buying interest for the greenback may accelerate. Meanwhile better wage numbers could hurt equities. However, given the upbeat sentiment surrounding the US-China trade conflict, we don’t expect a major tumble in case the figures dissapoint.

In other data releases out of the US, trade stats for the month of September (1230 GMT) are expected to show a slightly wider decifit, while September’s factory orders (1400 GMT) are anticipated to grow by 0.5% m/m after marking a 2.3% expansion in the previous month.

At the same time, Canada will be also publishing its own employment data for October. The unemployment rate is forecast to have held steady at 5.9%, while the number of employees are expected to have risen by 10k, by less than in September when the measure showed a gain of 63.3k. At its latest policy meeting in the prior week, the Bank of Canada raised interest rates to 1.75% and removed the part mentioning that officials will “take a gradual approach” with regards to rate hikes. Moreover, they simply noted that “in determining the appropriate pace of rate increases, Governing Council will continue to take into account how the economy is adjusting to higher interest rates”. Therefore, a decent employment report combined with a decent GDP growth number on Wednesday could keep bets for further and faster rate increases elevated.

Separately, Canadian trade surplus (1330 GMT) is said to have narrowed in September.

In corporate news, the Chinese online retailer Alibaba Group Holdings will be publishing earnings results before the US market open.